“The big money is not in the buying and the selling, but in the waiting.“ Charlie Munger

The first quarter was marked by significant volatility, driven by a number of factors, which we foreshadowed in both January’s Annual Investment Outlook and a recent market update email. These historical and current factors, which, in our opinion, have negatively impacted equity, fixed-income, and real-estate markets for the short term, include the following:

1) Ongoing uncertainty in U.S. policy, including tariffs, immigration, foreign policy, and affordability.

2) Two avoidable government shutdowns, one of which continues as of this writing.

3) The historical trend of midterm election years being volatile, with equity drawdowns during those years averaging 19%, until after the midterm election, following which markets tend to recover.

4) The outbreak of a hot war involving the U.S. and Israel versus the theocratic driven Iran.

5) The spike in energy costs resulting from Iran’s apparently illegal closing of the Strait of Hormuz.

6) Uncertainty regarding the direction of interest rates, which for now have risen by about 10% for the 10-year U.S. Treasury (or 38 basis points), impacting mortgage rates.

7) Questions about how beneficial the One Big Beautiful Bill Act of 2025 will be for the domestic economy, given significant business breaks and reduced taxes for certain individuals from the easing of limitations on the SALT deduction as well as other deductions, including breaks on tips, Social Security income, and overtime wages.

8) The projected robust increase in earnings for the S&P 500® Index for 2026 and 2027.

9) The evolving phenomenon of artificial intelligence (AI) and its implications.

Let us begin by examining what has historically occurred during periods of significant “policy uncertainty” from the U.S. government as evidenced by both domestic and geopolitical actions:

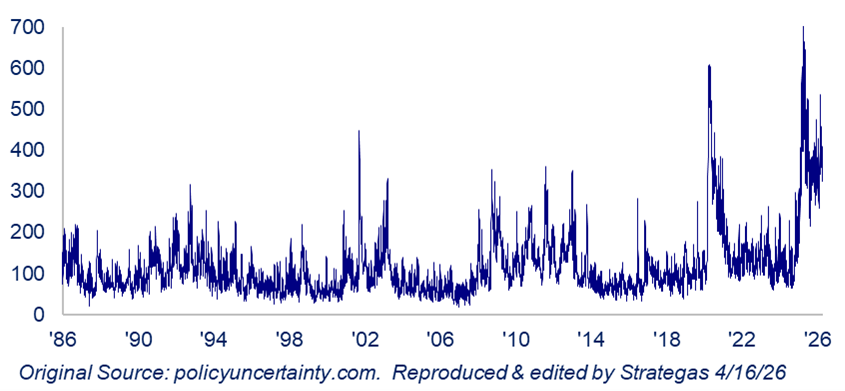

| Exhibit 1: U.S. Policy Uncertainty Daily Index (7-Day Moving Average) Key Takeaway: Policy uncertainty is highly event-driven, marked by sharp spikes rather than steady trends. |

As you can see, uncertainty that began last year with the ever-changing tariff policy eventually receded, but has now intensified again due to the war in the Middle East, government shutdowns, and ongoing tariff changes. The following chart demonstrates that, historically, periods of extreme policy uncertainty have often been followed by sizable returns for the S&P 500® Index:

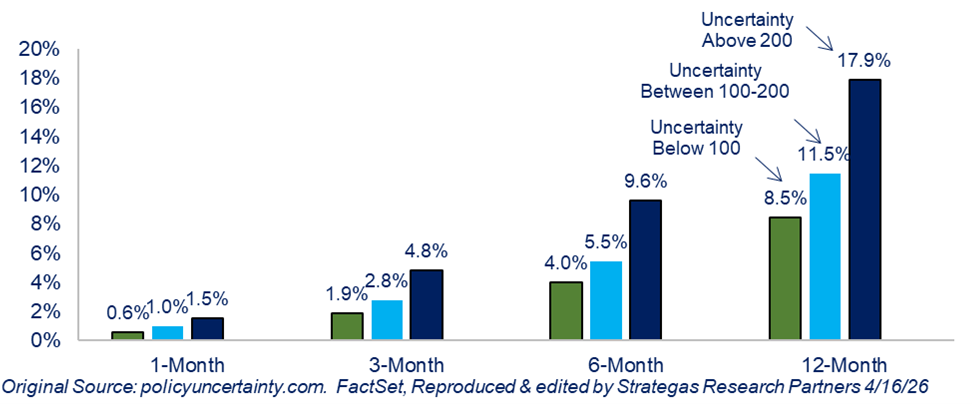

| Exhibit 2: S&P 500® Index Returns Following Spikes In U.S. Policy Uncertainty (Using Daily Policy Uncertainty Index: January 1985 – April 16, 2026) Key Takeaway: Markets typically absorb policy shocks quickly, with S&P 500® Index returns stabilizing or improving after uncertainty spikes. |

This chart demonstrates that following periods of extreme uncertainty, equity markets have returned an average of 18% one year later (for the period of March 1985 through March 2026). With growing earnings, which we will address a bit later, we remain cautiously optimistic that history may repeat itself.

