On Thursday June 16, 2022 First Long Island Investors held an online web seminar with Robert F. DeLucia, CFA. Bob was formerly Senior Economist and Portfolio Manager for Prudential Retirement. Prior to that role, he spent 25 years at CIGNA Investment Management and 15 years with Prudential Retirement most recently serving as Chief Economist and Senior Portfolio Manager. He currently serves as a Consulting Economist for Empower. Bob has 50 years of investment experience. He shared with us his latest economic forecast and the implications for global financial markets. He also provided guidance on how the various indicators should be taken into consideration when making investment decisions.

March 31, 2022

“The most important quality for an investor is temperament, not intellect.”

-Warren Buffett

All major indices were negative for the quarter (including bond indices), ending the string of seven quarters of consecutive gains and leaving investors facing a complex environment to navigate Challenges, both economic and geopolitical, which were cited in our 2022 Market Outlook (published in January), abruptly confronted investors during the course of the quarter.

The Fed, recognizing the highest inflation rate in 40 years, finally started a course of increasing the short-term borrowing rate that will be implemented in 2022 and 2023 in addition to ending its asset purchase program. The pace and magnitude of the increases will be data dependent, but it appears at this point to suggest short term rates approximating 2.5%-3.0% by the middle of 2023. The first increase, announced in March, was 25 basis points. At least six more increases are forecasted between now and the end of 2022 given the current level of inflation (8.5% as of March 2022), which the Fed now realizes may only be in part transitory. Americans are facing significantly higher fuel and food costs which in and of itself represents a major tax on the average family. Although we believe certain supply shortages will abate by year end, they are no longer what constitutes the root cause of inflation, as once thought by many.

Short-term borrowing rate increases could lead to long-term rates increasing reflected in the 10-Year U.S. Treasury that will impact mortgage rates and consumers in general; and possibly reduce price earnings multiples on equities if the 10-Year U.S. Treasury rises to above 3.5% in our opinion (as of March 31, 2022, the 10-Year U.S. Treasury was 2.3%). Later in this report we will address the possibility of a recession in 2023, but for right now we do not see a recession in the near term.

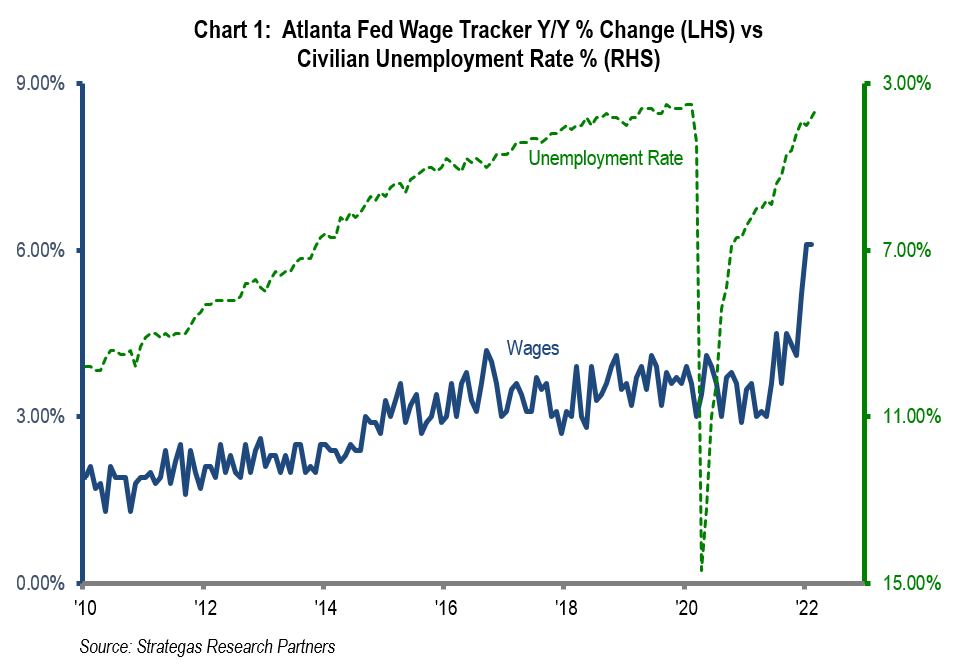

Long desired wage increases have finally made their way into our economy with increases approximating 5.6% most recently. This tracks a lower unemployment rate where labor is becoming scarce making wage increases for many a necessity to do business. Chart 1 shows average wage growth tracking the improvement in the unemployment rate. Of course, these trends follow the abatement of COVID-19 or perhaps our improved ability to navigate COVID-19 given vaccines, boosters, monoclonal antibody treatments, and the new drugs from both Pfizer and Merck. These provide relief for people contracting the virus and helps keep them out of the hospital. However, based on scientific opinion, variants of the coronavirus appear here to stay and boosters seem to be a preventive measure that we will all be receiving for quite a while.

