On May 2, 2019 Hofstra University held its 23rd Annual Gala and honored Robert D. Rosenthal, our Chairman, Chief Executive Officer and Chief Investment Officer for his years of dedication and service to the University as vice chairman of the Board of Trustees and chair of the Endowment Committee. The event raised a record-breaking 2.6 million dollars for scholarship. In addition to being the event honoree, Bob was presented with the Presidential Medal, one of the most prestigious awards given by the University.

Bob received his JD from the Maurice A. Deane School of Law at Hofstra University in 1974

March 31, 2019

“We always live in an uncertain world. What is certain is that the U.S. will go forward over time.” Warren Buffett

Robust results were recorded in the first quarter by equity markets following a very difficult fourth quarter. (Our clients enjoyed meaningful gains in all of our equity strategies in the first quarter.) Fourth quarter fears of higher interest rates, an imminent recession, political uncertainty over the anticipated Mueller report on whether the Trump campaign colluded with Russia, a slowing global economy, and continuing uncertainty about trade with China led to a severe decline in equity markets. In addition, the mid-term elections were contentious and led to a shift in power in the House of Representatives, which also concerned investors. We believe this severe market decline was disconnected from underlying company fundamentals as well as the general domestic economy. Our results for our clients in the first quarter, and those of the equity markets in general, suggest we were right, at least for now.

Domestic equities continued to outpace international equities, although both recorded significant gains. (We continue to underweight international equities.) As has been the case for a number of years, domestic growth companies continued to outpace domestic value companies. In addition, interest rates unexpectedly fell to levels not seen in roughly sixteen months. This resulted from the Fed backing off its October 2018 forecast of at least two interest rate increases in 2019. The Fed reversed that position and stated that unless data changes, it will not raise interest rates in 2019! In our opinion, this should be very good news for equity and real-estate valuations.

