2020—A New Year, A New Decade

Listen to the report.

“It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.”

-Robert Kiyosaki

The above quote really sums up the mission of First Long Island investors in representing clients over the long term. It is how we view 2020 and beyond while having just experienced the ups of 2019 and the unexpected downturn in late 2018. To have a sense of what we should do as investors for this coming year and beyond, we should analyze what took place during these last two somewhat volatile years to gain insight for the future. The 2018 market took our breath away in a dramatic fourth quarter reversal, and the 2019 market seemingly experiencing a “melt-up” in most asset classes, despite a trade war and articles of impeachment passed by the U.S. House of Representatives for only the third time in history.

With a backdrop of significant de-regulation under the current administration coupled with major tax reform, our U.S. economy in 2018 was vibrant. Unemployment dropped throughout the year, corporate earnings rose (particularly from tax reform), wages started to grow above the rate of inflation, and consumer confidence was ebullient. However, in the fourth quarter equity markets tumbled and investors fled the equity markets seeking the safe havens of cash and bonds. In our opinion, the two catalysts that primarily caused this severe and unexpected drop in the fourth quarter of 2018 were unwelcome Federal Reserve statements and interest rate increases and President Trump’s declared trade war with China while the trade pact replacing NAFTA (between the U.S., Mexico, and Canada) had not been completed. These events led the 10-year U.S. Treasury to reach 2.7% as of December 31, 2018 and to a drop in the S&P 500 Index by -13.5% in the fourth quarter resulting in a modest full year loss (-4.4%), after having been positive most of the year.

As 2019 began, fear of an imminent recession could be heard from pundits, however we at FLI (as we stated in our 2019 Investment Outlook), made it clear that we did NOT see a recession commencing anytime soon. At the same time, the newly appointed Fed Chair Powell, who pronounced a plan to raise interest rates in the fall of 2018, walked back off that plank in January 2019. Markets rallied sharply in 2019 while interest rates started to drop, with the 10-year U.S. Treasury ultimately closing 2019 at 1.9%. Plus, Washington and Beijing announced that Phase one of a trade agreement had been reached in December. Lower interest rates, a seemingly agreed to partial trade agreement, and the continued drop in unemployment to its lowest level in 51 years while inflation remained around 2% led to a dramatic increase in equity markets. Consumer confidence more than made up for sluggish business investment which we attribute to both the more than yearlong trade tiff with China and the leftist positions of certain well-polling Democratic presidential candidates who are proposing many potential policies that would be extremely difficult for the business community. These democratic socialist positions would not be well tolerated by most asset classes including the stock market in our opinion.

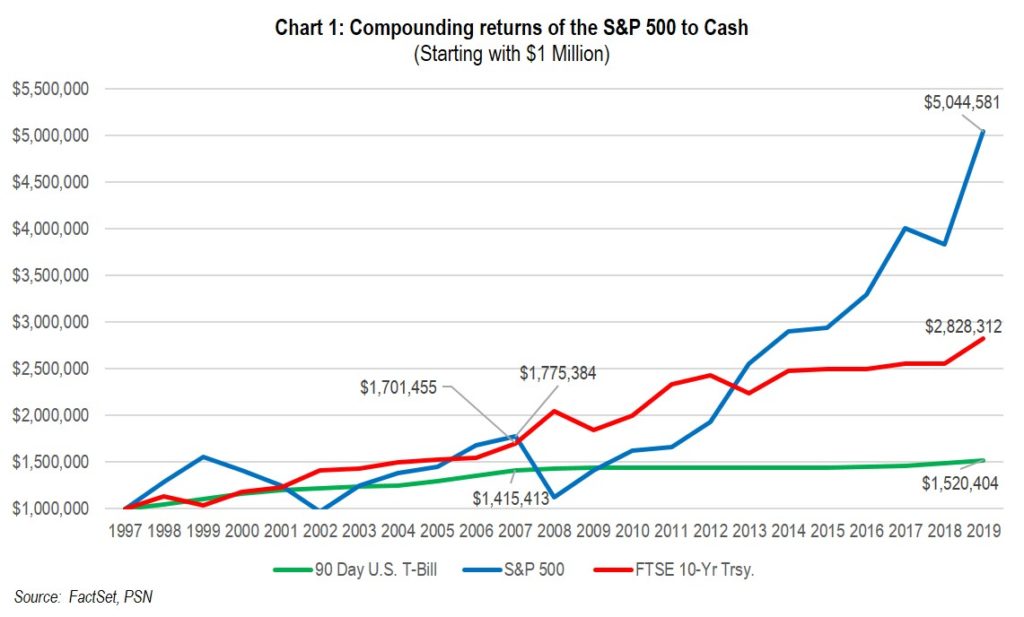

Those who fled the equity market in 2018 (and many prior to this) missed out on a gain in excess of 31% for the S&P 500 Index in 2019 (growth companies led the way for the 7th time in 10 years). Additionally, international continued to trail domestic returns for the second year in a row, making 2019 the 8th of the last 10 years where domestic bettered international. However, if they parked their dollars in longer-duration bonds, they did just fine but achieved nothing close to the gains in equity markets.

So, these oversized gains in 2019 for both bonds (8.7%, as measured by the Bloomberg Barclays U.S. Aggregate Bond Index) and stocks (31.5%, as measured by the S&P 500 Index) should in our opinion be considered in connection with 2018’s lackluster market performance for an average return over this volatile two-year period. It is obvious that those whose asset allocation kept a meaningful exposure to equity markets did very well, and those overweight bonds and cash missed out significantly. Our asset allocation in both our defensive and traditional equity strategies over the long term will, in our opinion, make our monies work harder for us and provide better returns than cash or bonds. This has been proven to be the case over the long term. Cash and bonds have a place, but overweighting at current very low rates will rob investors over the long term in our opinion.

