First Long Island Investors, LLC recently welcomed Robert J. O’Neill, former U.S. Navy SEAL Team Six leader and New York Times best-selling author, as the featured guest for our Thought Leadership Breakfast at the Garden City Hotel on June 4th, 2026. During the event, O’Neill shared his remarkable journey from a young man growing up in Butte, Montana, to becoming a member of the elite Naval Special Warfare Development Group, commonly known as SEAL Team Six. Over his sixteen-year military career, O’Neill participated in more than 400 combat missions and was involved in some of the most consequential special operations in modern military history, including the rescue of Captain Richard Phillips from Somali pirates and the mission that resulted in the death of Osama bin Laden.

O’Neill began by discussing the rigorous path to becoming a U.S. Navy SEAL. He described the relentless physical and mental demands of training, emphasizing that success depends less on athletic ability and more on perseverance, teamwork, and the ability to remain calm under pressure. He reflected on the culture of accountability within the SEAL community, where individuals are expected to perform in the most challenging environments while placing the success of the team above personal recognition.

He then recounted his experience serving with SEAL Team Six, one of the nation’s premier counterterrorism units. The missions entrusted to the team often required years of preparation, intelligence gathering, and rehearsal before a single operation could be executed. O’Neill stressed that the public often sees only the final outcome, while the true story lies in the countless hours of training, planning, and coordination that precede every mission.

One of the most memorable stories of the morning centered on the 2009 rescue of Captain Richard Phillips, whose cargo ship had been hijacked by Somali pirates in the Indian Ocean. O’Neill described the complexity of the operation, which required operators to deploy on short notice and adapt to rapidly changing circumstances. The successful rescue demonstrated the importance of preparation, precision, and disciplined execution under extreme pressure. He noted that while the operation became widely known through the film “Captain Phillips,” the real mission reflected the extraordinary professionalism and coordination of the military personnel involved.

O’Neill also provided a firsthand account of Operation Neptune Spear, the 2011 raid in Abbottabad, Pakistan, that ended a decade-long manhunt for Osama bin Laden. He discussed the extensive preparation undertaken by the team, including repeated rehearsals on full-scale mockups of the compound and contingency planning for every conceivable scenario. During the operation, the team faced unexpected challenges, including a helicopter crash upon arrival, yet continued the mission without hesitation. O’Neill reflected on the weight of the moment and the responsibility carried by every member of the assault force, emphasizing that the mission’s success was the result of years of intelligence work and the collective efforts of countless individuals across the military and intelligence communities.

Throughout the discussion, O’Neill connected the lessons of military service to leadership and decision making in business. He highlighted the importance of preparation, adaptability, and trust in high-performing teams. Whether confronting uncertainty in combat or navigating challenges in professional life, he argued that success often depends on maintaining focus, controlling emotions, and executing when circumstances change unexpectedly.

O’Neill concluded by reflecting on the values that shaped his career: discipline, resilience, humility, and service to a purpose larger than oneself. His stories provided a unique perspective on leadership under pressure and demonstrated how the principles developed in elite military units can apply across industries and organizations. Attendees left with a deeper appreciation for the sacrifices made by America’s special operations forces and the enduring lessons that can be drawn from their experiences.

FLI remains committed to offering clients timely insights from top industry experts and thought leaders through the FLI Thought Leadership Breakfast series. We thank Robert O’Neill for sharing his perspective and experiences on leadership, teamwork, and service.

“The big money is not in the buying and the selling, but in the waiting.“ Charlie Munger

The first quarter was marked by significant volatility, driven by a number of factors, which we foreshadowed in both January’s Annual Investment Outlook and a recent market update email. These historical and current factors, which, in our opinion, have negatively impacted equity, fixed-income, and real-estate markets for the short term, include the following:

1) Ongoing uncertainty in U.S. policy, including tariffs, immigration, foreign policy, and affordability.

2) Two avoidable government shutdowns, one of which continues as of this writing.

3) The historical trend of midterm election years being volatile, with equity drawdowns during those years averaging 19%, until after the midterm election, following which markets tend to recover.

4) The outbreak of a hot war involving the U.S. and Israel versus the theocratic driven Iran.

5) The spike in energy costs resulting from Iran’s apparently illegal closing of the Strait of Hormuz.

6) Uncertainty regarding the direction of interest rates, which for now have risen by about 10% for the 10-year U.S. Treasury (or 38 basis points), impacting mortgage rates.

7) Questions about how beneficial the One Big Beautiful Bill Act of 2025 will be for the domestic economy, given significant business breaks and reduced taxes for certain individuals from the easing of limitations on the SALT deduction as well as other deductions, including breaks on tips, Social Security income, and overtime wages.

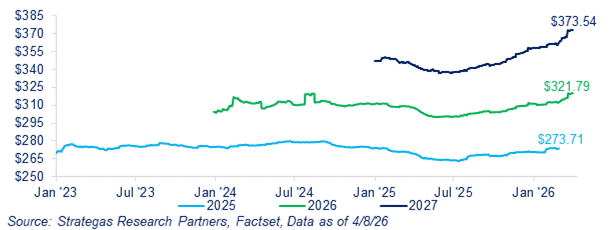

8) The projected robust increase in earnings for the S&P 500® Index for 2026 and 2027.

9) The evolving phenomenon of artificial intelligence (AI) and its implications.

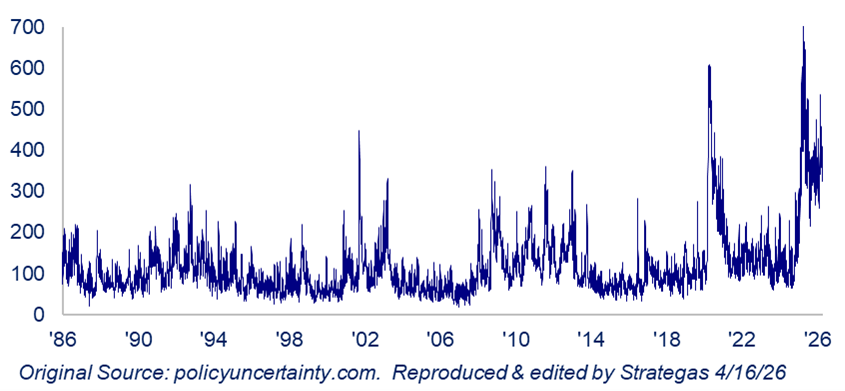

Let us begin by examining what has historically occurred during periods of significant “policy uncertainty” from the U.S. government as evidenced by both domestic and geopolitical actions:

| Exhibit 1: U.S. Policy Uncertainty Daily Index (7-Day Moving Average) Key Takeaway: Policy uncertainty is highly event-driven, marked by sharp spikes rather than steady trends. |

