The Internal Revenue Code recently underwent its first major tax overhaul since 1986. In an attempt to stimulate the national economy, The Tax Cuts and Jobs Act of 2017 was passed in December of 2017 and impacts taxpayers starting in 2018. On May 23, 2018 First Long Island Investors invited three prominent tax accountants, Charles A. Barragato, Lance D. Christensen, and Raymond Kelly, to share with clients and friends of the firm their perspectives on how the new tax reform will affect high net worth individuals going forward.

From left: Stephen Juchem, Charles Barragato, Raymond Kelly, and Lance Christensen

Raymond Kelly, a partner at RSM US, LLP, began the session by speaking about how the tax reform will impact businesses. Corporate tax reform can be highlighted by a tax rate reduction to 21%, down from a previous rate of 35%. This reduction is significant as it puts the United States at a corporate tax rate that is closer to the worldwide average, making the United States corporate tax rates competitive with the rest of the developed world. Companies were able to reduce their taxable income in 2017 by accelerating expenses that would otherwise have been deferred to 2018 or later. The acceleration of such expenses allowed corporations to reduce their tax in the year that had a higher tax rate, effectively providing a greater tax benefit.

Certain partnerships are also receiving a tax benefit under the new tax law. Partners of certain qualified businesses are eligible for a 20% deduction on pass-through income. Qualified businesses generally exclude service industries, except for engineering and architectural firms. In order to utilize this tax advantage partnerships may consider using techniques such as spin-offs in order to segregate their administrative and sales businesses from their service businesses. The tax community expects the Internal Revenue Service to issue further guidance on the 20% deduction on qualified businesses over the next few months.

Charles Barragato, a partner at BDO, continued the conversation by discussing the estate and gift tax provisions of the Tax Cuts and Jobs Act. He shared that the estate tax was initially established in 1916 and continues to this day except for the year 2010, when it was temporarily repealed. The IRS maintains a unified estate and gift tax system which means the two are treated as one and the same for the purposes of removing assets from ones estate. Under the prior law an individual was able to gift $5.4 million tax free over the course of his/her lifetime. Under the new law the exemption has been increased to $11.18 million, more than double the previous law. In addition to the lifetime gift exclusions, the allowable annual exclusion by which any individual can gift up to $15,000 (up from $14,000 in 2017) per recipient to an unlimited number of recipients tax free each year remains part of the tax code. Medical expenses and tuition payments continue to be considered non-taxable gifts if they are paid directly to the respective institutions.

While the new law provides for this lifetime exclusion limit to be significantly larger than in the past, that provision is set to sunset in 2025. Therefore wealthy individuals and families should still be engaging in dialogue with their wealth management and accounting advisors on tax-efficient estate planning and wealth transfer strategies. Some of the estate planning techniques Chuck touched on include the utilization of valuation discounts, grantor retained annuity trusts (GRATs), and sales to intentionally defective grantor trusts. Valuation discounts allow for illiquid assets, such as partnership interests, to be discounted on estate or gift tax returns. Individuals can consider using family limited partnerships in order to transfer wealth to their beneficiaries at a reduced gift tax cost. GRATs are used to transfer assets out of an estate. Using a GRAT, the taxpayer (the “grantor”) contributes assets such as securities to an irrevocable trust while receiving an IRS specified rate of return. Appreciation in excess of the IRS stated rate is given to the beneficiaries of the trust free of gift tax. Finally, an individual can make a sale to an intentionally defective grantor trust. This will move assets out of an individual’s estate while including all taxable income on the grantor’s income tax return. This will allow the beneficiaries to be entitled to the assets (net of any purchase note) while the grantor remains responsible for the income tax liability from the assets.