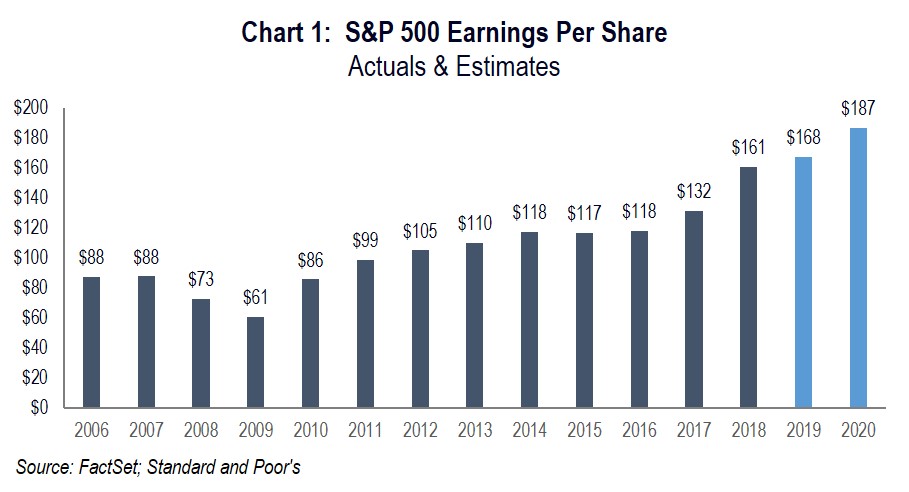

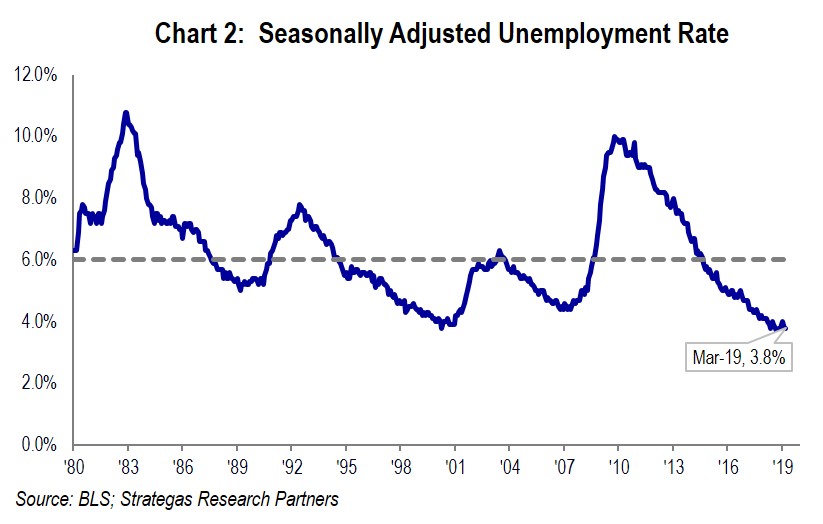

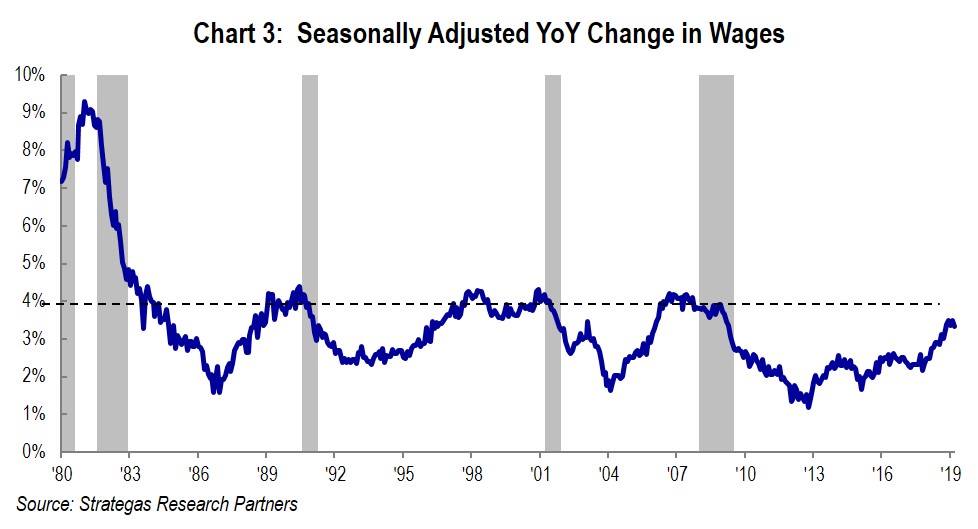

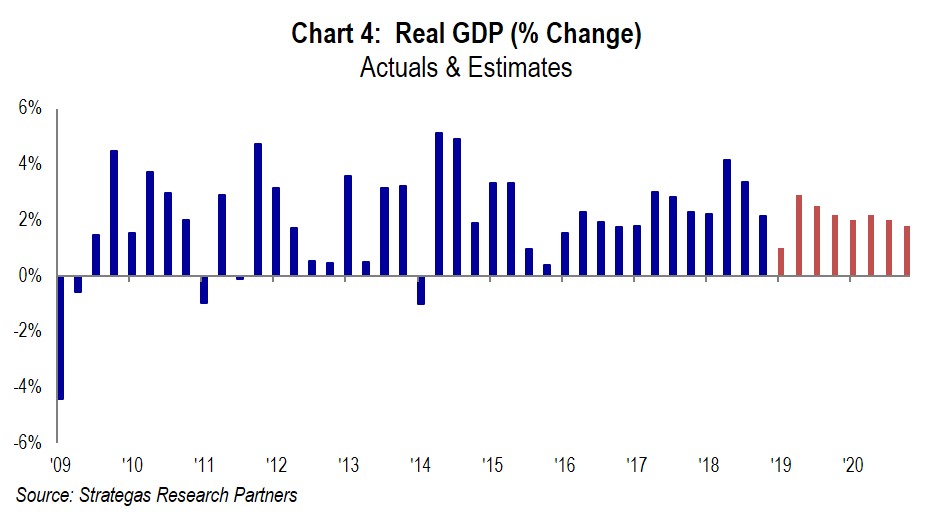

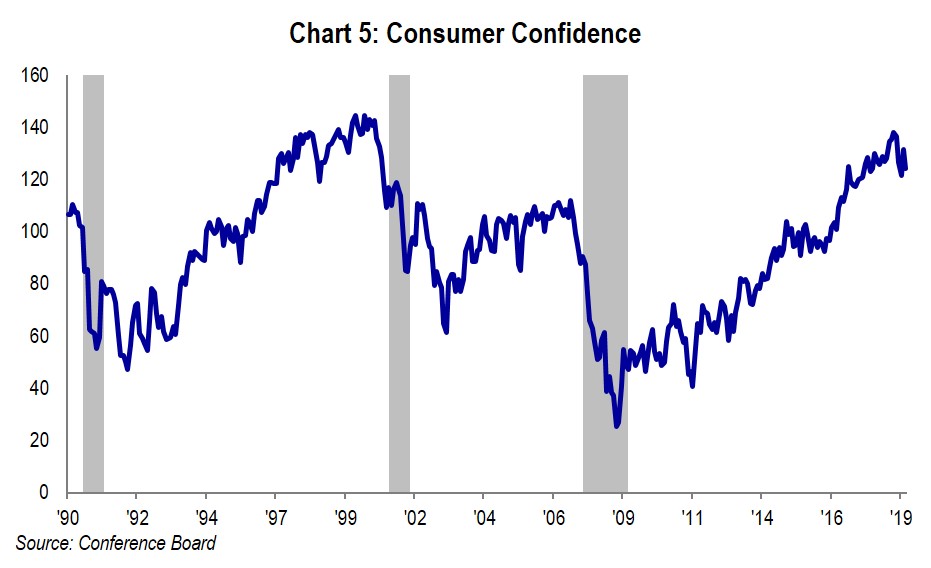

As we suggested in both our annual thought piece and in our fourth quarter letter, we strongly believed that the fundamentals of the companies we invest in were ignored in the fourth quarter stock market decline. We do not expect a recession any time soon (perhaps not for another eighteen months); corporate earnings continue to grow although at a slower pace (no new tax benefit this year); employment remains robust; wage growth is ticking up; and consumer and business confidence remain strong, as depicted in the charts below.

