“Invest for the long haul. Don’t get too greedy and don’t get too scared.”

– Shelby M.C. Davis

The first quarter resulted in strong absolute returns for our defensive and traditional equity strategies. Most strategies have exceeded their respective benchmarks year-to-date. This follows a significant bounce back in 2023 in the wake of a very difficult 2022 for equity and fixed income markets. In fact, several of our strategies have exceeded the prior peak at year-end 2021, which reflected several years of large gains. So, when one invests for the long haul, as the above quote states, they should be rewarded when the emotions of greed or fear do not prevail. There is one exception, fixed income, which was about flat for the first quarter including interest, following 2023 where results were modestly higher, and 2022 when losses were incurred.

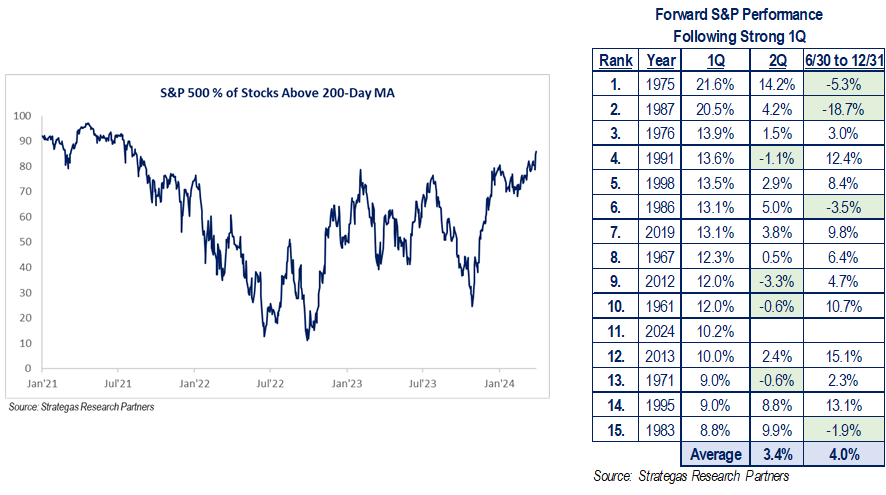

Early on, the first quarter continued to be led by a small number of large-cap growth companies, such that the Russell 1000 Growth Index outperformed the rival Russell 1000 Value Index. This can mostly be attributed to the disruption of artificial intelligence (AI) and its role in many growth companies. In addition, international investing, while positive, also underperformed its rival S&P 500 Index. We believe these positive results, led by growth companies, reflect reduced inflation, higher earnings, few prospects for recession, and a Fed that most recently indicated three interest rate cuts were being considered later in the year. Of note, in the past several weeks, we witnessed a broadening out of stocks achieving 52-week highs, many of which were outside the large-cap, technology-oriented companies. We are watching valuation very carefully, especially for the largest technology-oriented companies, where even the reference to AI has led to share price gains.

