September 30, 2017

“If you can remember that stocks aren’t pieces of paper that gyrate all the time – they are fractional interests in businesses – it all makes sense.” Seth Klarman

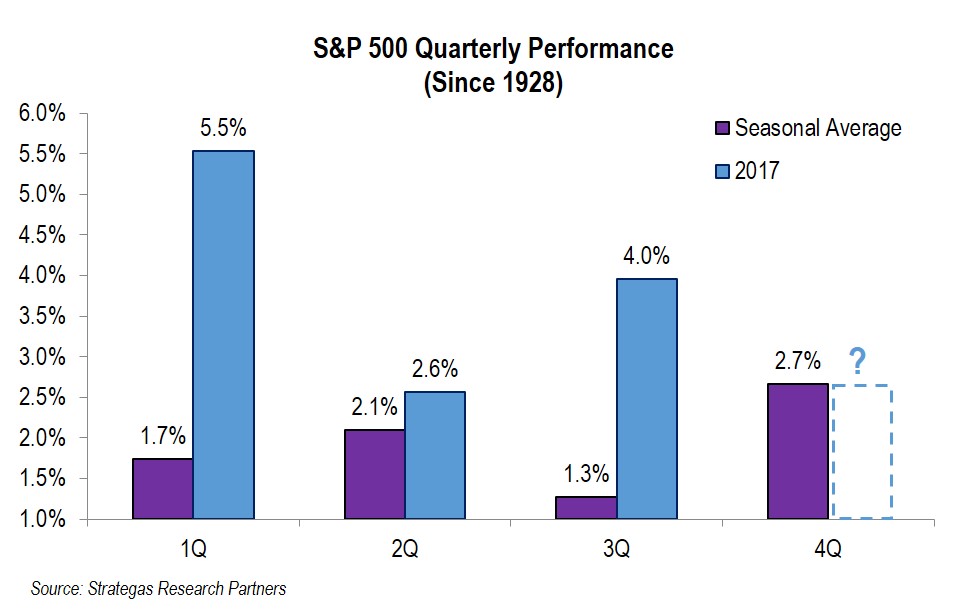

The third quarter proved to be a very successful one for our clients with all of our traditional and defensive strategies recording meaningful gains. Even the historically weak period of August and September proved to be positive for all of these strategies. Historically the outlook for the fourth quarter is positive:

Despite many investors waiting for the proverbial shoe to drop, strong earnings growth and the combination of low interest rates and low inflation provided the energy to drive equity prices higher for the third quarter and thus far this year. As the chart above demonstrates, at least from a historical standpoint, the fourth quarter has on average been the strongest performing quarter. Of note, international equities continue to make strong gains this year and are outpacing the S&P 500 for the first time in several years. Fortunately we have continued to increase our international exposure and this contributed to gains in several of our equity strategies. These international gains reflect the economic progress made in part in Europe and Japan as their economies are modestly growing and the companies in those regions are prospering. Thus, in our opinion, the apparent synchronized global growth is a major reason for the global stock market’s strength. How things have changed! Remember the days when the headlines out of Europe were quite disconcerting? (Greece going broke; Italy going broke; the EU disintegrating!)

All of our strategies are continuing a solid year of performance. This is especially noteworthy as indexing/passive strategies continue to gain favor, but have been left behind from a performance standpoint by many of our strategies this year. We believe this is important as we face the future with some growing clouds that give us cause for concern. The Federal Reserve’s continued path of raising interest rates and starting to taper its balance sheet should warrant at least some level of caution for investors in equities, real estate, private equity, and other asset classes. Money will get somewhat more expensive and the flood of cheap money driving up certain asset values is something to be watched. We are noting some weakness in commercial and residential real estate as too much supply comes to market in certain regions of the country. Additionally, in our opinion, many private equity managers have raised significant sums of money which they are now looking to invest somewhere. We are hearing of rich prices being paid for both some real estate and private equity investments. Also, geopolitical risks continue to be front and center with the aggressive actions of North Korea and the frequent verbal attacks from President Trump. This coupled with the continuing war in Syria as well as the fight against ISIS, is something that markets have shrugged off (thus far) but could create some volatility in the future. It is important to remember that volatility is at historical lows.

These clouds and others that exist, including the growing bifurcation of political ideology and wealth disparity, could impact the positive psychology that has given investors confidence. What has trumped (no pun intended) these clouds thus far has been the positive economic fundamentals mentioned earlier. Patience as an investor reflects faith in the spirit of America (even as it appears somewhat frayed right now) and a government that can be somewhat responsive, even if it appears to be dysfunctional at times. To sustain this long period of investment gains and economic prosperity, we need greater growth to support the somewhat high current valuations as well as assuaging investor anxiety. We continue to find, and ferret out, what we believe to be sound investment opportunities for the long term in each of our strategies even with markets making new highs on a regular basis. Make no mistake, we do not subscribe to the efficient market theory. Therefore through thorough research and inefficient markets, which typically view things through a short-term lens, we are still finding long-term opportunities in specific companies, real estate, and an occasional private equity idea.