Our goal is to keep you from losing too much in any downturn, expected or not, while over the longer term keeping your capital working for you. Those that chose to hide out mostly in cash and bonds missed out on a two-year average gain that would have grown their capital in an economic environment that was vibrant despite the trade war, a vacillating Federal Reserve, and a domestic political environment of both impeachment and winds of democratic socialism. Acting based on fear without analyzing fundamentals is not a prudent way to invest, in our opinion.

From a longer-term perspective, if you had chosen to follow your advisors at FLI over the past decade (which virtually all clients have), you would be in very good financial shape as we enter this new decade. But what is the current investment environment, and how do we protect our capital while still letting it work for us and future generations? We cannot assume that history will repeat itself, especially after a decade of gains.

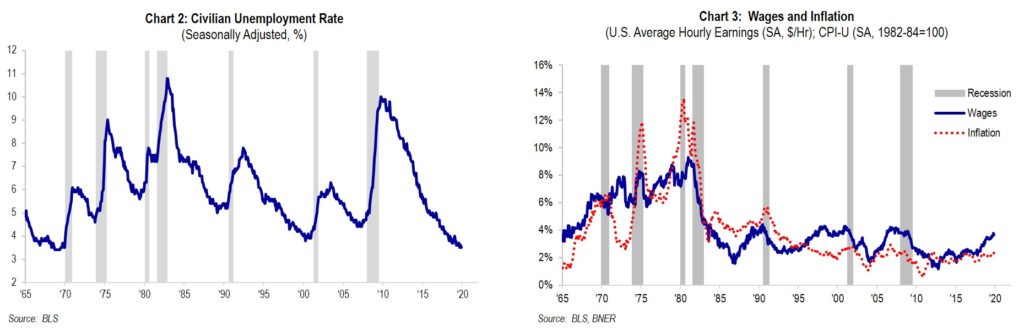

One major factor to analyze remains the employment picture which is excellent as evidenced by both the unemployment rate and wage growth (Charts 2 and 3 at the top of the next page) that depicts a rate of growth above inflation.

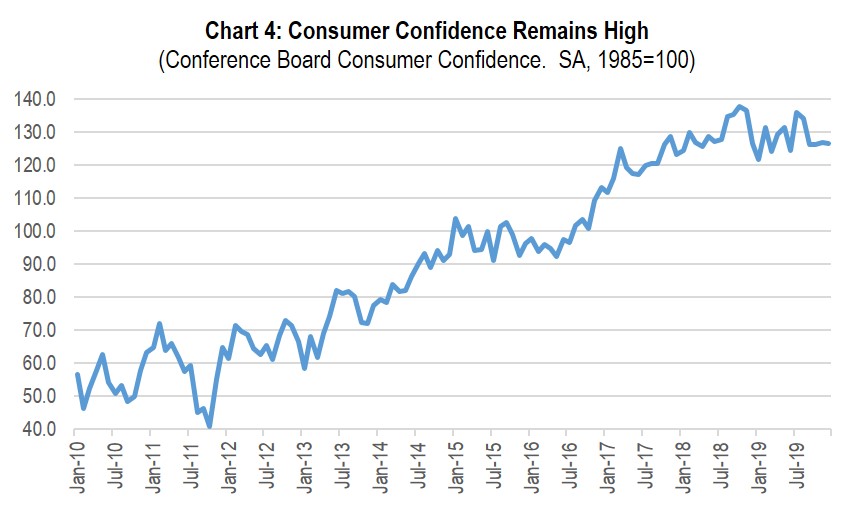

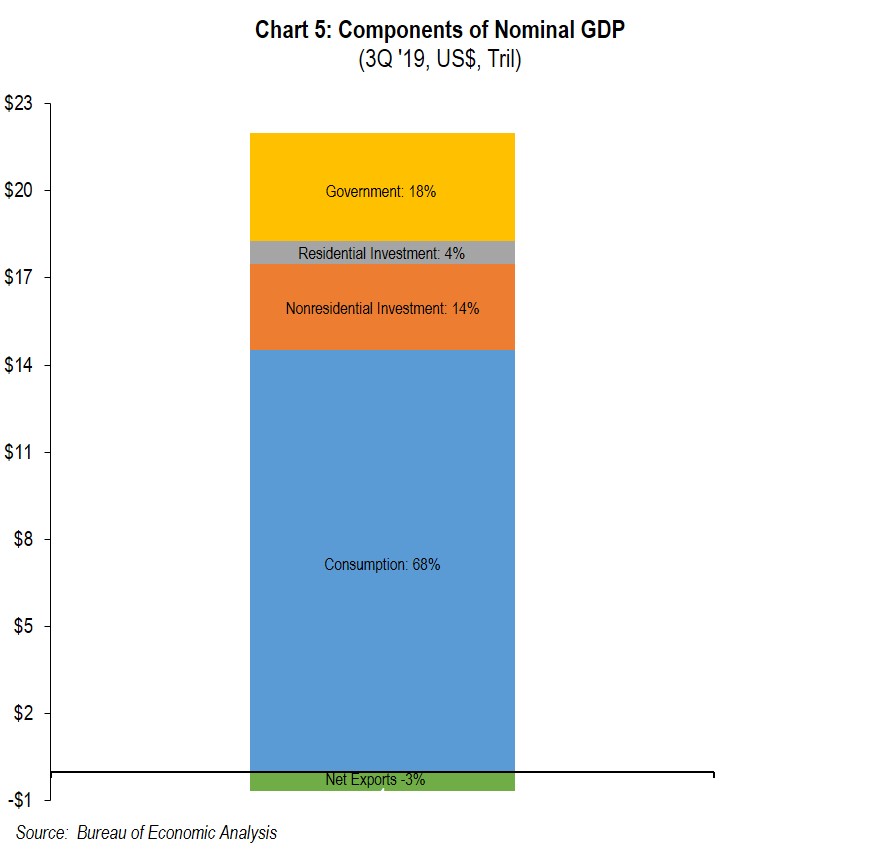

The consumer, who is benefitted by both of the above charts, continues to be robust and is a major driver of our economy. Consumer confidence remains quite high (Chart 4) and the consumer makes up 68% of our domestic economy (Chart 5).