Lance Christensen, a partner at Margolin Winer & Evens, LLP, took the group through the impact the tax reform will have on individuals. The top tax rate has been reduced from 39.6% to 37% which may not seem substantial but after factoring in the 20% potential pass-through rate, effective taxes can fall below 30%. Although the standard deduction is increasing to $24,000 for married individuals, the tax reform is tightening up on the allowable itemized deductions for individuals. State and local tax deductions are being capped at $10,000, and allowable mortgage interest is being limited to interest on future borrowings of $750,000 (down from $1,000,000 in 2017) (existing loans are grandfathered at current limits). In addition, home equity interest may no longer be deductible under the new law (however, such interest may be deductible if the loan proceeds were used to purchase, construct, or improve the home). These limitations are especially burdensome for New York residents who pay some of the highest real estate and state income taxes in the country. Lance shared that when these provisions were first announced there was concern that the cap on these deductions would negatively impact home values in areas like Long Island. Thus far, that has not happened based on a report Lance quoted during the session. It may still be too early to tell as the tax cuts were enacted less than a half year ago.

The states are attempting to help individuals from being burdened by these losses in deductions by passing new regulations. New York for example has created an 85% charitable contribution credit if donations are made to two state authorized charitable gift trust funds: The Health Care Charitable Fund and The Elementary and Secondary Education Charitable Fund. New York has also proposed a 5% unincorporated business tax which will be paid at the partnership level for flow through entities and flow through to the partners’ Schedule K-1’s. This will be interesting as the IRS may act to disallow the benefits resulting from such state tax workarounds.

Robert D. Rosenthal, Chairman, Chief Executive Officer and Chief Investment Officer of First Long Island Investors, concluded the seminar by explaining how the tax reform has and will continue to impact the investment marketplace. He emphasized that the new tax law is a fiscal growth initiative with a goal of boosting the overall United States economy. Over the past eight years GDP growth averaged roughly 1.8% per quarter. Over the two most recent quarters GDP was reported at 2.9% and 2.3%, respectively. He shared that many corporations have excess cash, due to lower tax rates, which they are using for reinvestment and in some cases to fund dividend increases for investors. The team at FLI believes the new tax law will strengthen companies financially and help continue to drive stock prices higher.

For more information on the effects of the tax reform law please refer to How Does the Tax Reform Bill Apply to You? Tax planning varies greatly based on an individual’s specific circumstances and we encourage each of our clients to reach out to us and/or their tax professional to review the strategies which would be most beneficial based on their needs. We look forward to the opportunity to work with you and your tax professional to discuss how the techniques discussed could be implemented for you and your family.

FLI is neither an attorney nor accountant, and no portion of this presentation should be interpreted as providing legal, accounting, or tax advice. Please contact your tax advisor.

Peconic Bay Medical Center honored the late Robert Entenmann, a founding client of First Long Island Investors, LLC, by naming the new administrative campus after him. After Mr. Entenmann died in 2016, his children Jackie and Robert, through the Robert Entenmann Advisory Committee, recommended to New York Community Trust that a gift of $5 million be made to PBMC’s New Era Campaign benefitting cardiac care for the region.

Robert D. Rosenthal who is Chairman and CEO of FLI as well a Trustee of Northwell Health (of which Peconic Bay Medical Center is a part) along with Ralph F. Palleschi, President and COO of FLI, and Edward Palleschi, Senior Vice President at FLI, attended the dedication with Robert’s daughter Jackie and members of the community. In his address to attendees at the event, Bob Rosenthal said “He [Robert Entenmann] was a man of conviction, a patriot, a man who believed in business ethics and most importantly he believed in quality – whether it was quality in a boxed cake we’ve all eaten for God knows how many years or whether it was quality in the wine he made at Martha Clara Vineyards, or his desire to have quality health care on Long Island.”

Read full press release here

“Only for short-term investors and market timers is a correction not an opportunity.”