The above depicts a continuation of some of the key factors that we believe can contribute to the continued appreciation of our investments. However, we do not live in a perfect economic or political world and there are some other factors to consider that constitute the proverbial “wall of worry.” These include:

- A troublesome, at least temporary, slowdown in global economic activity within the significant economies of Europe and China.

- In Great Britain, a resolution to the thorny issue of “Brexit” continues to be debated with no solution in hand. This could impact the European economy even further.

- Political bickering over the recently released Mueller report continues to make for a Congress consumed with infighting while not addressing the more critical issues of the growing deficit, immigration, climate change, health care, and the viability of Social Security and Medicare.

- Although we keep reading about progress in the U.S./China trade negotiations a deal has still not been reached. This by the way could, if it happens, be a catalyst for more robust global growth later in the year.

- Interest rate spreads between the three-month and two-year Treasury bills versus the ten-year Treasury bond are important to monitor. The three month versus the ten year has recently inverted (albeit it is no longer inverted) suggesting a recession might occur in the not too distant future. However, the two-year Treasury versus the ten-year Treasury is not inverted (a spread of 14 basis points as of March 29, 2019) thus NOT signaling the threat of recession. Some pundits look to the three-month/ten-year, while we believe the two-year/ten-year spread is more indicative of an impending recession (which is not yet the case).

- The German and Japanese ten-year bonds are in negative yield territory. This suggests a concern about the pace of growth, or lack thereof, in both countries. Not a good sign in our opinion.

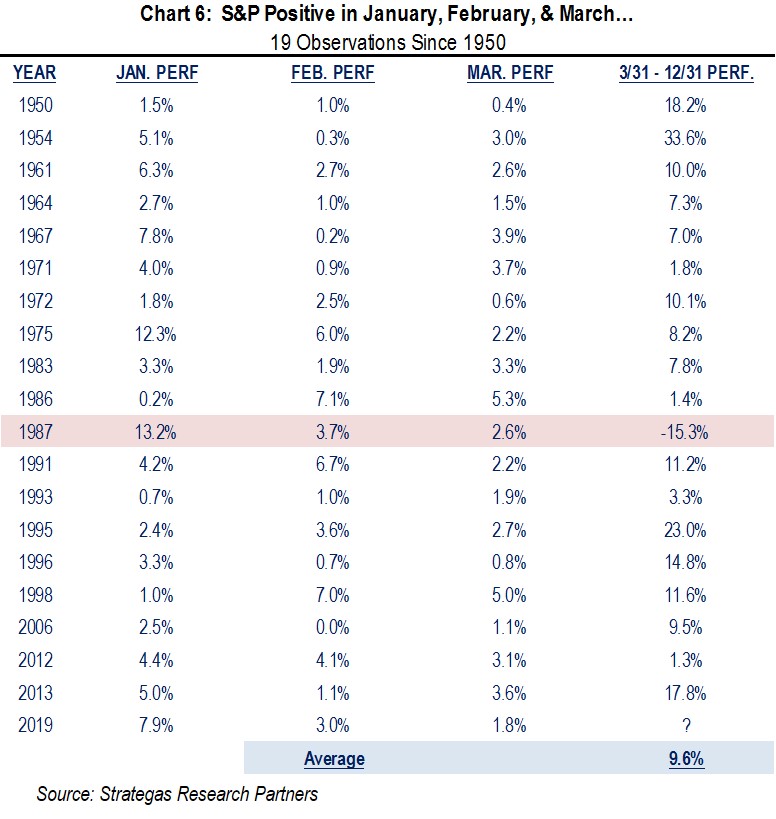

When putting all of this together we get a mixed economic picture. Thus our quote rings true, “we always live in an uncertain world.” However, we continue to take a long-term approach to investing in what we and our outside managers view as high-quality and reasonably valued companies and real-estate opportunities. Our heavily weighted asset allocation to the U.S. demonstrates our adherence to Buffett’s view that the U.S. economy (and government) will go forward over time. From a historical perspective, the robust equity returns in the first quarter suggest that there may be more to come for the balance of this year:

The above chart depicts a historical record which appears very positive. However, we point out that history is a guide and not a guaranty. Additionally, in each of these years there has historically been a drawdown at some point during the remainder of the year, although the full-year results have been positive. Yet it is worth considering that at least one of the outside economic experts we rely on believes that the second half of the year will see an economic acceleration for our domestic economy. If a trade agreement with China is reached that too can add to a stronger economy on a global basis. Finally, given the approaching 2020 election cycle, the current administration will be looking to encourage a robust economy. Of course, given the sudden and unexpected downturn in the fourth quarter of last year, one must not get too optimistic.