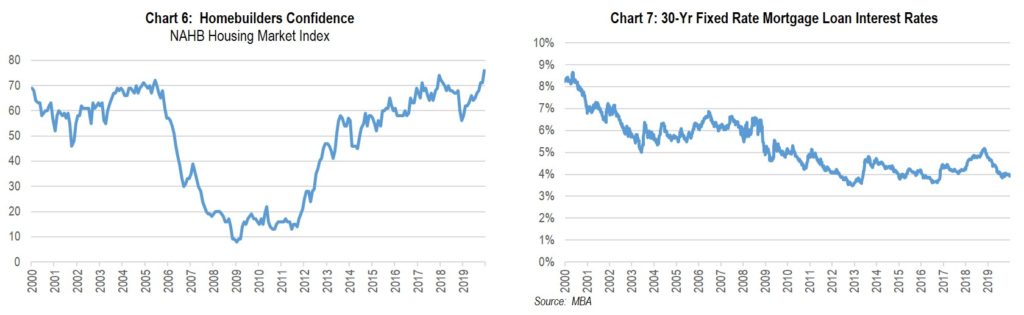

The healthy consumer also is a critical component to our robust housing market (and a contributor to our economy) along with low interest/mortgage rates (as seen in Charts 6 and 7).

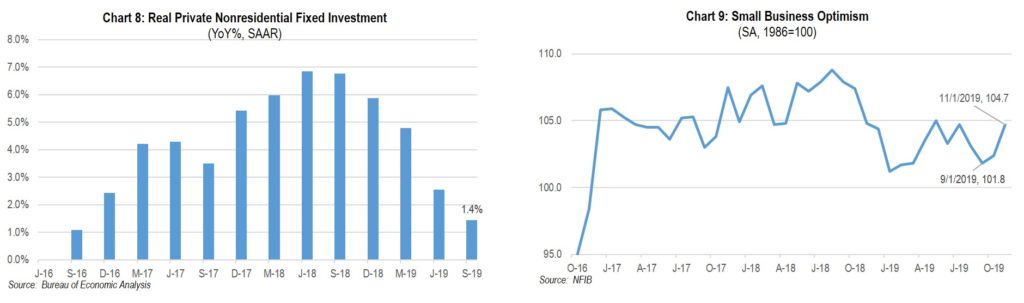

On the other side of the coin, business investment (Chart 8) which is critical to productivity and important to job creation in the future remains disappointing. We believe that for businesses to increase their investments they really need to see the positive effects of both Phase one of a China trade deal and the newly approved trade pact with both Mexico and Canada. Chart 9 depicts, in our humble opinion, the muted small business optimism resulting from the trade wars, fears of higher interest rates and recession, as well as the political turmoil from this past summer, which just started to rise in the fourth quarter:

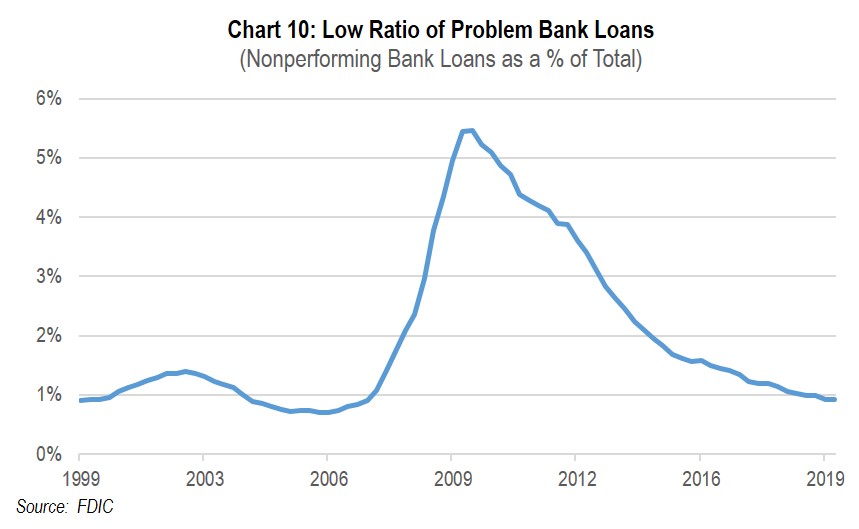

Our view continues to be that, barring an unforeseeable exogenous event, we will NOT experience a recession in 2020. We expect that having some of the trade issues being resolved, coupled with a strong consumer, will lead to another year of GDP growth of 2% or more. It is possible that with an accommodative Fed helping our domestic economy, as well as foreign central banks stimulating China and Japan, the global economy could also pick up steam. In addition, our strong banking system (as evidenced by all major banks having recently passed their stress tests and the ratio of delinquencies to total bank loans currently being at the lowest level in 25 years, as shown in Chart 10) enabled by a modestly positive yield curve will support our growing economy. Several of our strategies hold high-quality banks whose earnings and dividends are growing. However, not all companies will be winners in terms of growing earnings, and not all real estate will benefit from either business investment or robust residential activity. Thus, selectivity will be crucial in choosing our holdings for long-term investment. With long-term investment we are biased to companies whose earnings and/or dividend growth have durable qualities and we need well-located real-estate related investments in areas of growing population and job growth.