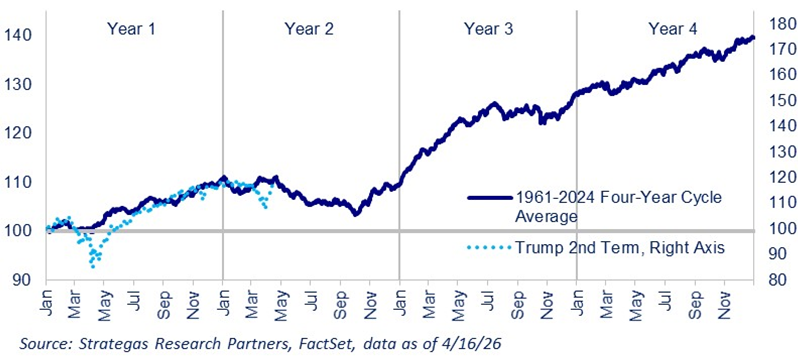

Historically, midterm election years are volatile and tend to produce the poorest returns for stocks within a typical four-year Presidential term. The following chart shows the historical performance during the four-year term, dating back to 1961:

| Exhibit 3: Average S&P 500® Index Price Returns During Four-Year Presidential Cycle (1961-2024) Key Takeaway: The S&P 500® Index presidential cycle shows a repeatable pattern of weakness in Year 2, strength in Year 3, and attractive, but moderate gains, in Year 4, however it should be viewed as a statistical tendency—not a predictive tool. |

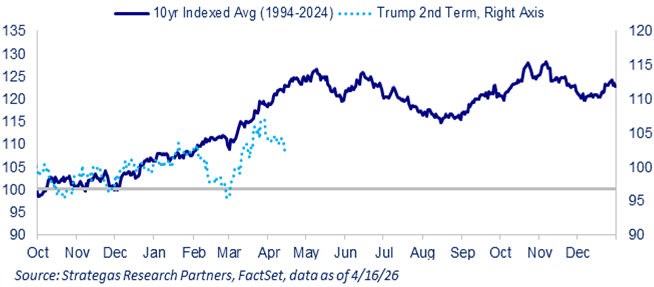

The above chart illustrates our earlier point: year two, the midterm election year, typically brings volatility and market drawdowns until the midterm, followed by a significant recovery post-election and into the third year of a presidential term. At the same time, we believed that interest rates for the 10-year U.S. Treasury would likely rise temporarily before stabilizing. This trend is playing out as we write this report.

| Exhibit 4: Average 10-Year Yield (Indexed) From October of Year 1 Through Year-End Year 2 Of Presidential Cycle (1994-2024) Key Takeaway: The pattern shows that the 10-year U.S. Treasury yield tends to enter a “re-pricing and confirmation phase” during the early-to-mid presidential cycle, where direction is driven less by politics and more by inflation and growth expectations. |

Interest rates are critically important, especially as we face the likely replacement of current Federal Reserve Chairman Jerome Powell at the end of his term. The balance between inflation protection and full employment is being tested in light of rising energy costs from the Middle East conflict and concerns that AI could replace large numbers of employees. Yet, higher S&P 500®Index earnings, including the presumed benefits from a robust tax law, suggest employment stability, in our view. Higher interest rates from the Federal Reserve were detrimental to stocks in 2022; however, we do not expect the Federal Reserve to raise rates anytime soon. While the market expectation for a reduction of two short-term rate cuts in 2026, based on consensus estimates at the end of 2025 may not materialize, even a single rate cut by the end of the year could boost stocks, given the projected increase in profits:

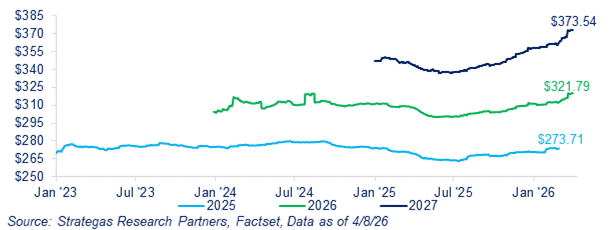

| Exhibit 5: 2025 vs. 2026 vs. 2027 S&P 500® Index Earnings Per Share Progression Key Takeaway: Earnings growth expectations sit in the 16-17% range for this year and next. |

This robust projection of improving corporate earnings is impressive. However, we would not be surprised if these projected earnings are revised downward somewhat over time, and yet they still give us reason for optimism. In an environment with less policy uncertainty and stable interest rates, we believe equities will recover toward the end of the year, following historical patterns.

Of course, the ongoing war in the Middle East as of March 31, 2026 is sobering for investors, as spiking oil costs are likely to impact inflation, at least temporarily. This oil shock has led our outside economics advisor to somewhat increase the odds of recession, though we do not believe this shock will cause one. The impact on stocks has been notable; the average stock in the S&P 500® Index has declined by 21% from its highs, while the index itself has only fallen about 9%:

| Exhibit 6: S&P 500® Index Average Stock % Decline From 52 Week High Key Takeaway: Average stock decline in the S&P 500® Index is -21%, despite the headline index falling just -9% |

The bottom line is that the declines investors are experiencing are steeper than what the index itself reflects, as the S&P 500® Index drop from its highs earlier in January understates the average stock’s losses. If Iran’s stranglehold on the Strait of Hormuz persists for months, the resulting increase in global inflation could be more significant and prolonged.