-Warren Buffett, Chairman, Berkshire Hathaway

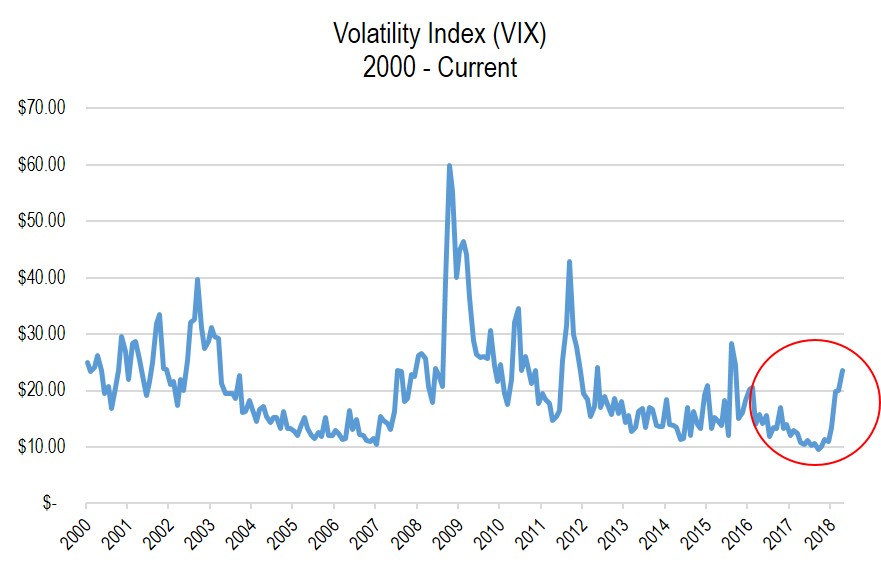

The first quarter witnessed the return of somewhat higher than normal volatility as compared to recent years (and certainly compared to the abnormally low volatility of 2017).

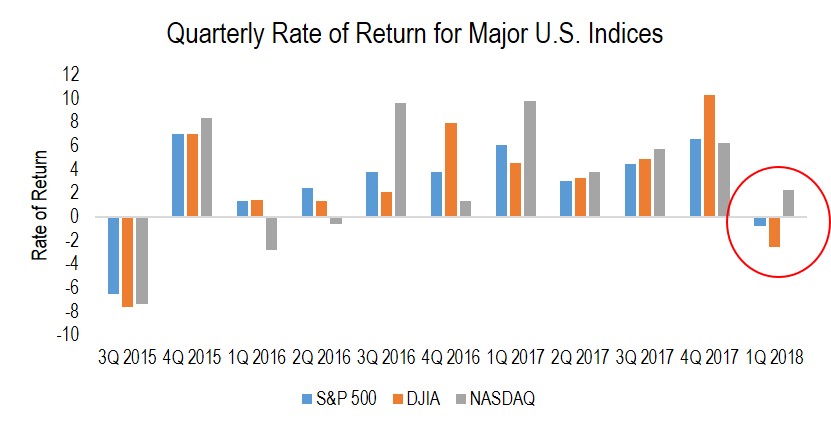

In addition to this increased level of volatility, both the S&P 500 Index and the Dow Jones Industrial Average recorded their first losses in ten quarters (-0.8% and -2.5%, respectively), while the technology driven NASDAQ rose by 2.3% (see chart below). Investors experienced the euphoria of the market hitting a number of highs in January only to be followed by sharp declines in February. In fact, the decline in early February resulted in the first correction (a decline of 10% or more) since the first quarter of 2016. However, markets sharply recovered in early March only to be followed by more declines leaving us with modest losses for the S&P and Dow for the first quarter. This roller coaster of ups and downs was disconcerting to many investors. However, we were not discouraged given the underlying strong economic fundamentals that we continue to observe, and because we realize that downturns and corrections are a part of long-term investing.