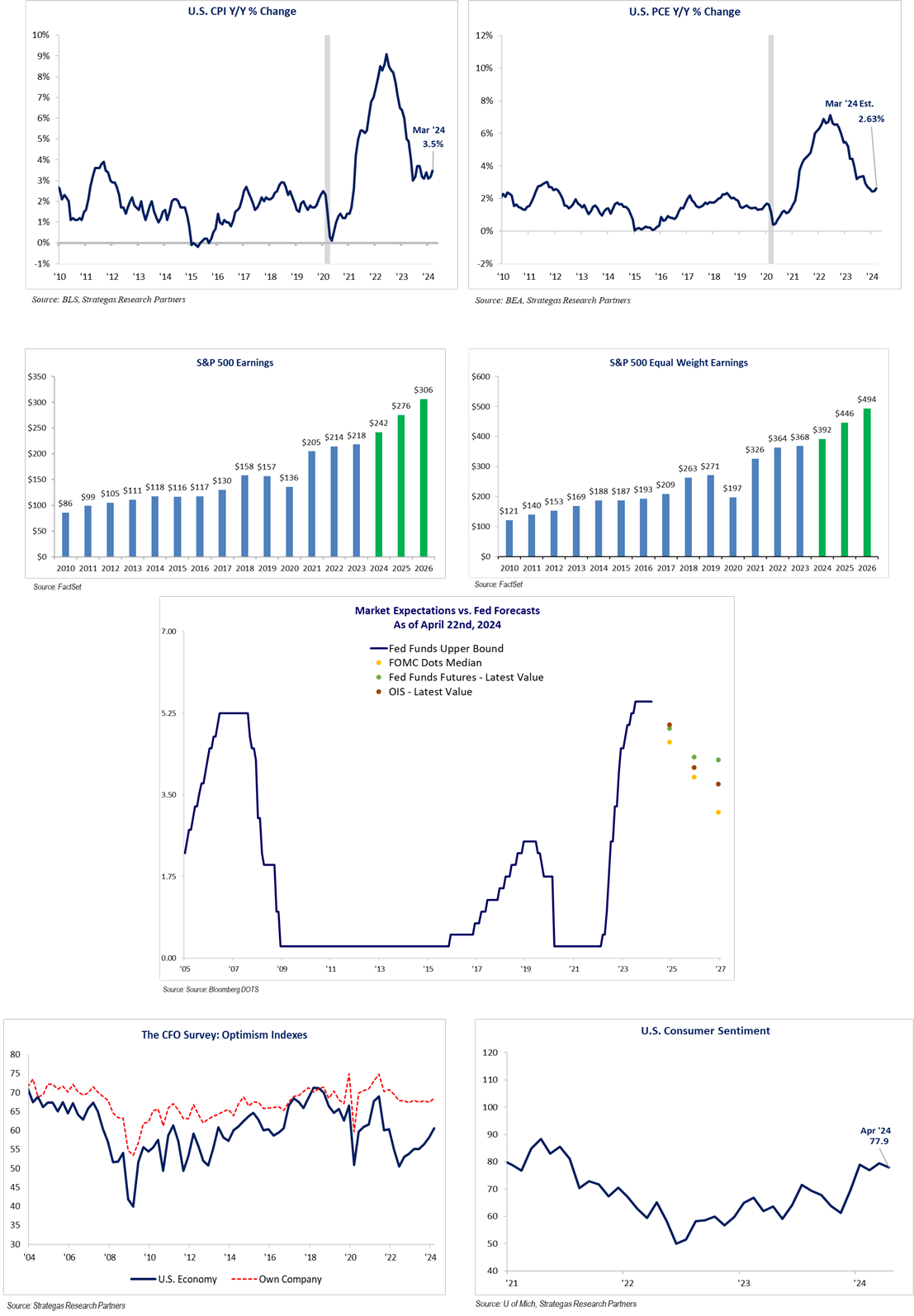

The following charts reinforce our view that there is some broadening out of the markets, inflation is trending down (although not yet at a level sought by the Fed), earnings growth estimates for the average large company (S&P 500 Index) continues to be positive for 2024, and employment (not pictured) continues to reflect a strong, although slowing, economy (not one headed for recession in 2024).

As the charts suggest from our consultant, Strategas Research Partners, the performance in the first quarter “rarely” suggests a market top.

It appears, for now, that the economy can constructively deal with the yield on the 10-year U.S. Treasury being in a range of 3.75% to 4.75% and inflation that has dropped to 2.8% for the core PCE (the Fed’s preferred inflation measure) while unemployment remains below 4% and GDP growth is forecasted to be approximately 2%. These factors contribute to the projected growth in corporate earnings and our belief that we will continue to grow our clients’ wealth, with a prudent asset allocation, over the course of this year. Anecdotally, our contacts in the real estate industry have also indicated that financial conditions in real-estate financing have finally improved. A note of optimism.

So, what can go wrong?

With two wars raging and a presidential-election year unfolding, we cannot afford to be complacent. The Middle Eastern war between Israel and Hamas (a proxy for Iran) could result in an escalation of hostilities. Already, the Houthis (another Iranian proxy) are attacking ships in the Red Sea, causing some havoc with global trade. This could result in an upturn in inflation. Of course, a growing conflict in the region with another Iranian proxy, Hezbollah in Lebanon, is simmering. Also, there is no end in sight to the war between Russia and Ukraine. American policy is being challenged politically in the case of both wars as well as the potential cost to the American taxpayer. Fortunately, these events have not been disruptive to our financial markets thus far.