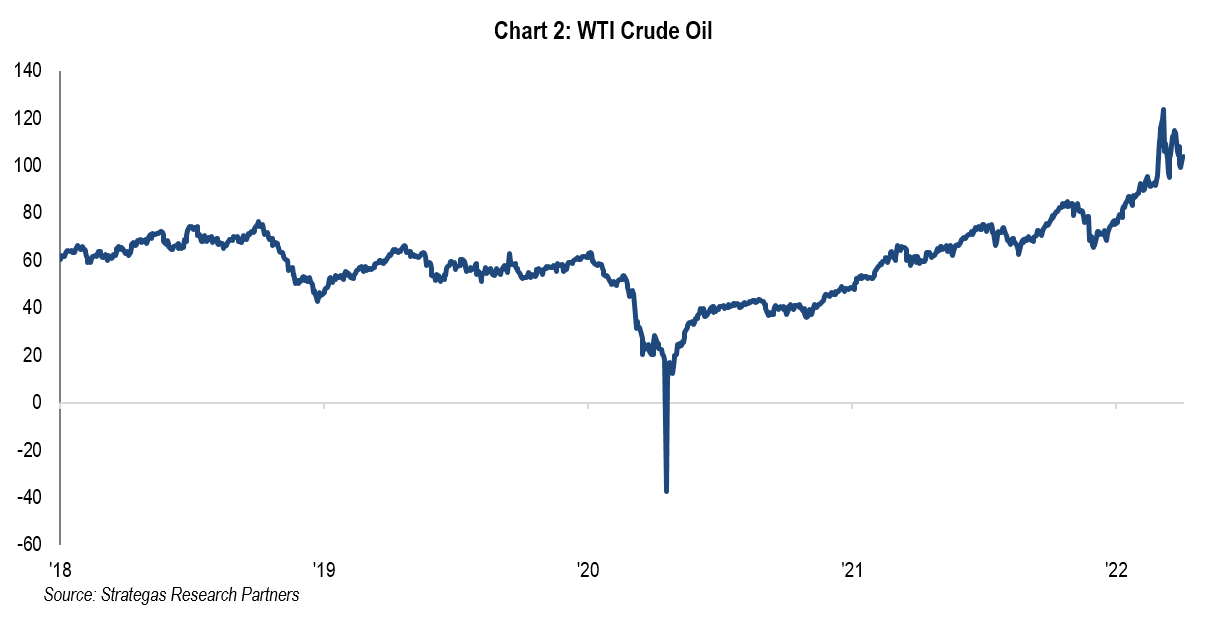

Besides wage increases, which we do not believe are transitory, fuel costs have soared. The increase in fuel costs (oil) seem to have been parallel to the Administration’s focus on alternative energy sources and a deemphasis on fossil fuels. Chart 2 shows the increase in the price of oil over the last several years. The initial surge began with the election of President Biden. The second surge has occurred with the Russian invasion of Ukraine and our government’s decision to stop importing some of our energy needs from Russia. At this time, the President has decided for the second time in the last six months to release oil from our Strategic Petroleum Reserve (a reserve that was created in 1975 to provide emergency protection given geopolitical strife in the Middle East). In our opinion, releasing oil from our Strategic Petroleum Reserve will not have a long-term positive impact on oil prices (the release of reserves is currently slated from now until the fall).