To summarize:

In January’s Annual Investment Outlook, we highlighted the historical “chop” and typical market correction that often occurs during a midterm election year. Since then, areas of concern have mounted: the continuing partial government shut down; ongoing tariff re-regulation (new tariffs recently announced on certain pharmaceuticals); uncertainty surrounding the potential replacement of Federal Reserve Chairman Jerome Powell; questions about the direction of interest rates; the Iran war given energy’s impact on inflation; and the evolution of AI and its implications for investment, productivity, and employment. Additionally, the current strain between the U.S. and its NATO allies is troubling, as many NATO countries are not supporting the war against Iran, a conflict with consequences that are hurting their economies, not to mention the broader threat Iran poses to global peace, in my opinion.

On the positive side, the forecasted robust rise in S&P 500® Index earnings, the presumed favorable impact of the One Big Beautiful Bill Act of 2025, and productivity gains from the build out of AI. Stock prices have declined, in our opinion, all contribute to compression of price-earnings multiples, while earnings for many companies have increased. This volatility has allowed value stocks, including our Dividend Growth strategy, to perform better than growth-oriented companies for now. For example, the Magnificent 7 are down on average 12%, despite rapidly growing earnings for most, if not all. We expect this trend to reverse as earnings continue to grow throughout the year.

2026 will be a challenging year for investors, but we believe returns will improve as uncertainty diminishes, and we are confident that it will. We also expect energy prices to recede and inflation to rise, though not substantially. However, much depends on the duration of the energy shock caused by spiking oil prices. In our view, the Federal Reserve will not raise rates, and while gross domestic product (GDP) growth may slow, we do not anticipate a recession. We also believe that history will repeat itself, with meaningful equity gains from this point forward, and that business will return to a more normal environment for real estate and capital markets.

Whatever the outcome of the midterm elections, it will provide a degree of certainty compared to where we stand now. Investors value certainty, and with a Republican in the White House, even if both Houses flip to the Democrats, significant new policy changes are unlikely in the foreseeable future.

So, we advise against emotional reactions. Sit tight with the customized diversification we recommend, which encompasses exposure to our four investment baskets that typically favors our defensive basket. Let earnings and dividend growth play out this year, leading to even better valuations, especially for quality companies. Over the long term, that is what matters. Hopefully, the war in Iran will resolve in weeks rather than months, and Iran will cease to pose the threat to global peace that has troubled the last four Presidents from both parties.

Finally, we believe that AI is real and will help the free world evolve from a technical, medical, and productivity standpoint, benefitting all of us, hopefully without significant negative impact on employment. However, there will be business winners and losers, with some companies gaining tailwinds and others facing headwinds from AI adoption. Our job is to be patient and careful in our stock selection. The one risk we will monitor closely is the overall impact of elevated energy costs on inflation and how long that effect will last.

Please do not hesitate to call anyone on our investment or wealth management committees should you have any questions.

Have a great spring!

Robert D. Rosenthal

Chairman, Chief Executive Officer and Chief Investment Officer

DISCLAIMER

The views expressed herein are those of Robert D. Rosenthal or First Long Island Investors, LLC (“FLI”), are for informational purposes, and are based on facts, assumptions, and understandings as of April 24, 2026 (the “Publication Date”). This information is subject to change at any time based on market and other conditions. This communication is not an offer to sell any securities or a solicitation of an offer to purchase or sell any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Nothing herein should be construed as a recommendation to purchase any particular security. The companies and securities described herein may not be held in every (or any) FLI strategy at any given time. Investment returns will fluctuate over time, and past performance is not a guarantee of future results.

This communication may not be reproduced, distributed, or transmitted, in whole or in part, by any means, without written permission from FLI.

All performance data presented throughout this communication is net of fees, expenses, and incentive allocations through or as of March 31, 2026, as the case may be, unless otherwise noted. Past performance of FLI and its affiliates, including any strategies or funds mentioned herein, is not indicative of future results. Any forecasts included in this communication are based on the reasonable beliefs of Mr. Rosenthal or FLI as of the Publication Date and are not a guarantee of future performance. This communication may contain forward-looking statements, including observations about markets and industry and regulatory trends. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect the views of the author as of the Publication Date with respect to possible future events. Actual results may differ materially.

FLI believes the information contained herein to be reliable as of the Publication Date but does not warrant its accuracy or completeness. This communication is subject to modification, change, or supplement without prior notice to you. Some of the data presented in and relied upon in this document are based upon data and information provided by unaffiliated third-parties and is subject to change without notice.

NO ASSURANCE CAN BE MADE THAT PROFITS WILL BE ACHIEVED OR THAT SUBSTANTIAL LOSSES WILL NOT BE INCURRED.

Copyright © 2026 by First Long Island Investors, LLC. All rights reserved.