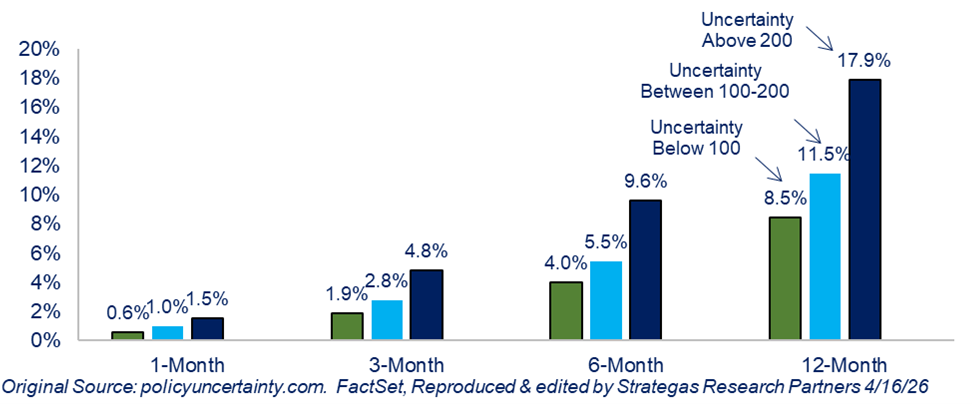

As you can see, uncertainty that began last year with the ever-changing tariff policy eventually receded, but has now intensified again due to the war in the Middle East, government shutdowns, and ongoing tariff changes. The following chart demonstrates that, historically, periods of extreme policy uncertainty have often been followed by sizable returns for the S&P 500® Index:

| Exhibit 2: S&P 500® Index Returns Following Spikes In U.S. Policy Uncertainty (Using Daily Policy Uncertainty Index: January 1985 – April 16, 2026) Key Takeaway: Markets typically absorb policy shocks quickly, with S&P 500® Index returns stabilizing or improving after uncertainty spikes. |

This chart demonstrates that following periods of extreme uncertainty, equity markets have returned an average of 18% one year later (for the period of March 1985 through March 2026). With growing earnings, which we will address a bit later, we remain cautiously optimistic that history may repeat itself.

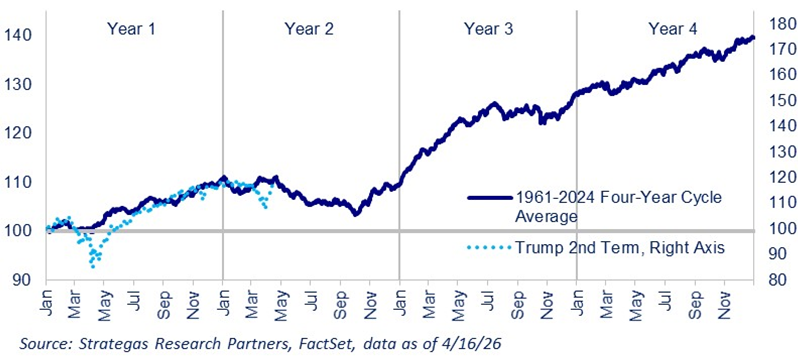

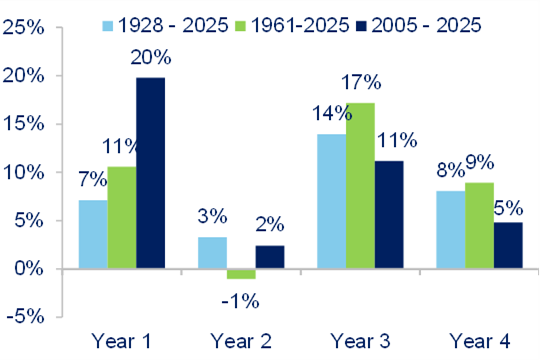

Historically, midterm election years are volatile and tend to produce the poorest returns for stocks within a typical four-year Presidential term. The following chart shows the historical performance during the four-year term, dating back to 1961:

| Exhibit 3: Average S&P 500® Index Price Returns During Four-Year Presidential Cycle (1961-2024) Key Takeaway: The S&P 500® Index presidential cycle shows a repeatable pattern of weakness in Year 2, strength in Year 3, and attractive, but moderate gains, in Year 4, however it should be viewed as a statistical tendency—not a predictive tool. |

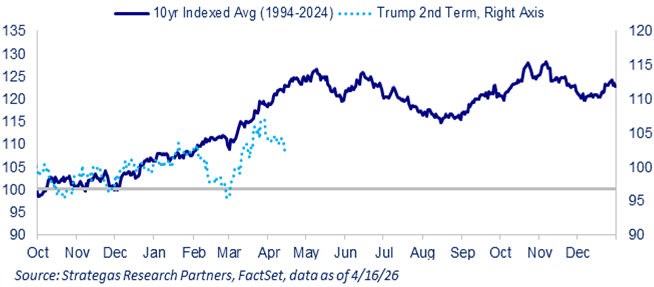

The above chart illustrates our earlier point: year two, the midterm election year, typically brings volatility and market drawdowns until the midterm, followed by a significant recovery post-election and into the third year of a presidential term. At the same time, we believed that interest rates for the 10-year U.S. Treasury would likely rise temporarily before stabilizing. This trend is playing out as we write this report.

| Exhibit 4: Average 10-Year Yield (Indexed) From October of Year 1 Through Year-End Year 2 Of Presidential Cycle (1994-2024) Key Takeaway: The pattern shows that the 10-year U.S. Treasury yield tends to enter a “re-pricing and confirmation phase” during the early-to-mid presidential cycle, where direction is driven less by politics and more by inflation and growth expectations. |

Interest rates are critically important, especially as we face the likely replacement of current Federal Reserve Chairman Jerome Powell at the end of his term. The balance between inflation protection and full employment is being tested in light of rising energy costs from the Middle East conflict and concerns that AI could replace large numbers of employees. Yet, higher S&P 500®Index earnings, including the presumed benefits from a robust tax law, suggest employment stability, in our view. Higher interest rates from the Federal Reserve were detrimental to stocks in 2022; however, we do not expect the Federal Reserve to raise rates anytime soon. While the market expectation for a reduction of two short-term rate cuts in 2026, based on consensus estimates at the end of 2025 may not materialize, even a single rate cut by the end of the year could boost stocks, given the projected increase in profits:

| Exhibit 5: 2025 vs. 2026 vs. 2027 S&P 500® Index Earnings Per Share Progression Key Takeaway: Earnings growth expectations sit in the 16-17% range for this year and next. |

This robust projection of improving corporate earnings is impressive. However, we would not be surprised if these projected earnings are revised downward somewhat over time, and yet they still give us reason for optimism. In an environment with less policy uncertainty and stable interest rates, we believe equities will recover toward the end of the year, following historical patterns.

Of course, the ongoing war in the Middle East as of March 31, 2026 is sobering for investors, as spiking oil costs are likely to impact inflation, at least temporarily. This oil shock has led our outside economics advisor to somewhat increase the odds of recession, though we do not believe this shock will cause one. The impact on stocks has been notable; the average stock in the S&P 500® Index has declined by 21% from its highs, while the index itself has only fallen about 9%:

| Exhibit 6: S&P 500® Index Average Stock % Decline From 52 Week High Key Takeaway: Average stock decline in the S&P 500® Index is -21%, despite the headline index falling just -9% |

The bottom line is that the declines investors are experiencing are steeper than what the index itself reflects, as the S&P 500® Index drop from its highs earlier in January understates the average stock’s losses. If Iran’s stranglehold on the Strait of Hormuz persists for months, the resulting increase in global inflation could be more significant and prolonged.

To summarize:

In January’s Annual Investment Outlook, we highlighted the historical “chop” and typical market correction that often occurs during a midterm election year. Since then, areas of concern have mounted: the continuing partial government shut down; ongoing tariff re-regulation (new tariffs recently announced on certain pharmaceuticals); uncertainty surrounding the potential replacement of Federal Reserve Chairman Jerome Powell; questions about the direction of interest rates; the Iran war given energy’s impact on inflation; and the evolution of AI and its implications for investment, productivity, and employment. Additionally, the current strain between the U.S. and its NATO allies is troubling, as many NATO countries are not supporting the war against Iran, a conflict with consequences that are hurting their economies, not to mention the broader threat Iran poses to global peace, in my opinion.