Given all of the above factors, our recommended asset allocations for clients continues to reflect a defensive tilt through a greater allocation to our defensive strategies while underweighting fixed income (which in some cases provides a yield less than the rate of inflation) and perhaps a modest underweight to traditional equities if one is concerned about volatility. The mixed economic picture plus the usual political uncertainty as well as trouble spots around the world make the defensive tilt seem reasonable to us. Our mandate has always been and will continue to be a return of capital first and foremost, and then a focus on generating a return on capital.

Summary

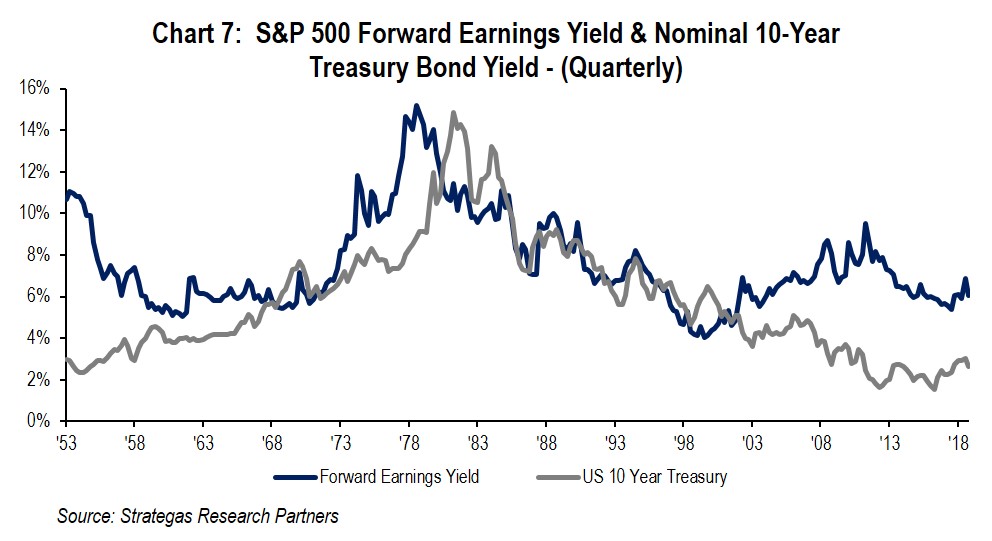

The first quarter was a very good one with appreciation in all of our equity-based strategies. Of the utmost importance, we believe that valuations are still reasonable. Furthermore, the relationship between the S&P 500 earnings yield and the ten-year Treasury yield supports that domestic equities are significantly more attractive than fixed income.

This is compelling in our opinion and suggests that further appreciation of equities (especially well-managed high-quality companies with growing earnings and/or growing dividends) is still quite possible unless earnings were to decline in general, which we do not believe will be the case for certainly the next year or so.

As our quote states, “we always live in an uncertain world” and that remains the case today. As the rest of the quote states, “what is certain is that the U.S. will go forward over time” which is also still the case today in our humble opinion. So, we remain cautiously optimistic as do the managers and outside economic consultants we work with.

Please call us with any questions that you might have relating to asset allocation or any of the charts or materials contained in this letter.

Best regards and enjoy spring!

![]()

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. Partnership returns are estimated and are subject to change without notice. Performance information for Dividend Growth, FLI Core and AB Concentrated US Growth strategies represent the performance of their respective composites. FLI average performance figures are dollar weighted based on assets.

The views expressed are the views of Robert D. Rosenthal through the period ending April 18, 2019, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC. Copyright © 2019 by First Long Island Investors, LLC. All rights reserved.

Following the sharp decline in the equity markets to close 2018, investors have concern about the outlook for 2019. On February 7, 2019, members of the First Long Island Investors Investment Committee held a web seminar where they shared with clients and business colleagues our perspective on the markets, domestic and global economy and when the next recession is likely to occur. These factors and more were incorporated into our latest thinking on asset allocation to position client portfolios for long-term growth.

On October 30th, First Long Island Investors had the distinct honor of hosting Lawrence Levy, Executive Dean, National Center for Suburban Studies (NCSS) at Hofstra University, as our guest speaker at a Thought Leadership Breakfast for clients and friends of the firm.