The heating up of our domestic political environment is another concern. Illegal immigration across our southern border has reached a crisis. The influx of immigrants to sanctuary cities and elsewhere is also causing an economic strain. Immigration, crime, proposed major tax increases by the current administration, and women’s reproductive rights are all major issues that will be debated as the year goes on. This, of course, is on top of the embedded inflation that Americans are faced with despite the rate of inflation abating. Additionally, the collapse of the Francis Scott Key bridge in Baltimore could have a minor inflationary impact.

Historically, equity markets have performed reasonably well in the fourth year of a presidential term. To help that result, incumbent administrations have at their disposal the power to spend. In this year’s case, the President has the CHIPS and Science Act, the Infrastructure Investment and Jobs Act, and the Inflation Reduction Act at his disposal to help the economy along. Again, we have said, both last year and this year in our thought pieces that we do not see the prospects of a recession occurring during this election year. This is a positive, to be weighed along with the uncertainty of two presumptive nominees who, according to the polls, a majority of Americans view as unfavorable.

Summary

We are off to a very good start, which historically has resulted in good results for the year, but there are many moving parts domestically and a significant level of geopolitical uncertainty. Some level of optimism is based on the Fed reducing rates at some point during the year. If inflation does not continue to abate and the Fed does an about face, that would not be good for equity, fixed income, or real-estate markets. The same could be said, in our opinion, as it relates to private equity.

We remain cautiously optimistic given the propensity of what we have described above. However, we remain true to our cautious nature while still working to grow our clients’ wealth through an individualized, prudent asset allocation. One that reflects a broadening of company participants in the equity markets’ rise, that includes owning both value and growth-oriented companies (which continue to play a major role in stock market advances), and that does not just rely on AI (which we believe is positive and

disruptive). Fixed income, on a pre-inflation, pre-tax basis, will continue to play some role in our asset allocations for clients, but a mix of defensive and traditional equity investments will be the major allocations for most clients.

Enjoy the spring season! Please call upon us for any and all of your wealth management needs. Stay tuned as we see what evolves with both the President’s attempt to increase income and estate taxes as well as the sunsetting of the Trump tax cuts over the next two years.

Best regards,

Robert D. Rosenthal

Chairman, Chief Executive Officer, and Chief Investment Officer

DISCLAIMERS

The views expressed herein are those of Robert D. Rosenthal or First Long Island Investors, LLC (“FLI”), are for informational purposes, and are based on facts, assumptions, and understandings as of April 25, 2024 (the “Publication Date”). This information is subject to change at any time based on market and other conditions. This communication is not an offer to sell any securities or a solicitation of an offer to purchase or sell any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Nothing herein should be construed as a recommendation to purchase any particular security. The companies and securities described herein may not be held in every (or any) FLI strategy at any given time. Investment returns will fluctuate over time, and past performance is not a guarantee of future results.

This communication may not be reproduced, distributed, or transmitted, in whole or in part, by any means, without written permission from FLI.

All performance data presented throughout this communication is net of fees, expenses, and incentive allocations through or as of March 31, 2024, as the case may be, unless otherwise noted. Past performance of FLI and its affiliates, including any strategies or funds mentioned herein, is not indicative of future results. Any forecasts included in this communication are based on the reasonable beliefs of Mr. Rosenthal or FLI as of the Publication Date and are not a guarantee of future performance. This communication may contain forward-looking statements, including observations about markets and industry and regulatory trends. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect the views of the author as of the Publication Date with respect to possible future events. Actual results may differ materially.

FLI believes the information contained herein to be reliable as of the Publication Date but does not warrant its accuracy or completeness. This communication is subject to modification, change, or supplement without prior notice to you. Some of the data presented in and relied upon in this document are based upon data and information provided by unaffiliated third-parties and is subject to change without notice.

NO ASSURANCE CAN BE MADE THAT PROFITS WILL BE ACHIEVED OR THAT SUBSTANTIAL LOSSES WILL NOT BE INCURRED.

Copyright © 2024 by First Long Island Investors, LLC. All rights reserved.