On the positive side, the forecasted robust rise in S&P 500® Index earnings, the presumed favorable impact of the One Big Beautiful Bill Act of 2025, and productivity gains from the build out of AI. Stock prices have declined, in our opinion, all contribute to compression of price-earnings multiples, while earnings for many companies have increased. This volatility has allowed value stocks, including our Dividend Growth strategy, to perform better than growth-oriented companies for now. For example, the Magnificent 7 are down on average 12%, despite rapidly growing earnings for most, if not all. We expect this trend to reverse as earnings continue to grow throughout the year.

2026 will be a challenging year for investors, but we believe returns will improve as uncertainty diminishes, and we are confident that it will. We also expect energy prices to recede and inflation to rise, though not substantially. However, much depends on the duration of the energy shock caused by spiking oil prices. In our view, the Federal Reserve will not raise rates, and while gross domestic product (GDP) growth may slow, we do not anticipate a recession. We also believe that history will repeat itself, with meaningful equity gains from this point forward, and that business will return to a more normal environment for real estate and capital markets.

Whatever the outcome of the midterm elections, it will provide a degree of certainty compared to where we stand now. Investors value certainty, and with a Republican in the White House, even if both Houses flip to the Democrats, significant new policy changes are unlikely in the foreseeable future.

So, we advise against emotional reactions. Sit tight with the customized diversification we recommend, which encompasses exposure to our four investment baskets that typically favors our defensive basket. Let earnings and dividend growth play out this year, leading to even better valuations, especially for quality companies. Over the long term, that is what matters. Hopefully, the war in Iran will resolve in weeks rather than months, and Iran will cease to pose the threat to global peace that has troubled the last four Presidents from both parties.

Finally, we believe that AI is real and will help the free world evolve from a technical, medical, and productivity standpoint, benefitting all of us, hopefully without significant negative impact on employment. However, there will be business winners and losers, with some companies gaining tailwinds and others facing headwinds from AI adoption. Our job is to be patient and careful in our stock selection. The one risk we will monitor closely is the overall impact of elevated energy costs on inflation and how long that effect will last.

Please do not hesitate to call anyone on our investment or wealth management committees should you have any questions.

Have a great spring!

Robert D. Rosenthal

Chairman, Chief Executive Officer and Chief Investment Officer

DISCLAIMER

The views expressed herein are those of Robert D. Rosenthal or First Long Island Investors, LLC (“FLI”), are for informational purposes, and are based on facts, assumptions, and understandings as of April 24, 2026 (the “Publication Date”). This information is subject to change at any time based on market and other conditions. This communication is not an offer to sell any securities or a solicitation of an offer to purchase or sell any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Nothing herein should be construed as a recommendation to purchase any particular security. The companies and securities described herein may not be held in every (or any) FLI strategy at any given time. Investment returns will fluctuate over time, and past performance is not a guarantee of future results.

This communication may not be reproduced, distributed, or transmitted, in whole or in part, by any means, without written permission from FLI.

All performance data presented throughout this communication is net of fees, expenses, and incentive allocations through or as of March 31, 2026, as the case may be, unless otherwise noted. Past performance of FLI and its affiliates, including any strategies or funds mentioned herein, is not indicative of future results. Any forecasts included in this communication are based on the reasonable beliefs of Mr. Rosenthal or FLI as of the Publication Date and are not a guarantee of future performance. This communication may contain forward-looking statements, including observations about markets and industry and regulatory trends. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect the views of the author as of the Publication Date with respect to possible future events. Actual results may differ materially.

FLI believes the information contained herein to be reliable as of the Publication Date but does not warrant its accuracy or completeness. This communication is subject to modification, change, or supplement without prior notice to you. Some of the data presented in and relied upon in this document are based upon data and information provided by unaffiliated third-parties and is subject to change without notice.

NO ASSURANCE CAN BE MADE THAT PROFITS WILL BE ACHIEVED OR THAT SUBSTANTIAL LOSSES WILL NOT BE INCURRED.

Copyright © 2026 by First Long Island Investors, LLC. All rights reserved.

Colliding economic policies. Positive equity returns in 2025. More to come?

“The individual investor should act consistently as an investor and not as a speculator. This means … that he should be able to justify every purchase he makes and each price he pays by impersonal, objective reasoning that satisfies him that he is getting more than his money’s worth for his purchase.” – Benjamin Graham

2025 absorbed a new political administration as well as seemingly colliding economic policies, bookended by unusually severe and unprecedented tariffs and major tax reform that passed by the slimmest of political majorities in the House of Representatives and Senate. At the same time, in 2025, inflation actually moderated versus expectations despite increasing tariffs, while interest rates continued to decline slowly. In addition, geopolitical strife led to the unprecedented U.S./Israeli attack on Iran’s nuclear capability, as well as an attempt at brokering peace in the Middle East along with isolating Iran and attenuating its terrorist activities both directly and indirectly through its proxies. Meanwhile, the brutal war between Russia and Ukraine continues despite efforts at achieving a peace accord or cease fire led by the Trump Administration. Adding fuel to this geopolitical uncertainty, the United States, through the military and FBI, took action, destroying alleged drug smuggling boats from Venezuela, undertaking a nighttime, large-scale attack on the country, and arresting Venezuelan President Nicolás Maduro and his wife, both of whom are under indictment in the United States for narco-terrorism, among other charges.

At the same time, an explosion of capital investment in and development of artificial intelligence (AI) created a massive wave of interest in sophisticated semiconductors, data centers, and related infrastructure. This led, in a disproportionate manner, to a significant increase in equity markets through the earnings biased performance of the Magnificent 7 plus one (Broadcom) over a two-year period.

Large-cap growth companies, followed by large-cap value companies, led domestic equity markets higher. International stocks rallied even more (as suggested in last year’s Annual Thought Piece) reflecting in part the weakening U.S. dollar and most prominent foreign central banks reducing interest rates, as well as some European countries increasing military budgets to confront the unabashed aggression of Russia’s continued war against Ukraine.

- Despite record highs on Wall Street, returns were concentrated in a small group of outperformers. Failure to hug the concentrated performance of the AI-oriented companies led to the vast majority of active equity managers trailing their respective benchmarks, but still delivering positive results to their clients. FLI falls into this category of positive returns across all strategies not achieving their benchmarks. We trailed the benchmarks as a direct result of our disciplined risk management: namely, our decisions to not be overexposed to the concentrated cohort of mega-cap AI-related businesses and to avoid companies with negative earnings or extreme valuations.

- Despite our Dividend Growth strategy appreciating by 10.7% net* while achieving average dividend growth of 9.8%, many dividend aristocrats trailed the S&P 500® Index significantly because the likes of the Magnificent 7 plus a few others, either pay NO dividend or de minimis dividends of less than one half of one percent.

As we enter the investment environment for 2026, we offer the following charts for reflection:

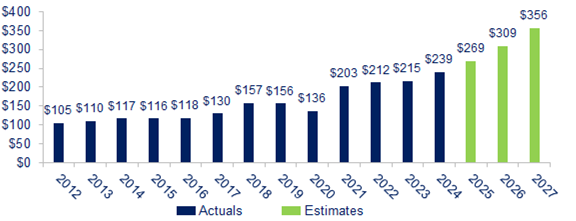

Exhibit 1: S&P 500® Index Earnings

Key Takeaway: 2026 Growth: Consensus points to approximately 15% earnings growth. 2027 Growth: Estimates suggest approximately 15% growth, potentially reaching $356.