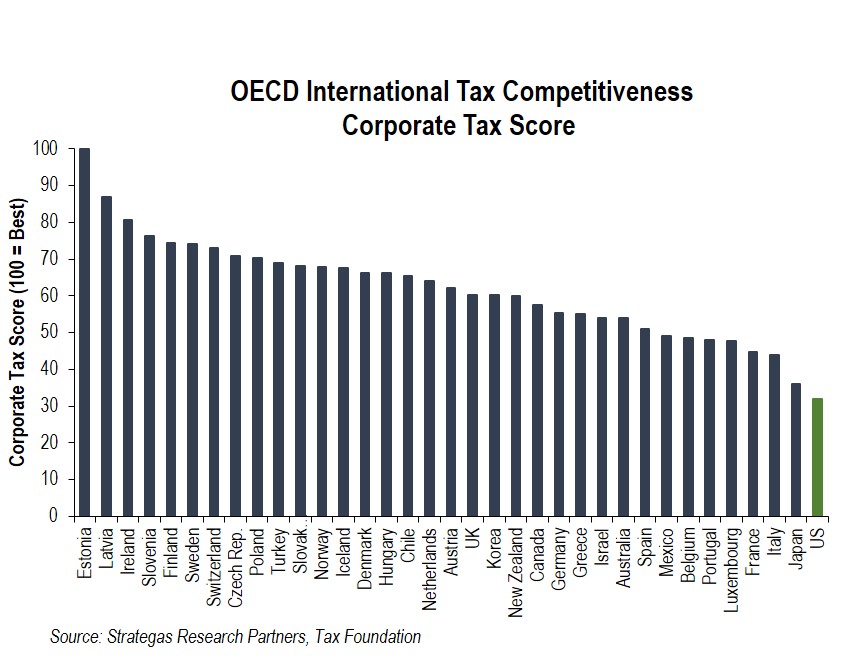

As investors feel nervous about various markets being at all-time highs yet again, the major tax cut/reform program recently announced by President Trump and his administration to enhance domestic growth is on their radar. This aggressive plan, the first such major reform in thirty years, if passed (in some form) would provide significant corporate tax relief and the potential for repatriation of foreign-sourced earnings. This may even garner bipartisan support based on how uncompetitive the United States is versus other developed nations from a corporate tax standpoint:

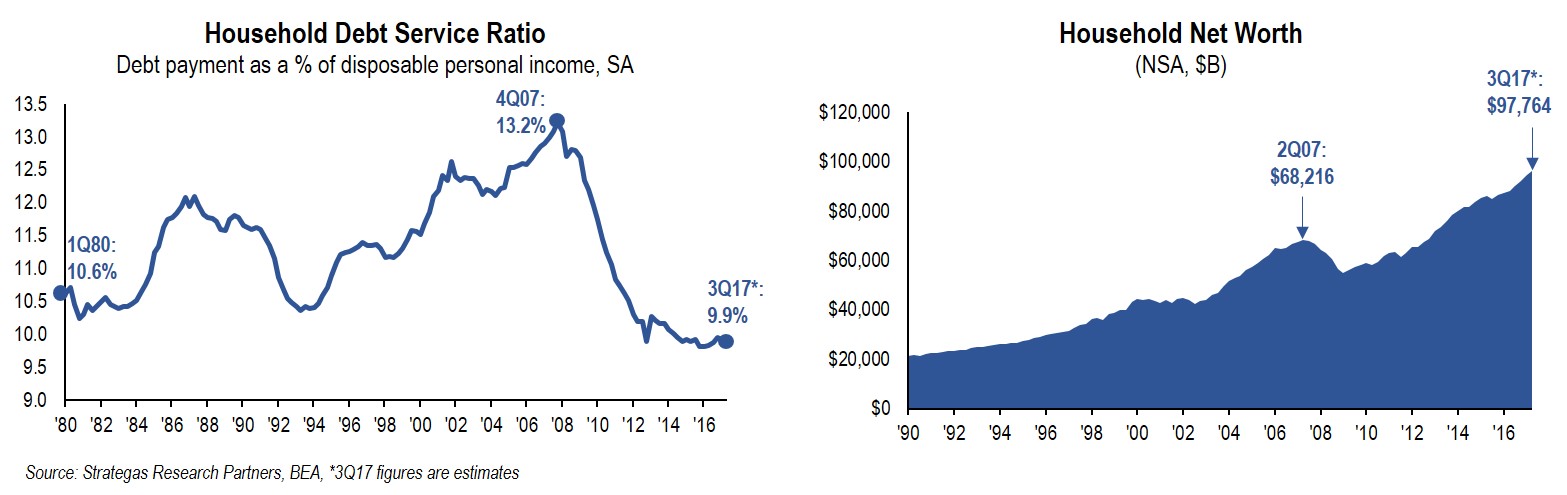

It is clear from the chart above that the United States needs to cut corporate taxes in order to be competitive with the rest of the developed world. It is obvious why many companies have sought to move operations overseas and it is apparent why we have lost jobs to these foreign countries. The combination of a lower corporate tax rate, bringing back significant foreign-sourced earnings to the U.S., and giving an incentive to domestic businesses to promptly invest in the U.S. would be a pro-growth platform that could result in faster and sustained domestic economic growth. These actions coupled with tax cuts for individuals and reform to help the beleaguered middle class would also push a domestic economy forward, of which 70% is based on consumer spending. By the way, the consumer has gotten into better financial shape since the “decession,” as you can see from the charts below, despite government policy that could be more helpful:

Tax cuts for individuals would also bring relief to those who have been facing increased medical costs from the flawed Affordable Care Act. This act has not been replaced, but is in need of surgery to make it more effective and affordable. Both sides of the aisle should see both corporate and individual tax reform as being essential to growing our economy at a faster pace than the past eight years. This would, in our opinion, give a boost to the earnings of many of the companies we invest in as well as many others. Increased earnings would make current valuations, which are somewhat on the high side, more reasonable. Of course, if nothing happens in this arena, there could be a let down on Wall Street as well as in investor psychology. That would set up a very difficult and contentious November 2018 election cycle for both investors and politicians.

Summary

Our third quarter was very good from an absolute standpoint. Our clients continued to see their mandates with us grow in value. The fourth quarter faces some clouds that we have outlined, while at the same time brings the anticipation of better earnings and possible significant tax reform. These two factors represent reasons for optimism. Interest rates remain low but with a slight upward bias. Bonds are still not attractive in our opinion and we remain underweight, especially as the Fed considers reducing its balance sheet which could increase interest rates. Traditional equity valuations are somewhat stretched by historical norms so we remain underweight. Low inflation and low interest rates make stocks more attractive but continued increased earnings are necessary to support these valuations and see them grow from here. For these reasons, we still remain biased to our defensive strategies which have delivered excellent results thus far this year. As compared to our other investment strategies, these results have only been equaled or outdone by several of our traditional equity strategies. However, we remain somewhat underweight to these traditional equity strategies given our concern that valuations have gotten somewhat ahead of themselves, and the chance that tax reform goes the way of the partisan gridlock in D.C. Although we believe that some tax reform will take place, we cannot guarantee it and therefore erring on the side of caution seems the prudent direction to take in our recommended asset allocations.

One of our consulting economists spoke at our June seminar. He made a point to tell our gathering that returns from this point will be less than what we have experienced in the past several years, in his opinion. He did not think we were facing a recession in the near-term (and neither do we). Nor did he think that corporate earnings were facing an imminent downturn (nor do we). He did cite the current higher starting valuation level after many years of market appreciation. As valuation is a very significant factor in the returns we can reasonably expect to achieve in the long run we believe this to be a prudent observation.

In the end, in our opinion, fundamentals drive valuations in all asset classes we invest in. Our approach is to invest piece by piece in each company, real estate opportunity, or private equity situation. As stated in our quarterly quote, we invest in specific companies based on their individual fundamentals. Over the long term this has worked. As we face an older bull market, potential “clouds” as mentioned earlier, some favorable factors still contributing to a growing economy, paying attention to the specifics of concentrated portfolios should be an advantage as opposed to hoping for entire markets to appreciate.

Again, we are grateful for your support and confidence in us. We are delighted to have achieved quite favorable results for the quarter and the year-to-date on clients’ behalf. Permitting us to invest for you in a concentrated but diversified manner has exposed your capital to meaningful gains this year. We are optimistic that this approach will continue to work for you over the long term.

Enjoy the upcoming holiday season. We hope to see you at our upcoming Thought Leadership Seminar with our special guest, Dr. Tara Maller, a former CIA Military Analyst, contributor to many cable TV stations, and an expert in the unfortunate subject of terror. Please call us with any questions you have on your asset allocation, your investments with us, and any other wealth management matters that we can be of assistance on.

Best regards,

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. Disclaimer: The views expressed are the views of Robert D. Rosenthal through the period ending October 19, 2017, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC. Copyright © 2017 by First Long Island Investors, LLC. All rights reserved.