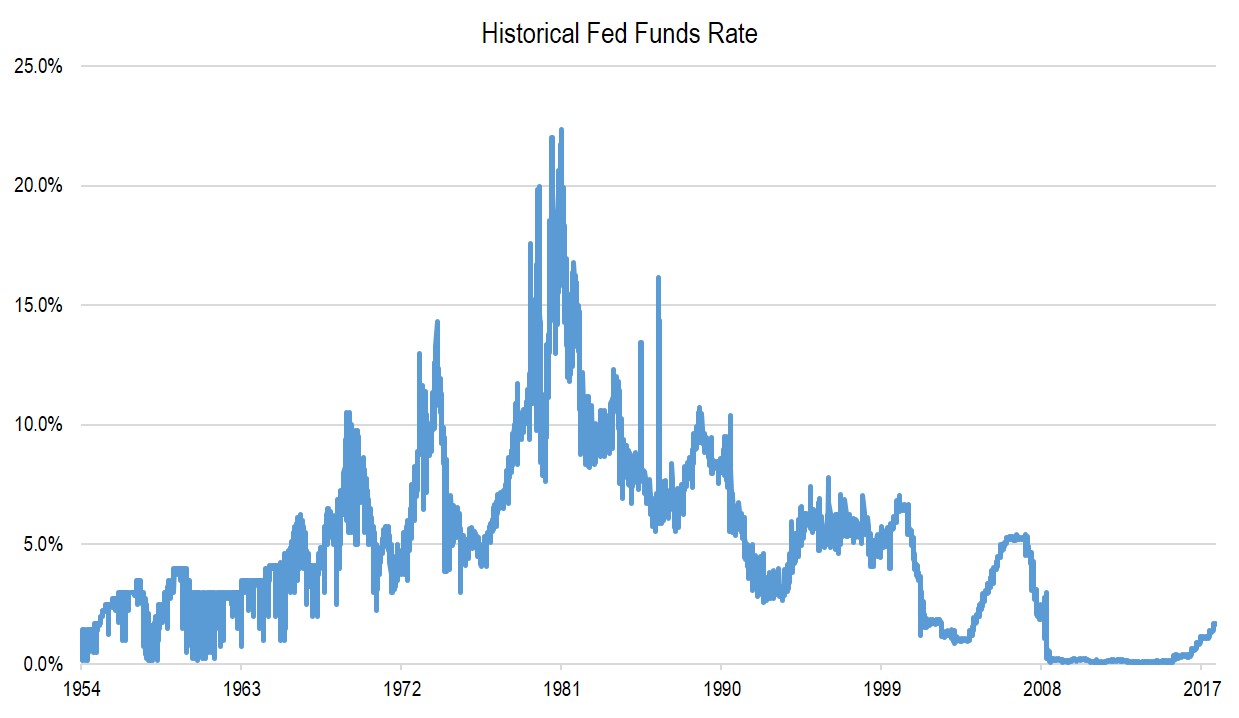

At the same time, the Federal Reserve, under the new stewardship of Chairman Powell, raised the federal Funds rate by an expected 25 basis points. In its official statement, the Federal Reserve pointed to a stronger economy and a continued strengthening in employment while inflation remains subdued at 2.4%. Accordingly, the Fed suggested that there would be an additional two, possibly three, more rate increases during 2018. Given the still historically low level of interest rates (see chart below), these projected rate increases do not suggest to us major headwinds for the equity or real estate markets. However, those with long-maturity bond portfolios could see modest losses. It is for these reasons (low yields and a bias to higher rates) that we continue to underweight fixed income as an asset class.

Given the above factors, we are pleased that all of our strategies1 for the quarter were either slightly positive or modestly negative. We view this as quite constructive given the significant absolute gains we enjoyed from all of our traditional and defensive strategies in 2017. In virtually all of our strategies we exceeded the respective benchmarks once again demonstrating the merit of active investing. We believe that given what we perceive to be positive drivers for the companies that we invest in, 2018 still should be somewhat of a positive year (although one should not expect returns to resemble those of last year).

In dissecting the positive drivers that we believe will provide these positive returns while outweighing some negatives, we point to the following:

- Profits for the companies that we invest in, and for many others, as seen in the chart to the right, should prosper in 2018 in part based on growing economies here and abroad.

- The Tax Cuts and Jobs Act of 2017 will reduce taxes for many of the companies we invest in, contributing to higher profits and increased cash flow.

- Repatriation of profits from overseas will also benefit many of the companies we invest in.

- Low interest rates and modest inflation, coupled with an increase in projected GDP growth, are constructive for equity markets.

- Consumer balance sheets remain in good shape supported by lower taxes, higher wages, and appreciating housing prices supported by an increase in housing formations.

- As stated in prior quarterly reports, synchronized global growth continues to support corporate earnings and business confidence around the world.