Source: FactSet data as of 1/7/26

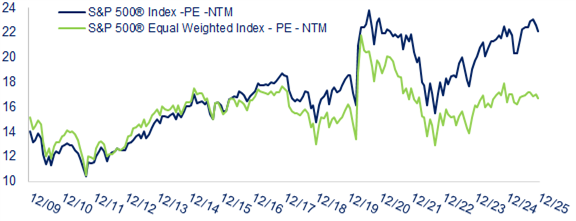

Exhibit 2: Price-to-Earnings Ratio

Key Takeaway: S&P 500® Index is trading at somewhat elevated levels (22x forward P/E although not extreme valuations), while the S&P 500® Equal Weighted Index (17x P/E) is much more reasonable.

Source: First Long Island Investors analysis, data as of 12/31/25

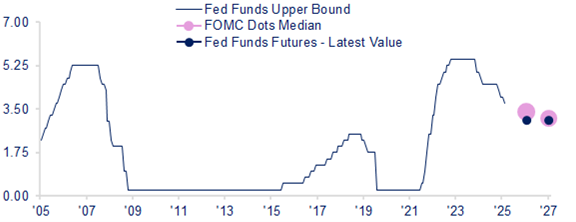

Exhibit 3: Market Expectations vs. Federal Reserve Forecasts

Key Takeaway: In 2026, the Federal Reserve forecasts fewer interest rate cuts compared to market expectations.

Source: Strategas Research Partners, Fed, Bloomberg, data as of 1/6/26

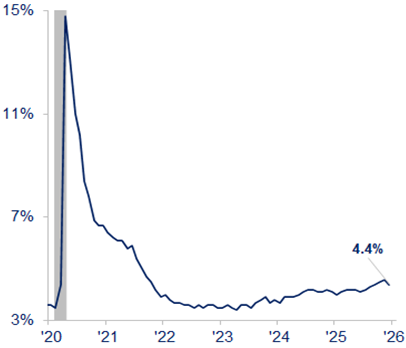

Exhibit 4: Civilian Unemployment Rate: 16 yr (Seasonally Adjusted, %)

Key Takeaway: The U.S. civilian unemployment rate (seasonally adjusted, 16 years and over) is currently 4.4% but still at historically normal levels.

Source: Strategas Research Partners, data as of 1/14/26

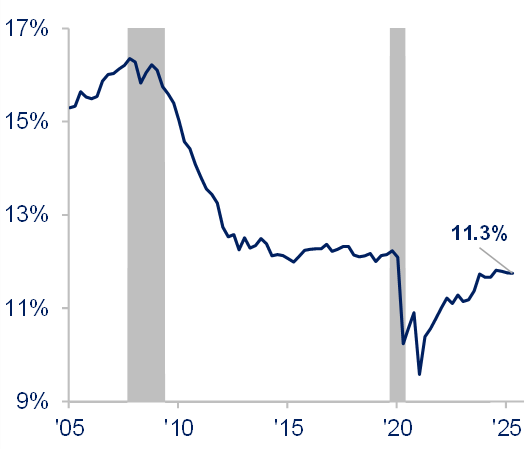

Exhibit 5: Household Debt Service Ratio (Seasonally Adjusted, %)

Key Takeaway: The Household Debt Service Ratio (DSR) is the ratio of total required household debt payments to total disposable income. DSR was 11.3%, which is inline with the long-term average (11.3% between 1980 and 2004exlcuding the housing bubble). This indicates that, relative to disposable income, the aggregate household debt burden is not historically high, despite the record absolute level of debt.

Source: Strategas Research Partners, data as of 6/30/25

Exhibit 6: U.S. Consumer Assets & Liabilities, Q3 2025

Key Takeaway: In Q3 2025, U.S. consumer balance sheets remained strong overall with record net worth driven by equities and real estate, but pockets of weakness emerged, especially in subprime auto and student loan delinquencies, alongside rising credit card struggles for lower-income groups.

Source: Federal Reserve Bank B.101 Table, Strategas, data as of 1/12/26

Exhibit 7: Manufacturers’ Shipments: Nondefense Capital Goods excluding Aircraft (Seasonally Adjusted, Mil $)

Key Takeaway: This metric (often called “core capital goods”) is crucial for GDP forecasts, as it measures spending on equipment for businesses, excluding volatile transportation. The chart indicates strong business investment, with shipments and orders rising, suggesting healthy Q4 economic activity.

Source: Strategas Research Partners, data as of 10/31/25

The above, when taken as a whole, indicates a reasonably accommodative investment environment. This is especially the case when one considers the impact of the “Big beautiful/ugly tax bill” of 2025 (the One, Big, Beautiful Bill Act). We view it as a positive on balance given the tax relief to many consumers through the expanded SALT deduction; liberalization of tax policies on tips, overtime, and Social Security benefits; an increased child tax credit; and deductibility of car loan interest. These features should bolster consumers, particularly at the lower rungs of the economic ladder, while businesses should benefit from incentives through immediate depreciation of eligible capital expenditures and immediate expensing of domestic research and development, fueling efforts to onshore manufacturing and bolster AI investment.

Summarizing the above, despite the political acrimony and upcoming midterm elections, there appears to be economic prosperity on the horizon in 2026. We still do not see a recession for 2026 and would agree with notable economic forecasts of GDP growth of at least 2%!

Our cautionary note is that not all companies have attractive valuations. The law of “bigness” may dull the equity performance of some of the hyperscalers despite their continued earnings growth. We witnessed substantial volatility in 2025 where some companies that barely achieved lofty Wall Street estimates or even exceeded them, were still punished with significant drops in their stock prices.

The Fear/Greed Index, which we often cite, ended the year on the cusp of fear and neutral while gyrating between extreme fear and greed during the year. This is especially the case when several notable pundits and industry insiders cry “bubble” around AI and technology in general. These include some successful investors and certain respected measures of valuation like the CAPE (Cyclically Adjusted Price-to-Earnings), which we do not subscribe to as a reliable valuation measure.

Our view remains one of cautious optimism. Earnings are growing; consumer balance sheets are solid; inflation is reasonable; tariff damage is likely modest in general; and tax relief should be coming while price-to-earnings multipliers are not nosebleed. These factors should all support the possibility of growing our assets again in 2026. In addition, although we believe the labor market will somewhat weaken, it will permit the Fed to respond in an accommodative manner. Some publicly traded equities along with some, but not all, private equity as well as some segments of real estate should all be beneficiaries.

The positives outweigh the negatives in our opinion. Having said that, one must revisit their asset allocation and adjust where necessary when some allocations may have risen too far in pure growth assets to be prudent from a risk/reward standpoint. Our straightforward, but successful, “bookend” approach continues to deliver reasonable returns through different stages of the business cycle. Our four investment baskets (Security, Defensive, Traditional Equity, and Private Investments) must be reviewed as we enter 2026 to reflect your goals as well as fears. Compounding wealth over time requires a prudent asset allocation that limits the damage of unforeseen market drawdowns.

Despite coming through a strange and complex 2025, we enter 2026 having achieved meaningful investment gains. We face what appears to be a solid economy, although we have concerns over health insurance costs adding to inflation and consumer distress. Bipartisan legislation is needed to address a potential health insurance crisis. Additionally, wealth inequality needs to be confronted through wage gains above inflation as well as possible further tax reform. Reform that incentivizes investment and working needs to be a priority while also recognizing the need to safeguard both our Social Security and Medicare systems.