Lawrence Levy, Executive Dean, National Center for Suburban Studies (NCSS) at Hofstra University (left) and Ralph Palleschi, President and Chief and Operating Officer, First Long Island Investors (right)

In 35 years as a reporter, editorial writer, columnist, and PBS host, Lawrence (Larry) Levy won many of journalism’s top awards, including Pulitzer Finalist, for in-depth works on suburban politics, education, taxation, housing, and other key issues. As a journalist, he was known for blending national trends and local perspectives and has covered seven presidential campaigns and 15 national conventions. In his leadership role at NCSS, which he was invited by Hofstra President Rabinowitz to create in 2007, Dean Levy has worked with Hofstra’s academic and local communities to shape an innovative, interdisciplinary agenda for suburban study, including a new Sustainability Studies degree.

Mr. Levy centered the conversation on the changing demographics on Long Island and how that has impacted education, business, real estate, politics, and more. He described Long Island as a diversified center for small business creation, at the best it has ever been economically. Exports are at highs not seen in decades, unemployment stands at 3.5%, and it has been aided by government defense spending as well as small businesses picking up a lot of the economic slack. On the flip side, he described Long Island as a place with an aging demographic as well as aging infrastructure (bridges, roads, sewers, etc.). The governmental fragmentation on Long Island makes it extremely hard to get initiatives passed to deal with some of Long Island’s issues such as its aging infrastructure.

The segregation of cultures that exists on Long Island is a core issue. Long Island currently has one of the highest segregation rates throughout the United States. This segregation dates back to the 1960’s when practices such as blacklisting, gerrymandering, and pure policy were used to ignite the movement of minority cultures into certain areas. Banks would reject people of certain ethnicities with equal standards simply because they did not want them taking out a mortgage for a home in certain areas. This has been detrimental to certain cultures that have spurred growth and diversity in Long Island.

According to Mr. Levy, a multitude of ethnicities have contributed to Long Island’s economic success. The Asian population, which has been growing at rapid rates, has helped support Long Island’s housing market. Latino groups continue to bring “new worlds” to communities, with an influx of diverse ideas and capital. Additionally, people of African ethnicities continue to choose suburban areas throughout Long Island as opposed to moving into New York City. Long Island has been “very fortunate” to have this cultural diffusion, in the words of Mr. Levy, but the segregation that exists on Long Island has caused some of these minorities to be placed at a disadvantage, particularly regarding the education that children receive in certain areas. For example, the Hempstead School District offers no advanced placement courses to its high school students, not only depriving them of advanced education but putting them at a disadvantage for continued education in college in comparison to their peers. According to Mr. Levy, 50% of students on Long Island are non-white, and 80% of them attend the poorest 15 districts (out of 125) on Long Island. He shared that issues like this only garner attention when they get penned as a “pocketbook” issue. He is concerned this segregation may never end and could require some external force such as artificial investment or de-stereotyping to make significant strides.

The conversation transitioned to a discussion of the notion that Long Island is being hit on both ends – the aging of our population and that young millennials are not choosing to live on Long Island because it is said to be too expensive. Mr. Levy disagrees with this pre-conceived notion and pointed to many booming “downtown” areas such as Rockville Centre and Huntington where apartments and housing are quite affordable. He believes the issue is more that young people are simply being raised to expect a luxurious house immediately after graduation. In order to combat this issue, there has been a focus on smart growth by which housing development aims to optimize housing for both younger and older residents who may not want a multi-purpose housing unit and converting unused parking lots into apartment complexes to bolster the housing supply. Naturally occurring retirement communities (NORC’s) have also aided in sustaining the elderly population as reinvestment in the property of these communities (wider doorways, simpler structures) are more appealing to this group.

More about the speaker:

Over the years Larry Levy has forged research alliances with other academic institutions, including Harvard, Columbia, Cornell, Boston College, Virginia Tech, New York University, Exeter, and Maynooths, as well as consulting relationships with not-for-profit groups, businesses and government agencies. One recent partnership of note, with the world-renowned Schomburg Center for Research in Black Culture, resulted in the heralded exhibition “Black Suburbia: From Levittown to Ferguson.” Along with Academic Director Christopher Niedt, NCSS has promoted the importance of studying suburbs nationally and internationally and has generated nearly $4 million in grants, gifts, and contracts. Dean Levy was recently invited to lecture at the Harvard Graduate School of Design and the Harvard Medical School on the challenges of the changing suburbs and gives about 30 talks a year to academic, civic, and business groups on a variety of topics. As a member of a Brookings Institution advisory panel, he was a featured speaker at a Brookings Metro Policy Summit in Washington, DC. He was recently appointed Chairman of the Community Research Advisory Board at the Feinstein Institute for Medical Research, one of the world’s leading such centers.