On the other side of the ledger, we do worry about these factors:

- A recession could occur (while we cannot time these, possibly in late 2019 or sometime in 2020). We are watching out for indicators including when the Treasury yield curve inverts, which is a harbinger of recession. A recession of the garden variety type (excess inventory) is not to be feared nearly as much as a “balance sheet” recession like 2008/9. Given the strength of most banks and consumers, we expect the “inventory” type of recession. However, equity averages typically decline no matter the type of recession.

- The extremism in Washington, D.C. resulting in an inability to compromise and effect reasonable change; the spending habits of Congress leading to a higher deficit (closing in on $22 trillion dollars); and the D.C. focus on political investigations, all create disruptions leading to greater volatility and investor confusion and concern.

- Geopolitical hot spots in Russia, the Middle East, and the Korean peninsula are top of mind. The immaturity of certain global leaders in dealing with these challenges is a significant concern. Election tampering, nuclear proliferation, and the multi-national war in Syria (Russia, Iran, the U.S., ISIS, Syria, and Turkey) continue to take Congress and the President’s time away from dealing with our growing deficit, the need for health care and immigration reform, and the ultimate need to restructure or rationalize both Social Security and Medicare, which are approaching financial crisis. These social safety nets must be preserved, but given the direction of demographics (more retirees requiring social benefits and less workers contributing to the system), some change is needed.

- From a purely economic standpoint, the potential of isolationism and trade war were major contributors to the uncertainty and volatility of the first quarter. We believe this will abate as time goes on. However, for the immediate future, it is a contributor to volatility and uncertainty along with some doubt over just how beneficial the recent tax legislation will be to our domestic economy.

- The Facebook data breach and misuse of personal information also riled the hot Information Technology sector. Disruptive technologies such as Facebook (a demonstration of American ingenuity and entrepreneurialism) will have growing pains and setbacks. However we do not believe this will derail Facebook, or any of our great tech companies including Alphabet and Amazon.com, which have transformed the way we communicate, gather information, and shop, as long as they do not break laws.

- Very low interest rates for such an extended period of time could have produced less obvious excesses, which as they are unwound could create volatility and dislocation of financial markets.

The above headwinds, which led to greater volatility and the first correction in major averages in more than two years, are a concern. In our opinion, this will not derail our equity-based strategies, which are concentrated and seek to invest in reasonably valued companies with solid financials, growing earnings, strong managements, and, in many cases, are beneficiaries of the recent tax law. Also, our bond portfolios remain typically short in duration so the creeping up of interest rates (thus far) should not be a major factor. Our current mezzanine real estate exposure continues to prosper with what appear to be good loans with equity kickers that have thus far resulted in solid returns. We anticipate recommending that suitable clients increase their allocation to this type of investment, when available.

Directionally, we continue to be biased to our defensive strategies. Our rational for this is the probability that a recession is getting closer, interest rates remain low so that bond investments will yield little better than inflation despite rates moving modestly higher, and some of the factors causing this recent spike in volatility have the potential to be more disruptive than might seem apparent. In addition, we still have to deal with the divisive and confrontational nature of Washington including the approaching midterm elections.

We continue to recommend an underweight to bonds (but have an allocation), an overweight our defensive strategies (all three), maintaining a modestly underweight allocation to traditional equities, and be selectively opportunistic in private investments, when and if they become available. Given a more challenging investing environment in the future, having a long-term view with a focus on quality remains paramount. In robust economies and markets, the tendency is for lower-quality equities or bonds to do better than they should. As economic and market circumstances become more challenging, these lesser-quality investments (typically weaker balance sheets) should not do as well as financially stronger companies in our opinion. We actually use periods of volatility to enhance portfolio characteristics where possible in our strategies.

We wish you a wonderful spring and hope to see you at our Thought Leadership Breakfast Seminar on May 23, 2018. The event will feature three prominent accountants who will share their perspective on the impact of the new tax law. We urge you not to hesitate to call upon us for any of your wealth management needs. It is a good time to focus on longer-term planning, including investments, estate planning, and insurance.