Most importantly, investors should counsel with us to review their asset allocations and explore wealth planning to weather what might be a volatile year given the midterm elections, the path of the Federal Reserve with a new Chair, continued geopolitical unrest in Europe and the Middle East, the simmering relationship between the U.S. and China, and questions about the U.S.’s future role in Venezuela.

Historically, midterm election years have seen significant volatility prior to the election, followed by rising markets into the following year. Thus, patience, as an investor, is always required to let earnings and cash flow drive performance:

Exhibit 8: S&P 500® Index Average Annual Price Returns

by Presidential Cycle

Key Takeaway: Key takeaways from the S&P 500® Index presidential cycle chart shows that, while midterm election years have historically produced positive returns, on average, returns are typically more muted than other years in the cycle.

Source: Strategas Research Partners, data as of 1/6/25

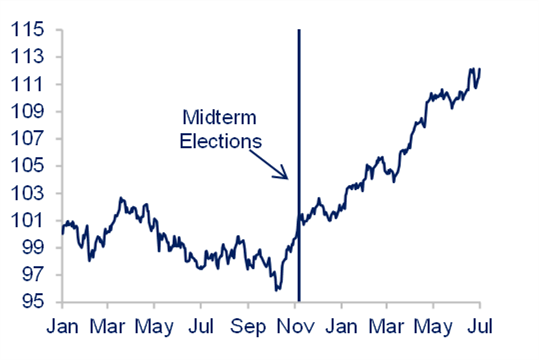

Exhibit 9: Average S&P 500® Index Performance Before & Following Midterm Elections (1994, 1998, 2002, 2006, 2010, 2014, 2018, 2022)

Key Takeaway: Historical patterns suggest volatility is likely leading up to the November 2026 elections, which is typically followed by a strong rally into year-end and the following year.

Source: Strategas Research Partners, data as of 1/6/25

Our bottom line remains bookending growth-oriented companies with value-oriented, dividend-growing companies. Within equities, one should maintain some exposure to internationally-domiciled companies while small- and mid-cap companies that have real earnings might finally get rewarded as they have lagged. Clients should also maintain modest exposure to fixed income to provide income and for protection during turbulent times. Certain real estate, especially industrial, remains attractive as short-term interest rates continue to modestly decline and onshoring efforts reflect recent administration achievements while the AI boom continues. Reduced onerous tariffs on food, decreased oil prices (and who knows what further downward pressure will result from a revitalization of Venezuelan oil reserves), and pharma company agreements on drug pricing should help keep a lid on inflation. Of course, medical insurance premiums must be dealt with politically.

We view 2026 with some optimism as earnings and interest rates should support the progress of good companies, both public and private, and well-situated real estate. The consumer remains resilient and both fiscal and monetary policies appear not to be colliding. As mentioned earlier, given reasonably full equity valuations, quality individual stock picking with some diversified allocations (including some exposure to international and small/mid-cap) should pay off for the patient investor.

We, as investors, should approach 2026 with the understanding that after three solid years of results, a new political administration, serious geopolitical issues, a midterm election looming, the One, Big, Beautiful Bill Act offering wealthy investors some greater opportunity, and the advent of AI, it is a time for reflection on what is to come and what we should do while always being conscious of risk. Consider that gold, silver, and bitcoin have also risen dramatically in the last three years alongside equities and certain real estate. This surge in alternative assets likely reflects mounting concern over the U.S. national debt, which has now climbed to nearly $38 trillion. We should not take our wealth for granted, which is why we, at First Long Island Investors, offer a customized “bookend,” high-quality, almost exclusively unlevered approach to each of our clients. We do this to afford our clients the opportunity to grow assets while feeling some protection from the unknowns in the future investment landscape. As previously stated quite clearly, we remain cautiously optimistic.

Our unique approach was recognized this past year by InvestmentNews awarding First Long Island Investors a 5-Star rating as one of the top twenty-seven registered investment advisers in the United States in 2025. We were both flattered and humbled by this designation and take it very seriously. We accordingly must do even more for our clients to continue to earn their respect and confidence. Certainly, as we enter our 43rd year in business, our experiences, client-oriented culture, and team of talented and dedicated professionals puts us in a position to represent you going forward.

We look forward to working with each of you, our clients, this year and in the coming years to keep compounding your wealth while being best positioned for the future. Please call upon us with any of your wealth and money management needs, or just as someone you can speak with who has your back.

We look forward to working with you this year and thank you again for your continued confidence.

Healthy, happy and prosperous New Year!!

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

DISCLAIMER

The views expressed herein are those of Robert D. Rosenthal or First Long Island Investors, LLC (“FLI”), are for informational purposes, and are based on facts, assumptions, and understandings as of January 15, 2026 (the “Publication Date”). This information is subject to change at any time based on market and other conditions. This communication is not an offer to sell any securities or a solicitation of an offer to purchase or sell any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Nothing herein should be construed as a recommendation to purchase any particular security. The companies and securities described herein may not be held in every (or any) FLI strategy at any given time. Investment returns will fluctuate over time, and past performance is not a guarantee of future results.

This communication may not be reproduced, distributed, or transmitted, in whole or in part, by any means, without written permission from FLI.

All performance data presented throughout this communication is net of fees, expenses, and incentive allocations through or as of December 31, 2024, as the case may be, unless otherwise noted. Past performance of FLI and its affiliates, including any strategies or funds mentioned herein, is not indicative of future results. Any forecasts included in this communication are based on the reasonable beliefs of Mr. Rosenthal or FLI as of the Publication Date and are not a guarantee of future performance. This communication may contain forward-looking statements, including observations about markets and industry and regulatory trends. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect the views of the author as of the Publication Date with respect to possible future events. Actual results may differ materially.

FLI believes the information contained herein to be reliable as of the Publication Date but does not warrant its accuracy or completeness. This communication is subject to modification, change, or supplement without prior notice to you. Some of the data presented in and relied upon in this document are based upon data and information provided by unaffiliated third-parties and is subject to change without notice.

NO ASSURANCE CAN BE MADE THAT PROFITS WILL BE ACHIEVED OR THAT SUBSTANTIAL LOSSES WILL NOT BE INCURRED.

Copyright © 2026 by First Long Island Investors, LLC. All rights reserved.

Robert D. Rosenthal (left), Kevin J. Tracey MD (right)

First Long Island Investors, LLC (FLI) has long maintained strong ties to Long Island, reflecting our deep commitment to the surrounding communities and institutions we serve. Through our philanthropic and thought leadership initiatives, FLI actively supports the healthcare community, recognizing the critical role it plays in advancing public health, innovation, and patient care across the region. In keeping with that theme, FLI recently welcomed Dr. Kevin Tracey, a distinguished medical innovator, as the featured guest for our Thought Leadership Breakfast at the Garden City Hotel on October 28, 2025. During the event, Dr. Tracey shared his journey from neurosurgeon to pioneer in bioelectronic medicine, exploring how the vagus nerve can be harnessed to treat chronic inflammation and disease. As a neurosurgeon, scientist, and entrepreneur, he leads research into how the vagus nerve regulates the immune system and inflammation. He holds more than 120 U.S. patents and is among the most-highly cited living scientists. His new book The Great Nerve: The New Science of the Vagus Nerve and How to Harness Its Healing Reflexes, outlines how tiny bioelectric implants and lifestyle strategies like meditation and breath work may transform treatment for conditions from rheumatoid arthritis to Alzheimer’s disease.