About the National Center for Suburban Studies (NCSS):

NCSS has collaborated on a number of local, national, and international scale conferences on aspects of suburban life, from diversity and housing, to ecology science and health care. The center also has participated in major consulting studies on sustainability, demographic change and education and health care challenges in suburbia. At NCSS, Dean Levy has co-authored major regional studies, including the LI2035 Sustainability Action Plan, all five Long Island Regional Economic Development plans, and many of the post Sandy recovery reports for Suffolk County communities. Before joining Hofstra, he was Senior Editorial Writer and Chief Political Columnist for Newsday; cohost of the PBS show Face-Off, and remains involved in the world of journalism and politics. Levy has been a guest contributor to BBC.com, CNN.com, Politico, Newsday, Citiwire, and Hearst Newspapers and wrote about presidential campaign issues for the New York Times.com Campaign Stops blog. (Most of these articles and some of the media appearances can be found at the NCSS website www.hofstra.edu/ncss). He appears regularly on local and national television. He is a graduate of Boston University’s School of Communication. He’s especially proud of organizing the Hofstra Celebration of Suburban Diversity, which annually brings together hundreds of people from different races, religions and other backgrounds and has raised more than $1 million for diversity related scholarships, research and community engagement. At the same time, the event, which has featured the region’s most influential business and labor leaders as keynote speakers, has dramatically raised Hofstra’s profile as a place that values diversity. He also is pleased to be able to “give back” by mentoring many young people in journalism and public life regardless of their ideological or political allegiance.

December 31, 2018

“Patience can be bitter, but its fruit is sweet.” -Aristotle

The fourth quarter witnessed a significant downturn for equity markets as well as a decline in energy prices. These downturns were in contrast to strong corporate earnings growth, estimated GDP growth of 2.7% and continued high demand for oil. The equity market downturn was widespread, however value stocks, which had trailed growth during the year, had less severe declines, but declined nonetheless. International stocks, including emerging markets, had substantial declines in the quarter contributing to full year results that significantly underperformed domestic stocks. Commercial real estate remains stable while residential real estate weakened, as mortgage rates slightly increased. This also depended on local market conditions.

For the most part, our defensive and traditional equity strategies fared well in that most met or exceeded their respective benchmarks during the quarter, despite almost all experiencing a significant drop during the quarter. For the full year, all but two of our many defensive and traditional strategies met or exceeded their benchmarks.

Quality, for the moment, did not seem to matter. Strong earnings growth, for the moment, in our portfolio companies for the most part did not matter (there were some exceptions). Better than targeted dividend growth (13.9% on average for the year) in our Dividend Growth Strategy, for the moment, did not matter as well. Overall, when looked at over the two year period of 2017 and 2018 our approach to asset allocation and investment strategies achieved solid results for our clients.

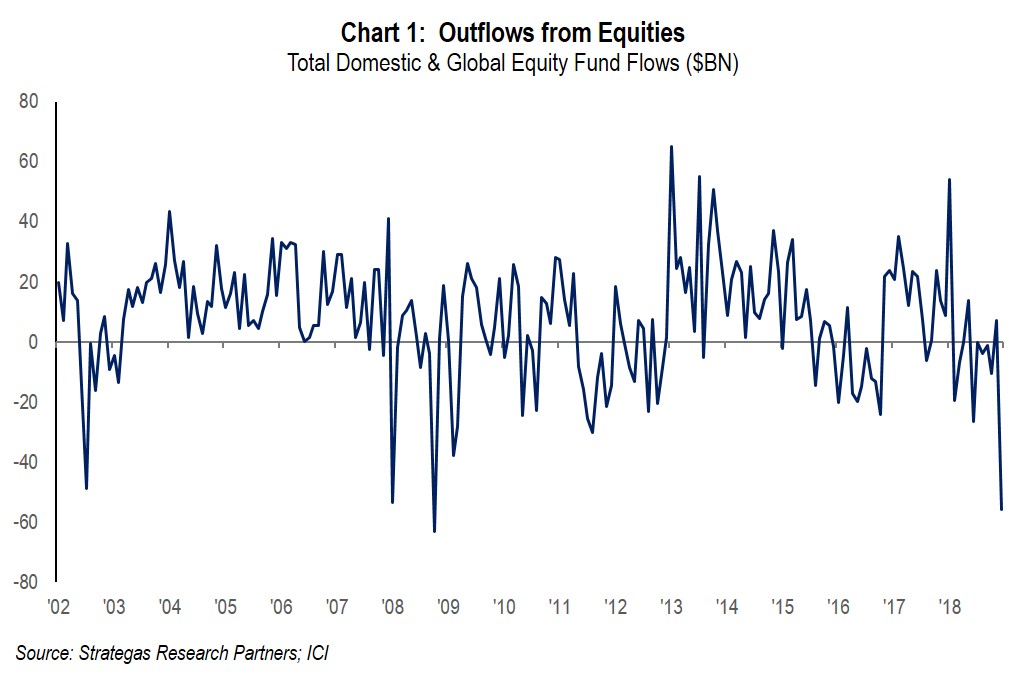

Apparently, what did matter were, in our opinion, missteps in communications by the new Fed Chair on interest rate and balance sheet policy, an attack on him by our President, a take back by the President of what seemed to be progress in talks with the Chinese, and the realization of the obvious — that corporate earnings would likely grow in 2019 but at a much slower pace. In our opinion, these factors, and probably others, led to the largest one-week outflow from equities on record, even greater than in 2008/2009! This makes no sense to us given underlying fundamentals and the strength of our banking system. We believe that withdrawals from ETFs and index funds (passive investing) is what contributed to the widespread decline irrespective of quality, earnings growth, or dividend increases.