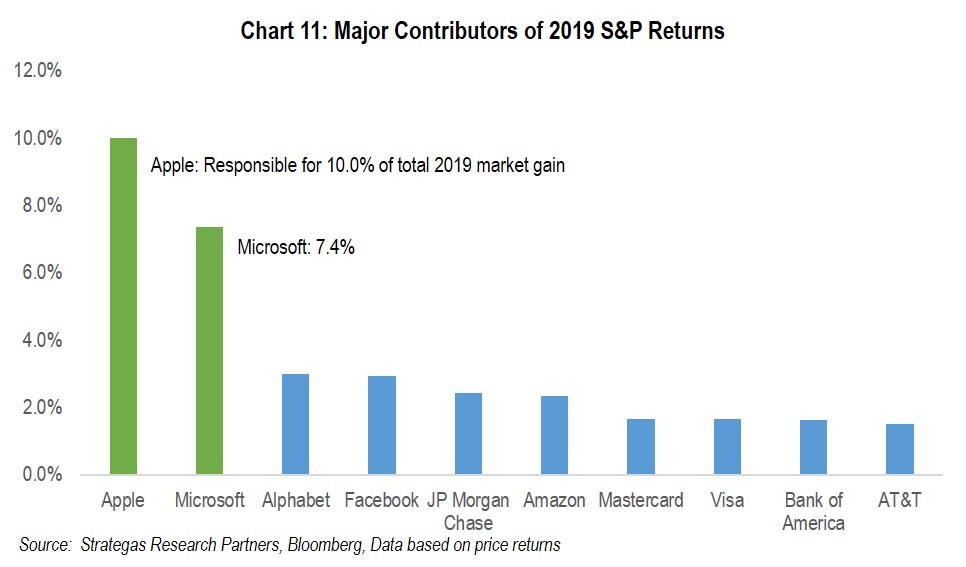

In 2019, equity market gains were skewed to “big winners,” including Apple and Microsoft. Those two companies contributed more than 17% to this year’s rise in the S&P 500 along with some other notable growth companies: (Some of the companies in the chart below are held in various FLI strategies.)

Valuation Matters

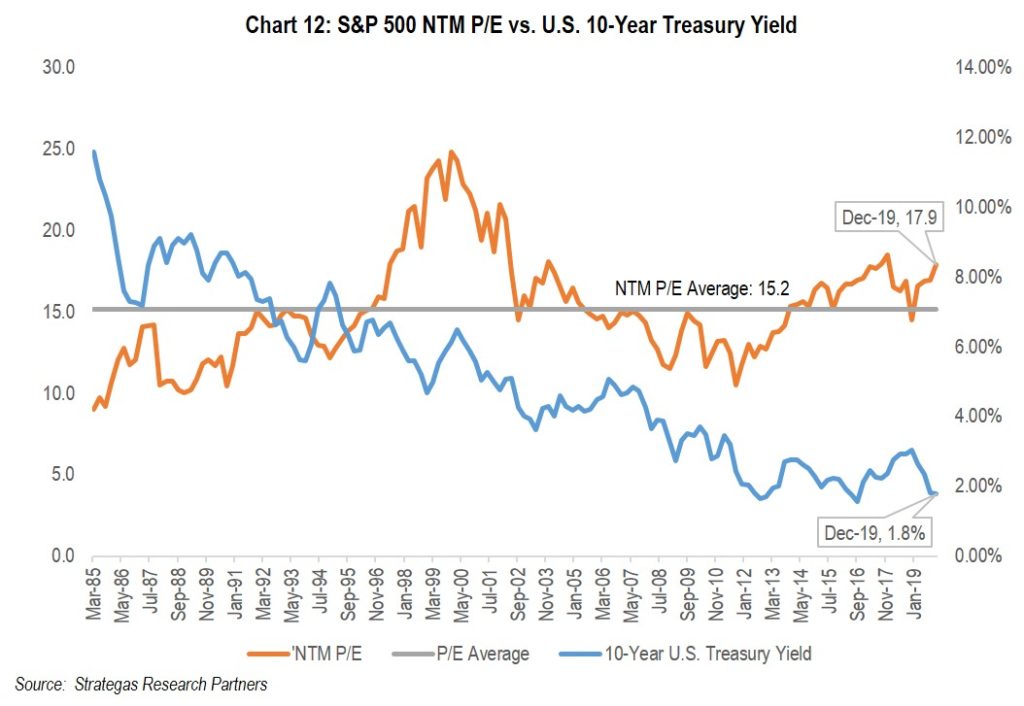

After such a strong 2019, we must visit valuation for the markets in general and of course for our strategies. All three well-known indices: the S&P 500 Index, The Dow Jones Industrial Average, and the NASDAQ achieved record levels. Let’s look at the current valuation of the S&P 500 Index from the lens of the price-earnings ratio and the yield on the 10-year U.S. Treasury which we believe is critical when looking at valuation:

Chart 12 (previous page) demonstrates that while the market is not cheap, it is not very expensive as long as the earnings projections for 2020 are met, after flattish earnings growth in 2019, given the current low interest rate environment.