Dr. Tracey began by highlighting a fundamental truth: the world resists change. While everyone seeks innovation, few are willing to embrace disruption. Drawing on his experience developing a neural implant designed to treat inflammatory diseases, he discussed the challenges of overcoming adoption barriers and reshaping long-held medical paradigms.

He traced the evolution of medical research, noting that while decades of work have yielded life-changing discoveries, roughly 90% of all studies fail. Still, the mission remains clear: to produce knowledge that can cure diseases and relieve human suffering. Because traditional institutions like the NIH are often risk averse in grantmaking, he emphasized the crucial role philanthropy plays in funding early, high-risk breakthroughs.

Dr. Tracey drew parallels between the twentieth century war on infection and today’s efforts to understand inflammation. Vaccines and germ theory once added fifteen years to average lifespans by eradicating infectious diseases. He posed a provocative question: What if we could do for inflammation what we did for infection? Discoveries such as blocking TNF (tumor necrosis factor) have already led to anti-inflammatory drugs generating over thirty billion dollars annually, but many patients still see limited results.

That gap inspired a new approach targeting the vagus nerve, which connects the brain to the body and regulates key organs and immune responses. Described as the “brakes” of the nervous system, the vagus nerve helps control inflammation. Dr. Tracey’s company SetPoint Medical has developed an FDA approved, implantable, computerized stimulator that communicates with the brain to restore balance. Early trials have shown that over eighty percent of patients experienced improvement, marking a potential paradigm shift in medicine.

For the first time, MRI scans have shown arthritic joints beginning to heal, an unprecedented outcome made possible through neuromodulation rather than pharmaceuticals. Dr. Tracey concluded by noting that this breakthrough represents not just a new device but a new way of thinking about medicine itself. With continued collaboration among doctors, researchers, and patients, bioelectronic medicine could redefine how humanity treats disease in the decades to come.

FLI remains committed to offering clients timely insights from top industry experts and thought leaders through the FLI Thought Leadership Breakfast series. We thank Dr. Kevin Tracey for sharing his perspective and expertise on the topic of healthcare.

“In investing, what is comfortable is rarely profitable.” Robert Arnott

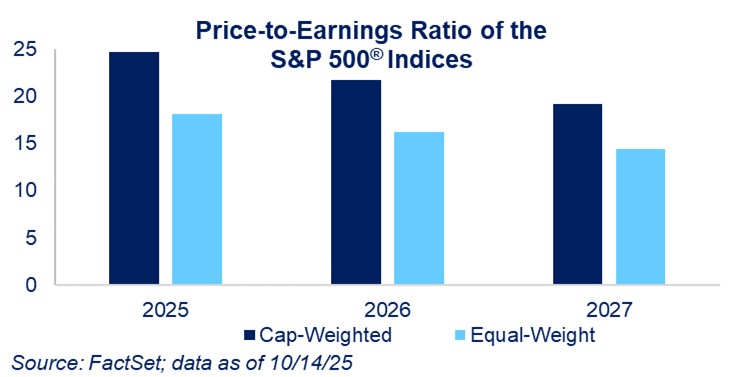

Reasonable gains were achieved across all of our strategies in the third quarter despite crosscurrents from tariffs, uncertainty about the number of Federal Reserve interest rate cuts, a weakening labor market, and continued geopolitical strife. Growing corporate earnings, modest increases in inflation, largely caused by significant tariff increases, and the trend toward lower short-term interest rates all played a part in the gains achieved across different asset classes as did the unfolding growth story of artificial intelligence (AI). Bonds, large-cap growth and value stocks, international equities, gold, Bitcoin, and segments of the real estate market all participated in what proved to be a good quarter from an investor’s standpoint. Positive money flows also impacted segments of the market, as the third quarter recorded the strongest inflows so far this year and the second strongest quarter since 2020.

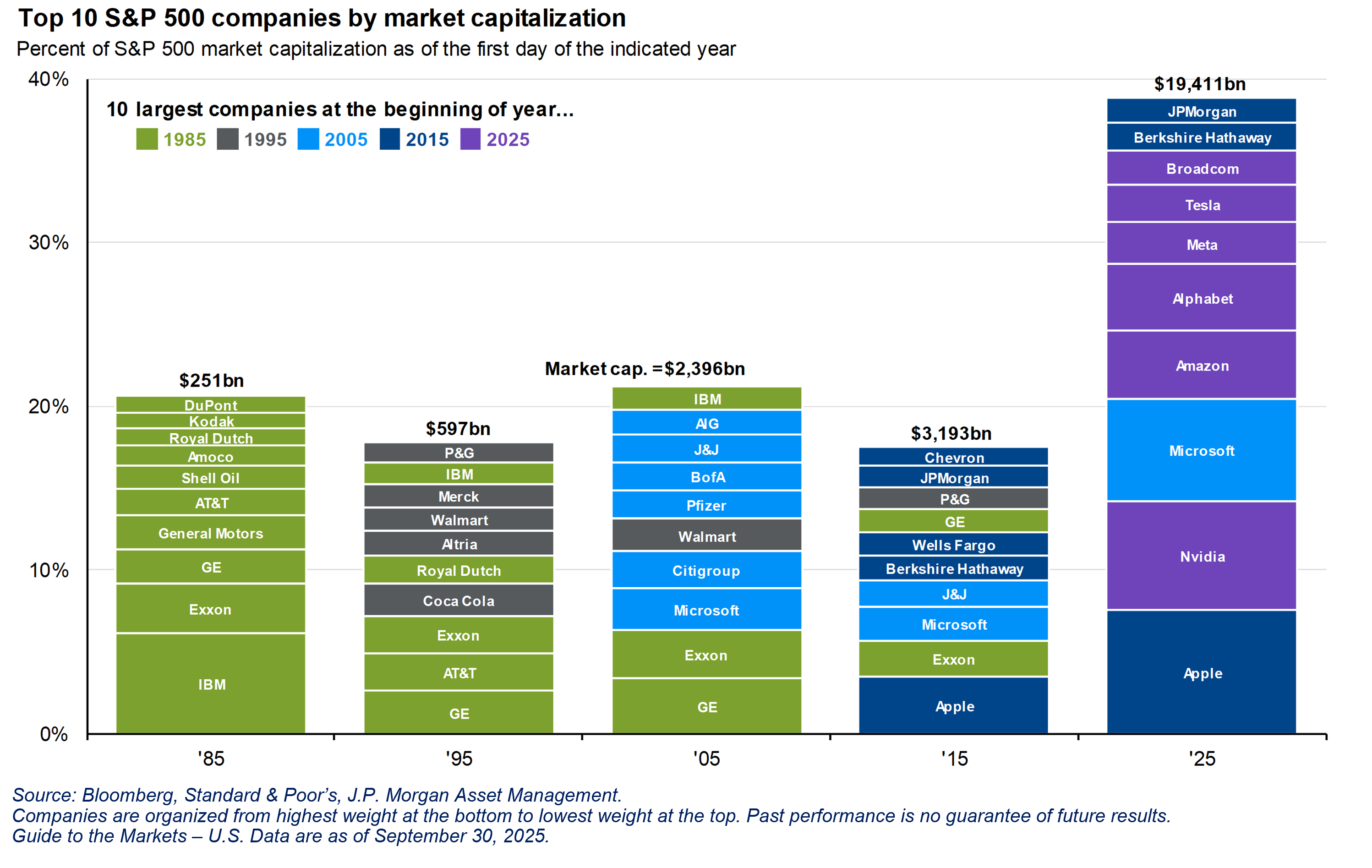

These gains for the quarter and year-to-date, however, do not come without a meaningful level of uncertainty. The continued narrowness of stock market gains (seven companies represent more than 35% of the S&P 500® Index), the depreciating dollar, seemingly high valuations for growth stocks, the full extent of inflationary forces from tariffs, and the potential economic return of the AI arms race are all contributing to an “unloved bull market” in investing. Gold and Bitcoin have achieved new record highs, making us wonder whether the growing national debt, new government policies, or a government shutdown are having a negative impact on our domestic currency. Historically, government shutdowns have not had a negative impact on equity markets. Add to this the continued political divide across our nation, which causes angst among investors.