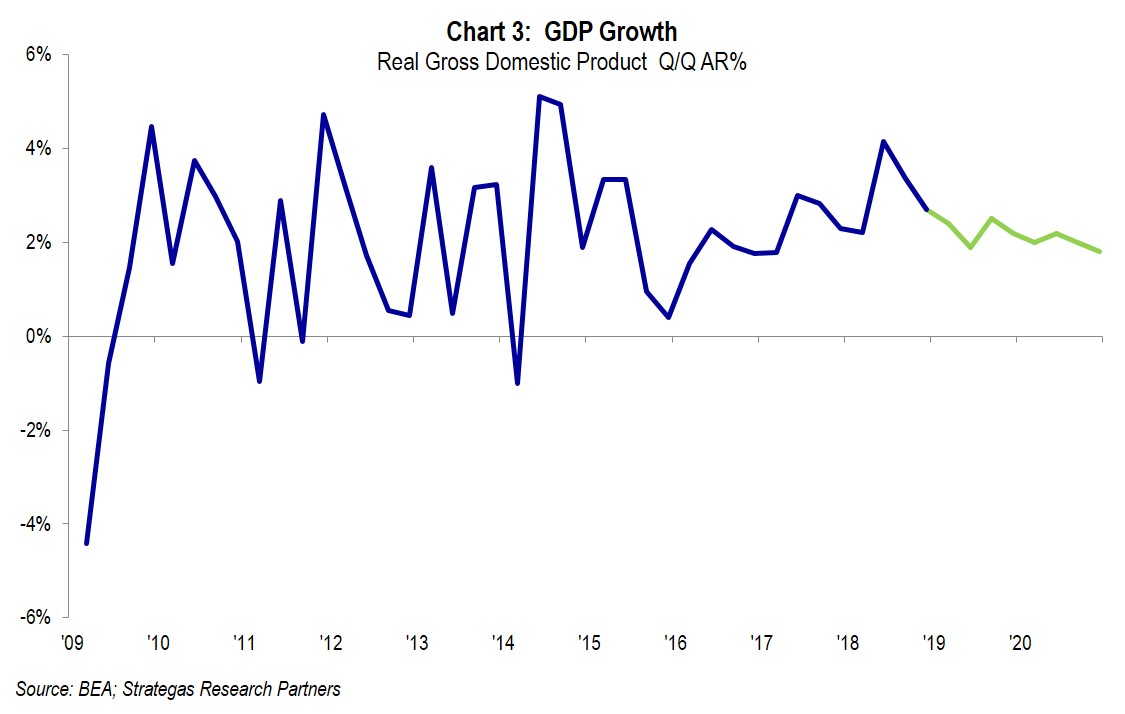

It just seems strange to us that record outflows (See Chart 1) would occur when earnings growth is projected to continue and GDP growth also continues, albeit at a slower pace (see Charts 2 and 3).

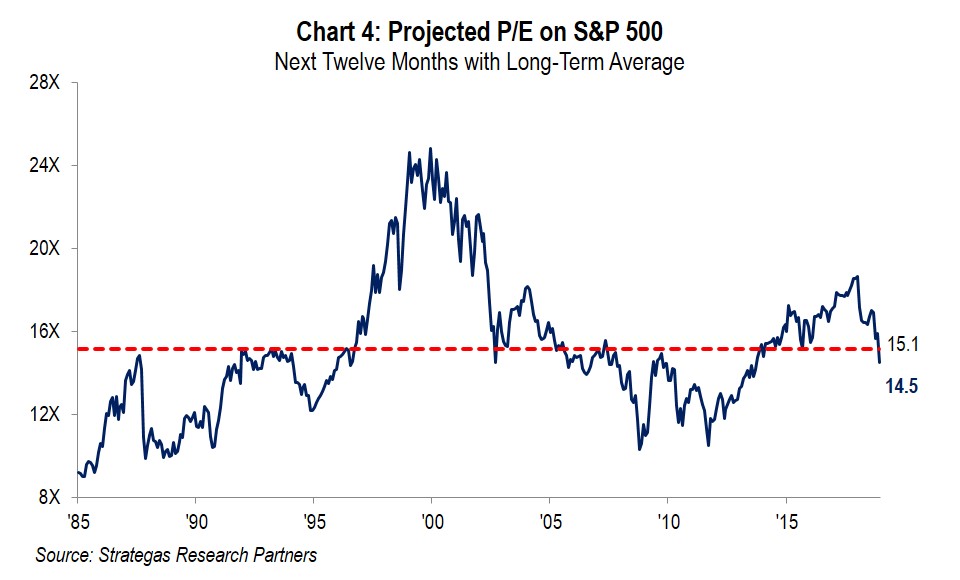

So, without repeating what we spoke of in our annual thought piece, the economy and earnings remain moderately strong while stocks were taken to the “woodshed” in the final quarter of 2018. The result being a below average P/E on 2019 projected earnings.