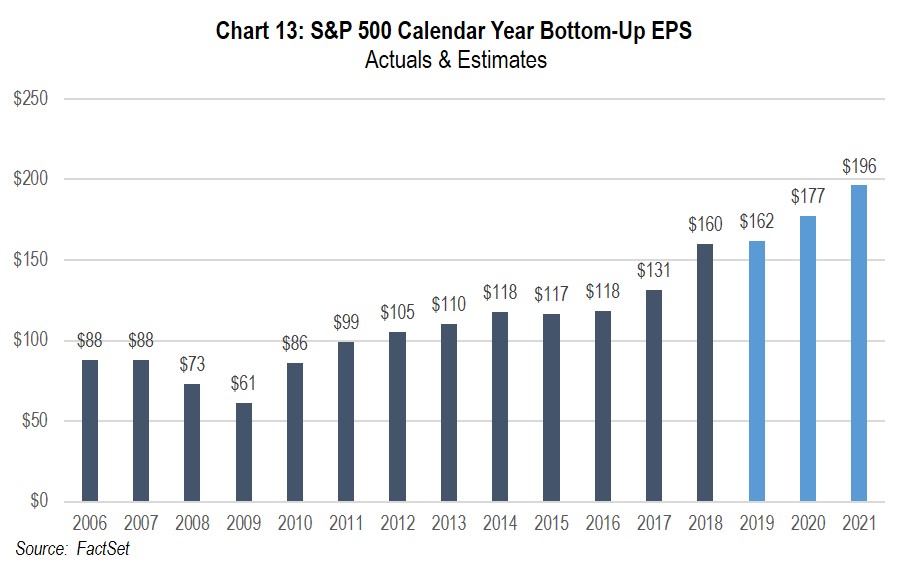

FactSet’s consensus estimates currently point to earnings growth for 2020 of about 9.6%. Despite this projection, picking the right companies to invest in is critical as evidenced by Chart 11 on the previous page. We do not believe that all companies will achieve the same level of positive results, so our continued bias, for the most part, of either investing in high-quality companies with growing earnings and/or financially strong quality companies with above-average dividend growth fueled by growing cash flow is essential. These types of companies when reasonably valued should not only protect one’s capital over the long term, but will provide what we believe will be a reasonable return above inflation (while also being superior to cash and bonds at prevailing interest rates). The same goes for real estate and private equity investments. Earnings, rent roll, or acceptable mezzanine interest rates with underlying quality properties or private companies are imperative in today’s investment environment, where there is still plenty of uncertainty both economically and politically.

Political and Geopolitical Environment

Normally we do not focus on the short-term impact of the political and geopolitical environment as long-term investors. However, our domestic political environment is imbued with extreme divisiveness resulting in a partisan impeachment, and with a Presidential election in roughly ten months, it most likely will provide volatility and fear. In addition, for the first time in my memory, the winds of democratic socialism are real as some segments of our population and politicians attempt to deal with the growing issues of wealth and income inequality. We at FLI do not believe that democratic socialism is the answer to the issues, but some potential candidates for President believe it, or something close to it, is called for. We believe the unintended and possibly even some of the intended consequences could hamper our economy and most, if not all of the various asset classes we invest in. We will be watching this carefully, for if a democratic socialist leaning candidate wins the Presidential election, along with Senate composition changing, major tax, regulatory, and social reforms might have to be reckoned with. In any case, there are tough decisions ahead for our elected officials in dealing with the cost of health care, the funding of Social Security and Medicare, climate change, legal immigration, and our mushrooming debt along with border security and geopolitical threats (wow, quite a wall of worry).

As mentioned earlier, increased free trade and a stronger global economy should be the result of a Phase one deal with China, the newly signed trade arrangement with Mexico and Canada when implemented, as well as a possible deal with Great Britain once it exits from the Eurozone. If these should not happen there could be a negative impact to our economy, but we do not believe that will be the case.

Domestic politics and trade arrangements around the world will play a role in how strong or weak the U.S. economy will be. The resulting GDP growth will be an underlying factor in how many companies prosper in the years to come.

What to Do Going Forward

As investors we must be guided by the principles espoused in Mr. Kiyosaki’s quote. It is not just how much money we make this year, but how much can we hold onto together with gains from the past, and how much we can grow our assets for the future without taking undue risk. There is always uncertainty and we have just come through a two-year period where if one had the proper customized asset allocation (with a bias to growth and a bias to FLI’s Dividend Growth Strategy in the value space) one did quite well. In our view, we remain “skeptically optimistic” such that we would continue to remain overweighted to our defensive equity strategies (made up of both growth and value-oriented companies) that can appreciate, slightly underweight traditional equities (with some exposure to internationally domiciled companies), and underweight fixed income which had a great run in 2019 that we believe will not be repeated in 2020. Also, we will continue to selectively invest in quality, real-estate-based investments with targeted higher yields.

We continue to believe that concentration and selectivity in one’s investments will pay off in the years to come as it has in years past. There is no excuse for not sticking to high quality in all of one’s investments. We have always believed that is the best prescription for avoiding any oversized losses in the long run. In the short run anything can happen, but in the long run quality, long duration earnings growth, and growing dividends will lead in our opinion, to growing one’s net worth. At FLI we offer our clients numerous ways to participate in that formula.

We believe that 2020 can be a successful year for our clients notwithstanding a potential increase in volatility from politics and geopolitical hotspots (including Iran/Iraq, Russia, and North Korea) that will inundate us with rhetoric and fear as well as the ups and downs of our various trade negotiations. Given the news bombardment all investors face, we will continue to focus on the long-term fundamentals of each of our investments. We will also continue to invest in secular growth trends through quality and dominant companies as well as stalwarts that reward shareholders with growing dividends for the foreseeable future. As stated several times, we do not anticipate a recession in 2020!