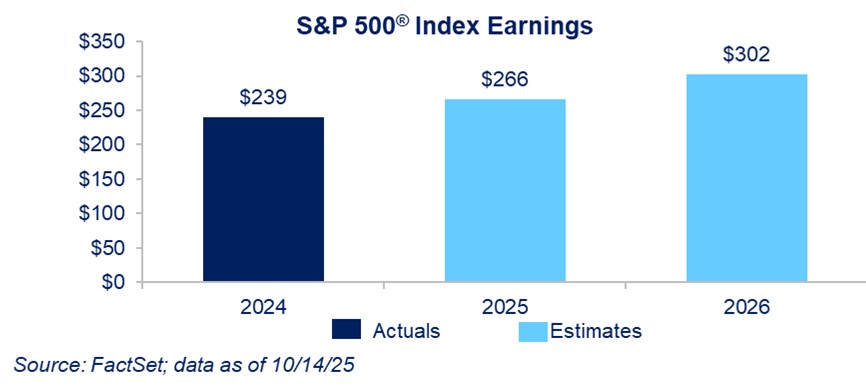

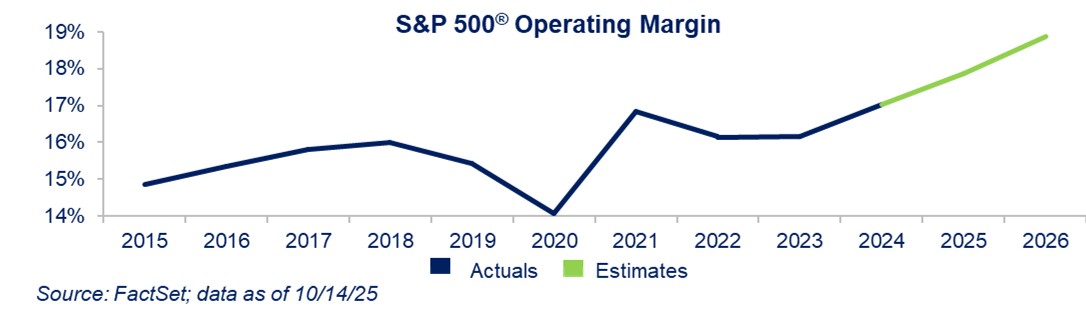

On the positive side, S&P 500® Index earnings continue to grow as profit margins expand:

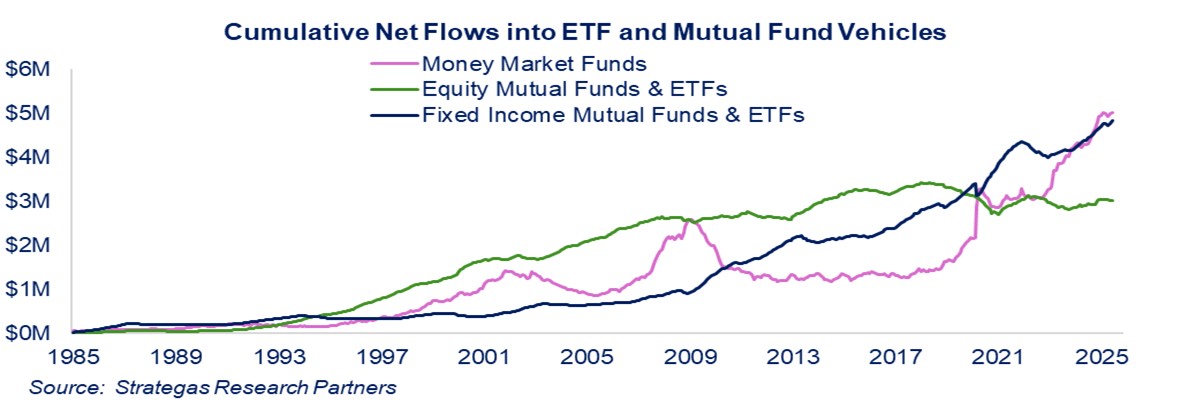

As you know from reading our reports over our almost 42 years of being in business, we rely on earnings and cash flow growth to be the backbone of capital appreciation. Whether it is the earnings of a company or the cash flow of real estate, that growth is required for sustainable appreciation, in our opinion, along with a reasonable level of interest rates, a combination essential for capital appreciation. Additionally, money flows can affect which asset class performs better over shorter periods:

We believe that, over the past few years, investors globally have allocated capital to various asset classes in differing amounts. Certainly, the disruptive technology of AI has led to certain growth companies seeing huge buying interest. Chipmaker NVIDIA has appreciated almost fifteen-fold over the past few years, and other companies in the AI space have followed suit, including Oracle and Broadcom (up 70% and 43% this year, respectively). Companies with cloud capabilities, including Amazon.com and Microsoft, have also been part of this tech revolution. These and other companies in the Magnificent Seven plus have contributed to significant appreciation in certain FLI strategies over the past two-plus years. Most recently, as referenced in our Annual Thought Piece in January, international investing has also seen strong money flows, contributing to the MSCI ACWI ex USA Index appreciating 23% year-to-date. We believe this strong international performance can be attributed in part to valuation, our depreciating dollar, uncertain and often erratic U.S. government policies (such as tariffs), and declining interest rates abroad, while certain European countries increase their defense spending leading to local economic growth.

Now the uncertainty we reference includes the following:

- How many rate cuts will the Federal Reserve implement?

- What direction will the interest rate on the 10-year U.S. Treasury take?

- How much inflation will result from the ultimate tariff rates?

- How high will unemployment rise, reflecting some economic slowdown and uncertainty?

- What benefits will the economy derive from the recent tax legislation passed by Congress?

- How and when will the geopolitical hotspots in Europe and the Middle East be resolved?

- Are valuations stretched for certain segments of the equity market?

The uncertainty described above makes it difficult for investors to navigate the current investment landscape. We believe the Fed will continue to reduce short-term interest rates several times over the next year. At the same time, history suggests that does not mean the 10-year U.S. Treasury will decline, unless inflation really abates. The direction of the 10-year U.S. Treasury is very important to the housing market, as it is what the interest rates for mortgages are based on. It is our opinion that the Fed’s prediction of lower inflation in 2026 and 2027 (Personal Consumption Expenditures Price Index (PCE) advancing 2.6% and 2.1%, respectively) in large part depends on the accuracy of the Fed’s prediction of slower gross domestic product growth of 1.6% this year and 1.8% next year. The current Administration would expect somewhat higher growth and, perhaps, the recent tax bill will help achieve that. At the same time, the Fed expects unemployment to reach 4.5%, which would not be too harsh. In our view, the comprehensive tax bill of 2025 will benefit business by inducing investments in technology and manufacturing, given depreciation incentives. Perhaps this will aid employment, although the labor supply has diminished due to the country’s current immigration policies. We are sure both sides of the aisle would love to see legal immigration reform, but it has been elusive for decades.