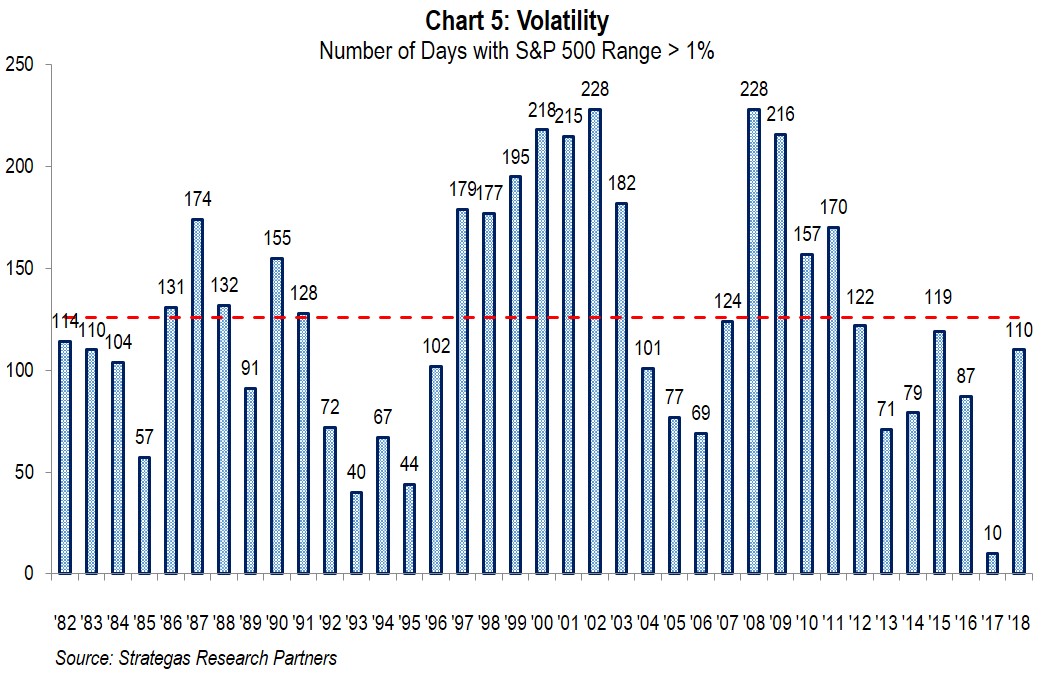

Additionally, volatility picked up in the fourth quarter. In numerous quarterly reports we have warned of increased volatility. Well, it is here but in Chart 5 below you can see that volatility is normal, and where we came from was abnormally low.

By the way, the increased volatility, if it continues, should help one of our defensive equity strategies.

What does it all mean?

The fourth quarter was very difficult for most investors. Equities sharply declined wiping out three quarters of gains for the S&P 500 and then some while short-term interest rates increased while longer-term bond yields declined. Oil prices declined, we believe because of oversupply, which will help consumers and many businesses (acts like a tax decrease). Valuations are now far more reasonable going forward; some would argue cheap when considering where interest rates are.

However, looking forward we now have a split government, a President and his campaign under investigation, key cabinet members departing, a partial government shutdown, and a Chinese trade war still evolving. This is a prescription for more volatility while economic fundamentals remain quite reasonable, for now. We as a firm still do not see a recession for 2019. That is a positive in our opinion.

We will be watching the fundamentals which we continue to believe will reward us as long-term and PATIENT investors. Just think about the impact of we or you having panicked the day or so before the Dow appreciated by over 1,000 points. Prudent asset allocation is our path to withstanding these periods of extreme volatility while prospering over the long term (the last several years have been good to us), and being patient to achieve the sweetness of the bitter environment we have just endured.

We hope you will join us on Thursday, February 7th at 2 PM EST for our web seminar where we will discuss our overall outlook for 2019 and how we are recommending clients portfolios be allocated for long-term results.

The start of the New Year is always a good time to reevaluate your asset allocation and ensure it is aligned to meet your goals. We would be happy to sit down and discuss your individual situation.

Best regards,

![]()

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. Partnership returns are estimated and are subject to change without notice. Performance information for Dividend Growth, FLI Core and AB Concentrated US Growth strategies represent the performance of their respective composites. FLI average performance figures are dollar weighted based on assets.

The views expressed are the views of Robert D. Rosenthal through the period ending January 25, 2019, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC. Copyright © 2019 by First Long Island Investors, LLC. All rights reserved.