Most importantly, have a healthy and happy New Year. We hope you will join us for our web seminar on February 13, 2020 at 2PM EST where we will dig deeper into many of the items covered here as well as taking questions from attendees.

Best regards,

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. The views expressed are the views of Robert D. Rosenthal through the period ending January 14, 2020, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC.

FLI average performance figures are dollar weighted based on assets.

All performance data presented throughout this communication is net of fees, expenses, and incentive allocation through or as of December 31, 2019, as the case may be, unless otherwise noted.

FLI believes the information contained herein to be reliable as of the date hereof, but does not warrant its accuracy or completeness. This communication is subject to modification, change, or supplement without prior notice to you. Some of the data presented in and relied upon in this document are based upon data and information provided by unaffiliated third-parties and is subject to change without notice.

NO ASSURANCE CAN BE MADE THAT PROFITS WILL BE ACHIEVED OR THAT SUBSTANTIAL LOSSES WILL NOT BE INCURRED.

Copyright © 2020 by First Long Island Investors, LLC. All rights reserved.

First Long Island Investors was honored to host Jon Ledecky, co-owner of the New York Islanders, for an exclusive event with clients and friends of the firm at the Garden City Hotel on November 7, 2019. Mr. Ledecky has a prestigious background as a businessman. He is a Harvard alumni who pursued a career in venture capital. He went on to start his own office supplies business, U.S. Office Products, which eventually completed an initial public offering in 1995. Following his departure from U.S. Office Products in 1998, Mr. Ledecky would go on to purchase ownership stakes in two professional Washington sports teams, the Capitals and the Wizards, from 1998 to 2001, before purchasing a stake in the New York Islanders in 2014. After a two-year transition period, Mr. Ledecky became co-owner in 2016.

The event was a fireside chat between FLI’s Chairman, CEO, and Chief Investment Officer, Robert D. Rosenthal (past co-Chief Executive Officer and a minority owner of the NY Islanders in the 1990s) and Jon Ledecky. The conversation began with accolades for the Islander’s 10-game winning streak they had at the time. Mr. Ledecky pointed out the team-brand of hockey the players were bringing every night and how special the streak was given 6 veteran players were injured during the streak. The conversation then switched gears to the community. Mr. Ledecky stated that owning a sports team is the next best service for the community outside of running for office. It provides a platform with free-branding (news, radio, Instagram, Twitter, etc.) and large brand value through players and alumni that fans are passionate about. This can be used to provide a great service to the community off the ice. Hockey with a Heart, a program where the Islander’s spotlight a non-profit each game, is in its third year raising money and awareness for local charities with causes that range from cancer fundraising, military appreciation, food and toy drives, mental health, to gender equality, and beyond. The Islanders Children’s Foundation was created in 2003 to support and provide opportunities to local youth. The foundation has raised over $13 million dollars since inception. Mr. Ledecky is extremely proud of the philanthropic efforts he is able to promote through the Islanders and their leadership in the community.

Mr. Ledecky spoke about his other investments as a businessman and the sectors and trends that currently pique his interest. Mr. Ledecky suggested “walking the mall”, a strategy consisting of observing which stores were busy or empty, what products were being sold and what was not. Great companies such as Sunglass Hut and Pharmapax have come from understanding markets that are not served or can be served differently. Mr. Ledecky also touched on the transformation of business in recent history and three notable trends. The first was the continual shift in advertising dollars towards digital platforms, such as Facebook, Instagram, and Twitter, where there are millions of eyeballs every day. The second was the rising popularity in online gaming/E-sports that can provide many unique business opportunities in the coming future. The final trend was 5G technology that in his mind will change the world that we live in.

The conversation shifted to Belmont, the site where the Islanders are building their new arena. Mr. Ledecky was extremely excited about the opportunity to have a dedicated arena for the Islanders. Part of the strategy for the new site was having a strong partnership with a concert and events promoter that can secure concerts during times the Islanders are either away or in off-season to continue to generate revenue. Seeking advice from ownership of other sports teams that had managed a relocation was also a key step Mr. Ledecky took during the process. Mr. Ledecky and the Islanders hope to further enhance the surrounding area and its visitation appeal by building a 250 room hotel across the street with a retail footprint that is close to JFK airport. The project carries numerous benefits such as $2.7 billion initial economic spend, $600 million ongoing spend, thousands of new jobs, and the first new Long Island Rail Road station in 50 years, all of which is beneficial to the economy of Long Island.

Finally, the conversation switched back to hockey and the great relationship between front office and bench. Barry Trotz, head coach of the Islanders, and Lou Lamoriello, President and general manager of the Islanders, have made great strides since their arrival in New York. Mr. Ledecky knew Barry from his previous ownership of the Washington Capitals (where Barry Trotz previously coached and won a Stanley Cup). Lou Lamoriello was brought in through connections from Toronto and since uniting the two have done a terrific job with the organization. Mr. Ledecky ended the conversation by saying “If you’re an owner of a sports team, the best thing you can do is realize you’re not a general manager or coach.”

The investment process at First Long Island Investors involves many elements including company specific research and analyses, extensive dialogue with our outside managers on companies, sectors, and the markets overall, interaction with economists, both independent and those affiliated with large organizations, as well as the investment professional networks of our team members. Robert (“Bob”) Rosenthal, our Chairman, CEO, and Chief Investment Officer, is part of an investment “think tank” alongside longtime mentor and acclaimed investor, William P. Stewart, and other respected market analysts. Recently this group engaged in a conversation that was sparked by comments made by The Blackstone Group, one of the world’s largest private equity firms, and touches on the issues weighing heavily on many, including some clients. Bob’s perspective is below:

The current “wall of worry” is made up of concerns regarding: the timing of the next recession; the state of the (messy) political situation in Washington, including but not limited to the trade situation with China and ongoing impeachment proceedings; negative sovereign yields in Europe and Japan; IPOs of companies with no profits; income and wealth inequality; and other subjects.