Regarding the geopolitical turmoil in both the Middle East and Europe, despite President Trump’s attempts to seek peace, that too has been elusive. At this point, Russia’s President Putin seems uninterested in a cease-fire or peace deal with the country he illegally invaded. This assertion is based on the 1994 Budapest Memorandum on Security Assurances treaty signed by Russia, in which Ukraine gave up its nuclear weapons. This ongoing war has cost the U.S. significantly, while also boosting our exports of munitions. The other war, in the Middle East, has seen Iran’s nuclear ambitions set back by a joint American/Israeli attack and the severe weakening of two of Iran’s terrorist proxies, Hezbollah and Hamas. Meanwhile, innocent hostages remain captive; Israel remains at war with Hamas; and the people of Gaza continue to suffer. Neither of these two wars is good for the world. (See P.S. for update)

Given these positives (growing earnings, potentially lower short-term interest rates, no recession in sight, and favorable tax policy), we continue to see an economy growing but at a slower pace; positive S&P 500® Index earnings growth; inflation somewhat above the Federal Reserve’s goal of 2%; and, unfortunately, a continuation of geopolitical strife. Add to this our own political divisiveness and rising extremism, which shows no signs of abating and has most recently led to violence in the form of political attacks and assassinations across the political spectrum.

As investors, we remain cautiously optimistic as the AI revolution fuels not only certain growth companies, but much of our daily lives; international investing remains robust; more value-oriented companies, as reflected in our Dividend Growth strategy, remain a safer harbor in our opinion (+12.1% net* year-to-date); and we would not be surprised to see small- and mid-cap companies play catch-up to large-cap growth and value companies if interest rates moderate:

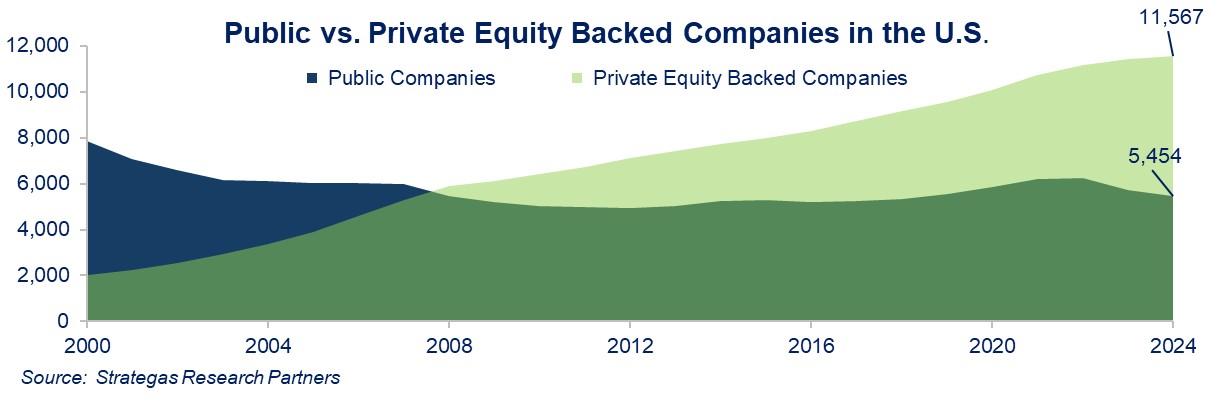

Another factor that we consider a positive from a long-term standpoint is the above chart showing the reduced number of public companies as compared to twenty years ago. At the same time, the proliferation of exchange-traded funds and index funds offer investors different ways to invest in the smaller pool of public companies. Private equity backed companies, on the other hand, have grown in number significantly. They are illiquid but might offer handsome returns.

The bottom line continues to be, in our view, maintaining our bias to high-quality, financially strong companies, through the book ends of both large-cap dividend growing companies along with large-cap growth companies, especially those participating in the cloud computing and booming AI trends. Having exposure to both quality international-domiciled companies and small- and mid-cap companies also makes sense as short-term interest rates are expected to decline. Of course, in this latest allocation, we emphasize companies with real earnings. We also believe that nearly every client should have some exposure to fixed income and alternatives (including real estate), especially as some believe equity valuations are stretched. It is this multifaceted asset allocation that will make investing, when it is somewhat uncomfortable given the enumerated uncertainties, profitable for the long term.

Our various investment strategies allow each of you to work with us to customize your asset allocations to achieve your long-term goals. Within the asset classes we have mentioned, we believe we can find quality opportunities with attractive earnings growth, cash flows, and reasonable valuations for the long-term investor.

We are pleased to announce two significant achievements. FLI has been awarded a 5-Star rating from InvestmentNews as one of the top 27 registered investment advisers in the United States in 2025! Additionally, we are proud to share that Thérèse C. Vobis, our Senior Vice President of Finance & Administration and Chief Financial Officer, has been selected as a recipient of the Long Island Business News Top 50 Women in Business award. Both honors reflect our dedication to you, our clients, and friends of the firm, as well as your confidence and loyalty, making this very special recognition possible.

Please enjoy the upcoming holiday season and stay healthy. Of course, do not hesitate to contact us should you or members of your family or friends have any wealth management needs, whether that includes investing, asset allocation, liquidity needs, insurance, tax or estate planning.

P.S. As of October 13, 2025, all living Israeli hostages have been returned to Israel, while only several of the deceased hostages have been repatriated. Approximately two-thousand Palestinian detainees have been emancipated, and a 20-point Trump peace plan is currently under consideration by a large number of Western and Middle Eastern countries. Whether this marks the end of the war between Hamas and Israel remains to be seen.

DISCLAIMER

The views expressed herein are those of Robert D. Rosenthal or First Long Island Investors, LLC (“FLI”), are for informational purposes, and are based on facts, assumptions, and understandings as of October 24, 2025 (the “Publication Date”). This information is subject to change at any time based on market and other conditions. This communication is not an offer to sell any securities or a solicitation of an offer to purchase or sell any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Nothing herein should be construed as a recommendation to purchase any particular security. The companies and securities described herein may not be held in every (or any) FLI strategy at any given time. Investment returns will fluctuate over time, and past performance is not a guarantee of future results.

This communication may not be reproduced, distributed, or transmitted, in whole or in part, by any means, without written permission from FLI.

All performance data presented throughout this communication is net of fees, expenses, and incentive allocations through or as of September 30, 2025, as the case may be, unless otherwise noted. Past performance of FLI and its affiliates, including any strategies or funds mentioned herein, is not indicative of future results. Any forecasts included in this communication are based on the reasonable beliefs of Mr. Rosenthal or FLI as of the Publication Date and are not a guarantee of future performance. This communication may contain forward-looking statements, including observations about markets and industry and regulatory trends. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect the views of the author as of the Publication Date with respect to possible future events. Actual results may differ materially.

FLI believes the information contained herein to be reliable as of the Publication Date but does not warrant its accuracy or completeness. This communication is subject to modification, change, or supplement without prior notice to you. Some of the data presented in and relied upon in this document are based upon data and information provided by unaffiliated third-parties and is subject to change without notice.

NO ASSURANCE CAN BE MADE THAT PROFITS WILL BE ACHIEVED OR THAT SUBSTANTIAL LOSSES WILL NOT BE INCURRED.

Copyright © 2025 by First Long Island Investors, LLC. All rights reserved.