The current causes of the rising price of oil and natural gas are complex. Certain regulatory guidelines imposed by the new Administration limited the ability of U.S. production to meet the rising demand in 2021, driving oil and fuel prices higher. Add to that, the outrageous invasion of Ukraine has led to significant economic sanctions against Russia including scaling back energy purchases. This is forcing the U.S. and European nations to seek supplies elsewhere. An obvious partial solution would be to attempt to more aggressively increase oil production domestically, but the Biden administration is trying to balance the needs of domestic oil production and combating climate change. Middle Eastern countries have been urged to increase their production, but thus far this has not resulted in much success. Increased oil from such disreputable countries as Iran and Venezuela are also under consideration but bring geopolitical issues.

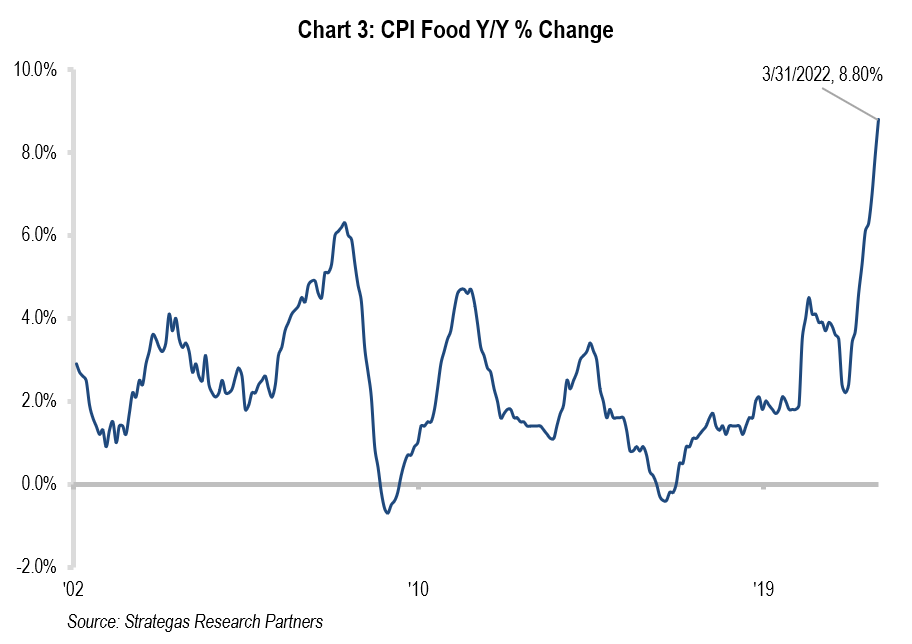

Another significant area of inflation is food prices (as depicted in Chart 3). Here wage growth as well as supply constraints have helped usher in a wave of inflation. However, this situation could get worse as Russia/Ukraine represent about 30% of the wheat (grains) produced globally. Given the ongoing war, we believe that supply will be constrained and this will further impact the price of certain foods going forward. Some countries are seeking to plant on government acreage as a way to increase supply, but this will take time.

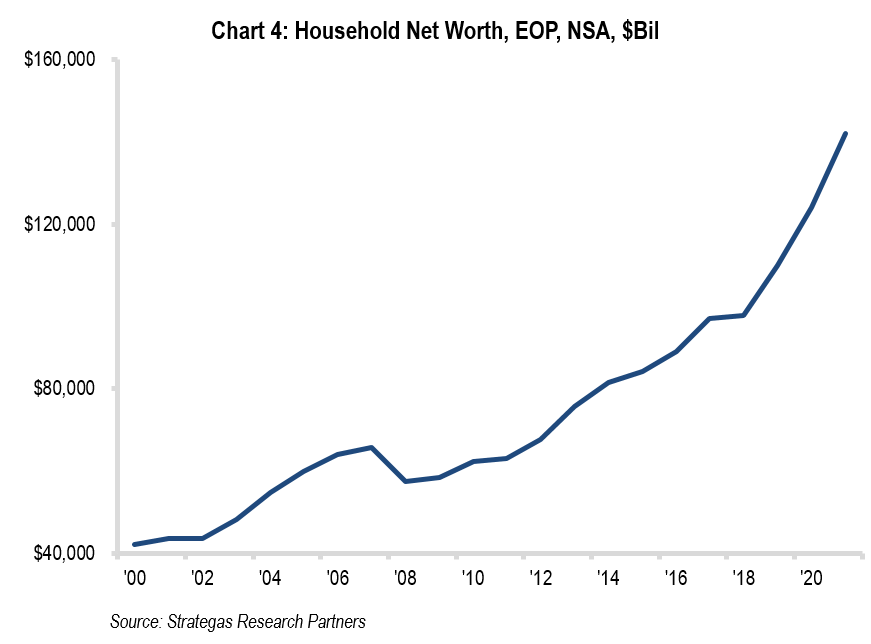

Several key areas including wages, oil, and food are stoking the rise of inflation confronting America. This could at some point lead consumers to reduce their purchases and contract economic growth. However, the consumer still appears very strong from a balance sheet standpoint, as you can see in Chart 4.