While it is true that there is a fair amount to be concerned with, many (including Blackstone) are quick to ignore the strength of the consumer, continued GDP growth in the U.S., low unemployment, and growing corporate earnings. (We do not see a recession in the near future.) There is no distinction being made by Blackstone between high priced bonds and private equity versus a reasonably valued, but not cheap, stock market. And of course, their approach takes a “market” perspective instead of viewing the opportunity through the lens of a concentrated portfolio of fine growing businesses, which is what we at FLI utilize for client assets and our own assets.

Of the various concerns we are hearing, the biggest is the unknown effects of negative sovereign interest rates. These negative rates are also keeping our treasury rates lower as Europeans and Japanese investors buy our bonds to earn a positive return on their capital. The thought is that negative rates will boost economic growth in those regions. I do not know if this will prove true and we at FLI have underweighted foreign equity investment as we do not like the lack of growth and socialist tendencies in many countries (e.g. France). The outcome of these negative rates is one we will be sure to watch.

In looking at valuation excesses we reference late 1999/early 2000 when the S&P 500 was trading at a price-to-earnings ratioi of 31 and the ten-year Treasury was 6.5%. These numbers are quite different from today, but that is not to ignore the point that the equity market is not cheap today. Furthermore the great businesses that are leaders in secular growth including credit cards/electronic monetary transactions, cloud computing, and streaming of content (to name a few) do not typically trade at 100 times earnings as they might have back in 2000. Valuations are loftier for durable growing businesses perhaps, but not nose bleed by any stretch.

It is easy to find danger in a bull market lasting ten years. It is easy to worry about very low interest rates and central banks trying to stimulate growth and employment. It is easy to look at IPOs where the share price declines after going public at absurd valuations while they seek their first dollar of profit. It is easy to paint a bleak picture of business growth in the midst of a trade war. It is also easy to fear the unknown of a political situation that could lead to socialism in the greatest economy in the world. But it is harder to stay the course with a prudent allocation to fine businesses that can see growth for years to come or companies that have strong balance sheets and offer stability, growing dividends and market dominance. This, in our opinion, is the alternative to very low to negative interest rates on sovereign debt or bloated private equity funds chasing too few really good investments, especially when most consultants have for years shunned the domestic equity market and pushed clients into private equity and hedge funds.

At the end of the day, things have not changed. A prudent asset allocation reflecting current valuations for each asset class category coupled with the recognition of one’s age, goals, and risk profile, while never losing sight of needing to invest for the long term (which will vary for each individual), makes the most sense. But as we all know, there is always a “wall of worry” to be navigated.

So, we remain cautiously optimistic; we are somewhat defensive; and we are concentrated in our investments. We do not own a “deworsified” portfolio in any of our strategies. Third quarter earnings have come in very well for the market in general and specifically for the companies we invest in. Guidance is also quite reasonable. Our Dividend Growth strategy is enjoying a strong year with dividend growth increasing for the portfolio by 10.4% on average. (The strategy for the year is up over 22% which more than makes up for a slight loss last year of minus 4.4%.) The two-year average appreciation is not at a nosebleed level nor are the valuations. As for the market as a whole, currently the S&P trades at a P/E of 20.9i, which in an environment of a ten-year Treasury at 1.9% to us is also not nosebleed by any means. For perspective, the dotcom bubble in late 1999 traded at a P/E of almost 31i when you could buy a ten-year Treasury at 6.5%. That was considered nosebleed territory with a bond alternative that was attractive. That is not the case today.

In summary, we have a defensive tilt; we are long term investors; we invest in concentrated strategies with companies that are doing well and have financial strength. The environment of investing always has a wall of worry. Today is no different, but the fundamentals still suggest that gains can be achieved.

A synopsis of the Blackstone interview can be found here:

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. Performance information for FLI Dividend Growth represents the performance of its composite. The views expressed are the views of Robert D. Rosenthal through the period ending December 10, 2019, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

Content may not

be reproduced, distributed, or transmitted, in whole or in portion, by any

means, without written permission from First Long Island Investors, LLC.

Copyright © 2019 by First Long Island Investors, LLC. All rights reserved.

i Price-to-earnings ratio is based on a trailing twelve-month basis

Philanthropy is one of the many topics we often find ourselves discussing with clients, especially as the holidays draw near and people want to have a positive impact on the community while ensuring they do so in the most beneficial way.

Charitable giving can be accomplished using cash, securities (appreciated securities are an excellent choice), or other assets. These assets can be given directly to a charity or indirectly through a donor advised fund or private foundation. In the last decade the use of donor advised funds (DAF) has risen significantly for a variety of reasons, most notably that a donor can make a contribution to a DAF and in most cases take an immediate tax deduction. The funds can then be invested for tax-free growth while deferring the decision of which charities will receive the monies and when. For example, if you set up a DAF in 2019 and immediately contribute $500,000 you can take that tax deduction (with certain limits) and then spread the giving over the next decade, distributing $50,000 or more per year to charities without further contributions to the DAF (assuming no net depreciation of the DAF’s assets).

Donor advised funds are gaining in popularity over private foundations because they streamline record keeping, are not subject to IRS annual minimum distribution requirements, have no legal or accounting costs to the donor, and typically allow the donor to choose the investment advisor to manage the DAF’s assets. DAF’s typically charge an administrative fee.