Best regards,

![]()

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. Partnership returns are estimated and are subject to change without notice. Performance information for Dividend Growth, FLI Core and AB Concentrated US Growth strategies represent the performance of their respective composites. FLI average performance figures are dollar weighted based on assets.

The views expressed are the views of Robert D. Rosenthal through the period ending April 20, 2018, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC. Copyright © 2018 by First Long Island Investors, LLC. All rights reserved.

On February 7, 2018, Robert D. Rosenthal, CEO and Chief Investment Officer, Philip Malakoff, SVP, Wealth Management, and Edward C. Palleschi, SVP, Wealth Management, held a web seminar where they shared with clients and business colleagues of First Long Island Investors our perspective on the current market and economic indicators. They discussed what our Investment Committee is most focused on for 2018 as we continue to position client portfolios for long-term growth.

“Uncertainty will always be part of the taking charge process.”

– Harold Geneen, American Businessman, Former President and Chief Executive of ITT Corporation

2017 was an excellent year for our clients. All of our traditional and defensive strategies made significant absolute gains. Our traditional and defensive equity based strategies averaged 22.7% and 19.1%, for the year, respectively. These results surprised many investors, but were consistent with what we had suggested could be the outcome based on these factors:

- Under Republican stewardship in all three branches of government in past years, equity markets averaged 19% per year. 2017 exceeded that.

- Business optimism increased on account of, among other matters, deregulation by the Trump administration.

- Global growth surprised many with Europe, Japan, and Asia joining higher growth in the U.S. and China.

- Comprehensive tax reform was finally passed (on a partisan basis) resulting in major corporate tax reform as well as a reduction in personal income tax rates and a limit on the ability to deduct state and local income and real estate taxes (which will hurt taxpayers in high tax states like New York and California).

- Employment remained robust. The unemployment rate fell to 4.1%. This contributed to consumer optimism.

- Inflation remained below 2% for most of the year which is helpful to consumers and we believe supports higher than average price-earnings ratios.

- Additionally, corporate earnings rose by about 12% for the year.

Of course, the above factors had to overcome worries last year that included:

- Three interest rate increases by the Fed (with the last being in December). At the same time, the Fed began to taper its bloated balance sheet.

- Valuations appeared high to some investors leaving them on the sidelines. The investment mood of caution was palpable.

- Friction with North Korea was a constant concern, mostly in the last half of the year. The potential for an armed conflict weighed on investor sentiment. The battle against ISIS and other terrorist groups also made headlines and was a concern.

- Concerns about the demeanor of President Trump as well as ongoing controversy regarding his campaign, members of his family, and certain advisors were constant news items.

These and other factors mentioned in our Investment Outlook (which clients received earlier this month) impacted 2017 as well as provided some caution, and, yes, optimism for 2018. In the final analysis, we had an excellent quarter and year even while having a recommended asset allocation that was somewhat defensive. These results contributed to meaningful appreciation in the net worths of our clients.

If you have not had a chance to read our Investment Outlook, please do.

On the news front, we would like to share with you that Ann DeVault, our Vice President of Administration, has decided to retire. Ann has been with FLI for over 28 years and while we are very sad to see her go, we wish her all the best. Ann is very well known to many of our clients and has been an integral part of our team for so many years. Ann will be leaving at the end of February so there will be plenty of time to wish her the best of luck. Also, we will be transitioning Ann’s work and relationships to others within our company. We have been working diligently to make sure that this transition is as smooth as it can be. Any clients who work directly with Ann will be contacted to review the specifics of the transition as it relates to them.

Finally, we invite you to join our web seminar, which is scheduled for Wednesday, February 7th at 2 PM EST. If you would like to join, please register.

Best regards,

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. Partnership returns are estimated and are subject to change without notice. Performance information for Dividend Growth, FLI Core and AB Concentrated US Growth strategies represent the performance of their respective composites. FLI average performance figures are dollar weighted based on assets.

The views expressed are the views of Robert D. Rosenthal through the period ending January 25, 2018, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC. Copyright © 2018 by First Long Island Investors, LLC. All rights reserved.