Our Complex Investment Environment

Despite starting from record lows, we are still facing higher interest rates for the first time in many years. These rate increases are designed to curtail the highest inflation in 40 years. Rising interest rates and higher inflation at the same time that we have a war raging in Ukraine makes for a pretty high wall of worry for investors. Profits for S&P 500 companies for this year are still projected to rise by 9% despite global concerns while the S&P 500 Index declined by 4.6% during the first quarter. This represents a modest reduction from the beginning of the year probably reflecting slower projected global GDP growth given the war in Ukraine as well as continued pockets of COVID-19 impacting various economies, including that of China. But a down market of 4.6% while still forecasting growth in earnings would seem to suggest some happiness by the end of the year. We believe this is a possibility and seems plausible to us as bond investors must digest negative real returns (absolute return minus the rate of inflation) that makes quality equity investing a better long-term option than investing in bonds (at this time, in our opinion).

Adding to this complex picture is the history of the equity markets appreciating after the first rate increase by the Fed as shown in Chart 5.

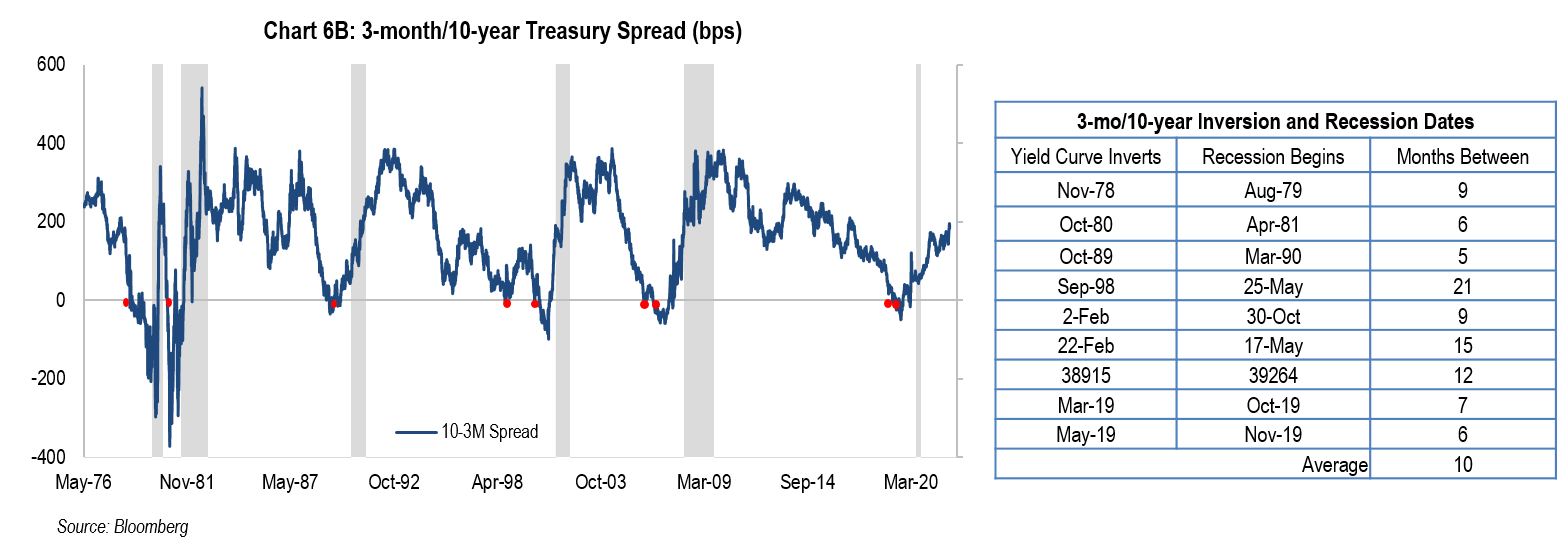

It appears that in times past the equity markets have been able to absorb Fed rate increases especially when earnings and GDP growth were still intact. Also, we must ponder the meaning of potential rate inversion where short-term rates exceed longer-term rates and the ensuing probability and timing of a possible recession. The spread between the 2-year and 10-year U.S. Treasuries slightly inverted for a brief period of time (less than one day) in the first quarter but is not currently inverted. The following charts show that meaningful inversion of the spread between the 2-year and 10-year U.S. Treasuries or that of the 3-month and 10-year U.S. Treasuries have typically been followed by a recession. As you can see in Charts 6A and 6B, recession has typically followed the inversion of the 2-year/10-year spread in the next twelve to eighteen months and of the 3-month/10-year by six to twelve months. We believe the spread between the 3-month and 10-year is more indicative of future economic growth and at this point it does not indicate an imminent recession.

This complex picture shows challenges to investors in the form of Fed rate hikes and possible recession; inflation and the potential impact on consumers and businesses; geopolitical strife with a war in Ukraine; and we still have to navigate the COVID-19 landscape but with many more tools (vaccines, boosters, and novel drugs).

Outlook for 2022

We believe that the complexity of investing right now is daunting, but the challenges are offset to a large extent by the strength of the consumer, our robust banking system, growing corporate profits, companies with pricing power, somewhat more reasonable valuations given the first quarter drop in stock prices, and growing dividends from many of the companies we invest in.

The current confluence of economic and geopolitical factors makes for investor anxiety and market volatility. From a contrarian standpoint, this negativity might be a positive. Our view remains that we should look over the valley of these factors with the expectation that over time, we as investors will continue to make gains. Proper temperament is now required so that we do not act emotionally to the first negative full quarter in two years. Whether one invests in public or private companies or real estate related opportunities quality, growth in cash flow, increasing dividends, and solid financial fundamentals will again be the keys to investment success. This, along with a prudent asset allocation among risk assets and a buffer of cash, is our prescription for weathering the complexity of the current investment environment. Over the longer term, never bet against America!