In response to the growing demand for donor advised funds and the desire of our clients to designate how their funds are managed before being distributed to the ultimate charitable beneficiary, FLI is pleased to share that FLI Dividend Growth and FLI Core are now approved strategies with both the Jewish Communal Fund and The UBS Donor-Advised Fund (each with a $500,000 minimum contribution). Both of the organizations are well-established donor advised funds whereby the donor can select any IRS-qualified public charity as a recipient from the DAF.

We look forward to discussing how donor-advised funds can play a role in your family’s charitable giving and would be happy to do so in conjunction with your tax advisor. Please keep in mind that the deadline for contributions to be income tax deductions this year is December 31st. These accounts take a little time to set-up, so if you would like to do so before year-end, we ask that you contact us by December 10th or we can help you set one up in 2020.

First Long Island Investors was honored to have Dr. Richard Barakat speak to clients at our recent Thought Leadership Breakfast. Dr. Barakat is Physician-in-Chief and Director of the Northwell Health Cancer Institute and Senior Vice President of Cancer Services at Northwell Health. Prior to joining Northwell Health, Dr. Barakat spent almost three decades at Memorial Sloan Kettering Cancer Center, serving as Head of Gynecology Cancer Services for 14 years before becoming the leader of the organization’s entire network. Dr. Barakat helped standardize practices across different locations and organizations, ensuring patients would have convenient access to cancer care without the need to travel to Manhattan. His successful integration and leadership put him on the radar of Northwell Health, which was in need of a physician-in-chief who could help expand the Cancer Institute’s programs and services.

Dr. Barakat began the conversation by shedding light on the brutal facts of cancer:

- In 2018, 9.6 million deaths were caused by cancer and 18.1 million new cases were reported globally.

- In the US alone, there will be approximately 1.7 million new cases this year and 600,000 deaths.

- One out of every eight women and one out of every ten males are diagnosed with some form of cancer in their lifetime.

- A third of cancer cases are either lung, breast or colorectal

- A third of cancer related deaths could be eliminated by dietary and lifestyle changes.

- Currently, there are 10.9 million cancer survivors in the US, and the cost of cancer is expected to reach $173 billion by 2020.

The conversation shifted to the treatment of cancer with a focus on the advancements being made in the treatment and quality of life care. Three areas of research are being emphasized at Northwell: precision medicine, immunotherapy, and CAR-T therapy.

Precision medicine is an approach where doctors treat patients based on a genetic understanding of the disease. All cancers have a genetic basis which can differ from patient to patient, even in the same affected organ. Tests can be conducted to determine which mutation is responsible for the cancer’s origin. Precision medicine involves the creation of drugs that target these mutations. This method is agnostic to the type of cancer and treatment is based on the cancer mutation rather than the tumor histology. One form of treatment in precision medicine is a PARP inhibitor. PARP is a protein found in our cells that helps damaged DNA repair itself. The inhibitor stops PARP proteins in cancer cells from repairing the cancer cells and the cells die off.

Immunotherapy treatments either help the immune system attack the cancer directly or stimulate the immune system in a targeted way. Cancer cells develop proteins that attach to and block the proteins on our body’s T-cells, the cells that defend our body from infectious germs and diseases. One form of immunotherapy is the use of checkpoint inhibitors. Some cancer cells make high levels of proteins. These can switch off T-cells, when they should really be attacking the cancer cells. Checkpoint inhibitor drugs stop the proteins on the cancer cells from switching off T-cells. This turns the immune system back on and the T-cells are able to find and attack the cancer cells. The drawback to checkpoint inhibitors is that the drugs are very potent with strong potential side effects.

CAR-T therapy, or chimeric antigen receptor T-Cell Therapy, is a treatment that alters T-cells to make them more effective at fighting cancer cells. CAR-T therapies induces complete remission in approximately 80% of patients. This therapy has been extremely effective for patients with leukemia and lymphoma. While effective, the therapy has been too expensive for many, costing near $400,000. Fortunately, Medicare is now covering treatment nationwide when it is administered at health care facilities enrolled in an FDA-mandated safety program requiring special training on handling side effects.

Dr. Barakat stated that recently the FDA has approved 13 new targeted therapies within precision medicine, 5 new checkpoint inhibitors, and the first adoptive cell immunotherapy. These are promising steps. An issue raised by Dr. Barakat was the insufficient attention given to survivorship post –cancer. More than 18% of the United States’ GDP is spent on health care (the highest of any developed country and the most per capita), yet our life expectancy is well below many countries. A primary reason for this is a lack of access to premier medicine around the country. Many of the country’s best hospitals and institutes are highly concentrated in certain areas leaving few choices for patients who are not fortunate enough to live in close proximity to dedicated cancer institutes.

For many, historically the best treatment available is in New York City. Traveling from Long Island into the city may not be a viable option for ill patients. Dr. Barakat believes Northwell is creating a leading Cancer institute on Long Island to help combat this issue. He cited that they are in the process of replacing Lenox Hill Hospital in NYC with a state-of-the-art 450 bed acute care hospital of the future. Northwell is also improving the quality and scope of cancer services delivered in its Long Island facilities. Dr. Barakat also pointed to Northwell’s ability to treat pregnant patients suffering from cancer at its Center for Cancer, Pregnancy and Reproduction, one of the nation’s first cancer programs dedicated specifically to pregnant women. 41,000 births occur at the Northwell location and one in every thousand pregnant women will be diagnosed with cancer. “No other center exists in the New York area that can offer this scope of services with experts working seamlessly together,” Barakat said.

Dr. Barakat brought a profound and stimulating conversation to clients that unearthed many oversights of cancer while sharing the encouraging advancements and steps being taken to fight off one of the world’s most deadly diseases.