Please call upon any of us on our investment committee or wealth management team to discuss your asset allocations and/or wealth management needs.

Best regards,

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

P.S. President Biden recently proposed a federal budget. It includes an increase in spending as well as a host of tax increases similar to those proposed last year, but not enacted. It is premature to discuss any aspect of it at this time. We will include discussion on it when warranted.

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. Partnership returns are estimated and are subject to change without notice. Performance information for Dividend Growth, FLI Core and AB Concentrated US Growth strategies represent the performance of their respective composites. FLI average performance figures are dollar weighted based on assets.

The views expressed are the views of Robert D. Rosenthal through the period ending April 22, 2022, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC.

Copyright © 2022 by First Long Island Investors, LLC. All rights reserved.

Barron’s recently asked financial advisors, including Philip Malakoff of First Long Island Investors, how they are navigating 2022’s volatile first quarter.

December 31, 2021

“There are two times in a man’s life when he should not speculate: when he can’t afford it and when he can.” -Mark Twain

The fourth quarter and the year 2021 represented another year (and quarter) of growing wealth for our clients. All of our traditional and defensive strategies were positive in the fourth quarter and for the full year. In fact, each of our defensive and traditional strategies returned double digit gains for the year. This follows similar robust gains in each of 2020 and 2019.

As our thought piece indicated, the period from 2010 to 2021 provided significant compounded gains in wealth for our clients. The S&P 500 Index actually grew at a very significant clip of 15.2% annualized. We attribute these gains to the following:

– Growing corporate earnings

– Growth in domestic GDP

– A significant increase in both monetary growth and fiscal stimulus

– Extremely low interest rates beginning with the financial crisis and following the government imposed economic shutdown after the onset of the pandemic

– A very strong consumer

– Following the near collapse of our banking system in 2008/2009, large money center and regional banks became very strong with all major banks passing stringent federal stress tests

– High levels of employment prior to the pandemic and gains in total employed since the pandemic lows now achieving near pre-pandemic employment levels

However, despite all of the positives mentioned above, many of which should continue to benefit us in 2022, we as investors are confronted with the following challenges:

– Record national debt

– The highest inflation rate in 39 years

– The Federal Reserve indicating that it will start tapering and concluding asset purchases in advance of raising short-term interest rates in 2022

– Financially strained safety nets of both Social Security and Medicare

– Climate change

– Geopolitical challenges with oppressive regimes in China, Russia, and Iran

– Our government paralyzed by extremism on both sides of the aisle

Thus, we do not believe, after leading our clients to significant wealth accumulation, that speculation should be considered rather than prudent asset allocation with a goal of growing wealth on a real basis after inflation and taxes. This is especially so when considering the “wall of worry” that we must scale in the years ahead (including learning to live with the coronavirus, which we believe will become endemic).

I urge you to read our thought piece which was recently sent to you if you have not already digested it, and consider that we believe the next several years of investing will probably not be as robust as the last decade.

We are delighted to have helped our clients achieve great gains in 2021 and look forward to continuing working on your behalf in 2022!

Wishing you a healthy, safe, happy and prosperous New Year.

Best regards,

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. Partnership returns are estimated and are subject to change without notice. Performance information for Dividend Growth, FLI Core and AB Concentrated US Growth strategies represent the performance of their respective composites. FLI average performance figures are dollar weighted based on assets.

The views expressed are the views of Robert D. Rosenthal through the period ending January 27, 2022, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC.

Copyright © 2022 by First Long Island Investors, LLC. All rights reserved.

On Thursday December 9, 2021 First Long Island Investors held an online web seminar where Marshal Cohen, Chief Industry Advisor at The NPD Group, spoke about the seismic shifts in the retail industry. Marshal spoke on a wide range of topics including: which segments of the retail industry are doing well and which are lagging, which pandemic related buying behaviors are continuing and which are starting to decline, the supply chain bottlenecks and how the relieving of those will impact buying and pricing, channels used for shopping and much more. Some of the key points are below:

- In 2021, there will be about $3 trillion worth of US retail spend (including restaurants and grocery) which is comparable to but ahead of spending in prior years which indicates that retail in the US is healthy.

- Dollar growth for the week ending December 4 (this includes cyber Monday week) was up 3% vs. 2020 and up 3% vs. 2019, a more normalized year.

- 2021 monthly data through the end of November shows 16% higher dollar growth and 7% higher unit growth over 2020.

- Breaking things down by pre-COVID, COVID, and 2021 year to date there are some interesting data points:

- In “normal times” 3-5% year over year growth would be considered good, and more than 5% would be considered great.

- The COVID period started with store closures that went all the way through December, including the 2020 holidays. Deep decliners were accessories, apparel, beauty, and footwear while housewares and small appliances, which were a very important part of the COVID lifestyle, were gainers.

- 2021 year to date, the “COVID decliners” rebounded and many of the “COVID winners” are down but still growing at very healthy rates.

| Dollar Percent Change vs. Prior Year | |||

| Category | Pre-COVID (12 months ending Feb 2020) | COVID (Mar – Dec 2020) | Current (Jan – Oct 2021) |

| Accessories | -5% | -34% | +30% |

| Apparel | -1% | -19% | +30% |

| Beauty | +2% | -21% | +31% |

| Footwear | +2% | -16% | +27% |

| Housewares | +1% | +24% | +8% |

| Small Appliances | +3% | +28% | +10% |

- There is a seismic supply shift happening. Marshal remarked many CEOs of large retail companies have shared with him that they are wrestling with how to get all of the merchandise that is out on the waters or on the docks transferred onto railroad cars or trucks and to the consumer.

- The current supply shortage is very likely going to turn into a very different scenario – it actually could turn into a supply overage.

- Three months’ worth of inventory (September, October, and November) are all being received right about now. For example, you couldn’t get a bicycle last year but now they have more bicycles than they can sell.

- Retail sales typically rise throughout the year, peaking in December and then in January there is less demand. Some retailers are discounting the overages now, a little earlier than Marshal would have expected, because they’ve got more inventory than they can sell.

- Pricing. Marshal shared a graph showing weekly data for dollar and unit change going back to February 2020. The data demonstrated a number of upticks. He shared that each of the upticks coincides with government stimulus money. Stimulus money absolutely propped up consumer spending across all major retail industries.

- In addition to spending more, the average selling price also increased. Consumers, even at the lower income levels, were driving the growth during the pandemic and willing to trade up and buy better products. In some cases, it was because it was the only choice and in some cases it was because they felt like stimulus money was free money and why not upgrade.

- Price increases are somewhat due to fewer promotions, the consumption of higher priced products, and less price sensitivity. For example, the first time gas crossed the $3 threshold we were shocked, the second time we were “oh this is not good”, yet by the third time it becomes almost acceptable.

- Employment – October had the highest level of people resigning from their jobs, a new record. Additionally, workers are changing their work environment and working from home in a hybrid or on a full time basis. Pre-pandemic only 8% of the workforce worked from home. That climbed up to close to 85% during the pandemic. It hovered, went down, and then went back up with the delta variant. The NPD Group feels it is roughly now at the level it will reside at, ~20%.

- Work from home impacts many different things.

- Over the last two-three years we’ve seen a decrease in the female side of the labor force. The male side has also decreased, but not at the same rate. As women left the workforce simultaneously the amount spent at restaurants dropped and that wasn’t coincidental.

- Wardrobe and footwear is impacted by work location. The use of automobiles is impacted.

- Based on pre-pandemic trends, more than 47 million workers age 55+ were projected to retire. More than 49 million actually retired. This acceleration in retirement also impacts retail.

- Leisure time correlates to retail in how people are spending their time and therefore their money.

- People are returning to experiences and some travel. Amusement parks, sporting events, movie theaters, and bowling are showing recovery.

- Fine dining is starting to come back. Country club dining saw elevated levels in 2021.

- Cruise lines have been the slowest to recover.

- There was an expectation that once experiences started to recover we would see a decline in tangible items but that is not happening. People are not planning as far out and not buying as far in advance due to worry that a trip or an event may get cancelled.

- The consumer is feeling wealthier than they have felt in years. They’ve been paying off their credit card debt, they’ve certainly been saving more money. Those rates are coming down in recent times but not quite to pre-pandemic levels. The personal savings rate peaked at 33.8% in April of 2020 and as of August 2021 it is back below 10%.

- The number of U.S. households with total household income over $100K has been rising over the last six years and these folks are driving retail growth. 2020 vs. 2019 all of the growth came from the upper end consumer and we are seeing the same in 2021 vs. 2020.

- Demographics are shifting as well. The 55+ generation accounts for nearly one third of discretionary dollar sales. This age group is also shopping online more.

- This is showing you both income and age are the big components driving the consumer, so retailers are recognizing that they should market to the less sexy audience which is that experienced consumer.

- Shift to Digital:

- Marshal shared that in 2015 he was presenting at the National Retail Federation and the speaker before him predicted the death of the retail store with everything sold online by 2020. This speaker also predicted that by 2018 department stores would be obsolete. Marshal took the stage and explained to the audience, that this was absolutely not going to happen.

- Marshal shared a graph looking at monthly data for the percent of sales in-store vs. online.

| % In-store | % online | |

| Jan 2019 | 71% | 29% |

| April 2020 | 52% | 48% |

| Sept 2021 | 64% | 36% |

- The pandemic accelerated the use of the online channel. As we come out of the height of the pandemic consumers are still using digital channels but also returning to brick and mortar stores.

- Looking at the shifts in channels it is best to look at Jan-Aug 2021 vs. Jan-Aug 2019 (pre-pandemic) and we see that e-commerce, grocery stores, mass merchants, and warehouse clubs, all of which were the high flyers during the pandemic, have continued to maintain growth. Tech stores, off-price retailers, and manufacturer owned stores are growing but at much slower rates. Specialty retail is the most challenged, particularly in apparel (e.g. Victoria’s Secret), department stores (i.e. JC Penney), and the restaurant business. The expectation is that the restaurant business is not likely to catch up to 2019 levels until 2023.

- Holiday Dynamics. Looking at the five weeks ending 12/4/21, the total dollars spent in retail is exceeding 2020 by 9% and 2019 by 14%.

- If you go back 20 years you see the same pattern – a decline post-Thanksgiving and then another uptick. 2020 didn’t show this trend because there was not as significant of an uptick for Black Friday. Marshal is not alarmed by the softening as there are still three usually strong weeks to go.

- The NPD Group’s survey on holiday purchasing intentions in September 2021 found the following: 30% of consumers plan on spending more than last year, the #1 item people think to give as a family gift is a TV (35%), the number one self-gift is the thousand dollar plus iPhone (55%), free shipping is the most important priority to consumers when choosing a retailer. This beat out the usual number one answer of value.

- Marshal concluded by sharing that he wants people to think about which businesses are set up to be nimble; to recognize that the consumer is shopping in the here and now; and to sell to a wider sector of consumers. For example, in the beauty business you can sell the same anti-aging skincare products to different age groups by focusing on a different purpose with each, one is anti-aging and one is preventative.

- The COVID lifestyle was driving work from home, healthy from home, fitness from home, educate from home and entertain from home.

After sharing his prepared remarks, Marshal took questions from attendees.

Q: Can you talk a little bit about the buy now, pay later strategy and how that impacts consumers and the overall economy for both the short term and the longer term?

A: Short term it gives the consumer the ability to buy without the same kinds of constraints and shift some spend. As I showed you savings and credit card debt were coming down, but are now back on the rise. As we get through the holidays I anticipate the consumer basically maxing out their credit cards. The buy now, pay later methods gives them the ability to expand their horizons, upgrade their products, buy more expensive products, etc.

Q: (from Bob – CEO and CIO of FLI): The home building and home improvement areas seem to be, from your presentation, very strong. We invest in Home Depot, Lowes, and Williams Sonoma. How do you see the trends for those kinds of companies going forward?

A: We certainly know that those companies can’t maintain the momentum of their growth, but they will continue to be a big driver. Keep in mind a lot of people who moved and bought homes didn’t necessarily have the budget to then upgrade the home, but they have the desire to do it, so there’s still plenty of runway room for the home improvement areas. We did see a decrease in the “do it yourself side” but “the do it for me” part of the business is growing. I’ll give you a great example in home décor – last year, people decorated their home to keep it cozy and comfortable, and they would buy throw pillows and blankets, pajamas and slippers because we were staying home. This year is all about expanding the nucleus, inviting more friends and family, so we’re back to decorating to impress. To your point about Lowes and Home Depot, I don’t think they will maintain the level of growth reached during the pandemic, but they will still be an integral part of the investment that people make in their homes.

Q: You talked a lot about the supply and then the overages and prices and how that’s going to impact the consumer. At a very high level, where do you see that impacting faster, is it more in the luxury goods or in staples? We see shelves and stores empty across the board. Who do you think will rebound first?

A: The biggest rebound is going to be in the commodity side of the equation, where sourcing is distributed across a wider sector of product. Commodities, which includes grocery products but also includes things like underwear and jeans, intimate apparel, etc. They had a lot of challenges early on, but now they’re the ones that I think that are going to hit retailers with an abundance of product. Fashion is the one that’s most vulnerable because those goods are perishable and can’t just be put to the side and sold later in the year. They’ve got to sell them now because they’ve already put into play product for next year. The thing to look for is who’s got product that they’re going to move quickly? Which retailers are going to take the hit early? Think of Old Navy that is selling the product at deep discounts to manage through the inventory. They don’t want to have to go into 2022 with 2021 merchandise, so they are going to be aggressive which could hurt margins.

Q: Do you have any kind of insight or timing as to when the backup at the seaports will kind of ease up and kind of get back to normal.

A: Good luck figuring that one out, but now the answer is we’re already starting to see certain industries have product that is now readily available which is good news. It’s not going to be a universal answer. Fashion will be probably one of the earlier ones to get back in position, hard goods like technology will take a little bit longer, video games will take even longer. I look at tech as one of the slower to recover, and I look at fashion as one of the quicker to recover and toys is another one that’s going to be challenged during Christmas, but right after Christmas there will be plenty of product.

Q: The percentage balance between in store and online you shared feels contrary to what we have been hearing in the news. What do you think is driving the desire to return back to in-store?

A: Excellent question. What’s happening is that as the nation was vaccinated to a sizable degree, and even those that didn’t get vaccinated, we certainly saw events start to just fill with people. In store shopping is not only advantageous because of the touch and feel nature but shopping in store is also a social aspect of our lives. We meet people either in restaurants or we meet people to shop. Furthermore if you are at a loss about what to buy it’s a lot more difficult to navigate on a site to find a substitute product or a product idea than it is to go shop in a store and get that element of education and impulse and feel.