June 30, 2023

“You must force yourself to consider opposing arguments. Especially when they challenge your best loved ideas.”

– Charlie Munger

The second quarter and first half of the year, from an investment standpoint, offered many challenges, but resulted in bifurcated yet positive results. More growth-oriented companies saw a decisive comeback from last year’s challenges. More value-oriented companies witnessed moderate gains after outperforming on a relative basis last year. Stock market indices gained for the quarter and year-to-date, but the results of most companies varied significantly from the outsized gains of a very small number of growth companies. As discussed below, the S&P 500 Index, on its face, can be a misleading indicator of the market’s overall performance.

The S&P 500 Index has in some cases been renamed the S&P 493. On a traditional market-cap-weighted basis, the popular average gained 16.9%, while on an equal-weighted basis, the average gained only 7.0%. The seven largest companies, on average, gained 89%, while last year they lost 46%, on average. Using valuation as a significant metric to consider, the S&P 500 Index is trading at a price-earnings ratio of 18.2x on projected 2024 earnings, while on an equal weighted basis, it is trading at a price-earnings ratio of 14.3x on projected 2024 earnings. Certainly, the equal-weighted price-earnings ratio on projected 2024 earnings is not alarming and, if anything, appears attractive. Of course, that is with companies all equally weighted and dulls the effect of the seven companies leading the appreciation charge this year. Please remember, these are estimated price-earnings multiples based on projected 2024 earnings, which do not reflect the effect of a potential recession as of this date.

The cause of this strange performance bifurcation was the unprecedented spike in interest rates driven by the Fed over the past 16 months, in our humble opinion. Never in modern U.S. history have rates risen from near 0% to 5.25% in that short of a period. This crushed growth stocks (think Amazon.com, which declined 50% last year), with the Russell 1000 Growth Index dropping 29.1%, only to rebound thus far this year by 29.0% (with Amazon.com rising by 55% year-to-date). Meanwhile, value-oriented companies held up better than growth stocks last year with the Russell 1000 Value Index being down 7.5% (think Johnson & Johnson, which last year appreciated by 6%), while this year the index is up a modest 5.1% (with Johnson & Johnson down a modest 5%). So far, in our opinion, our strategy at FLI of having our clients maintain a prudently diversified asset allocation that includes both value and growth stocks has led to some happiness for virtually all of our clients.

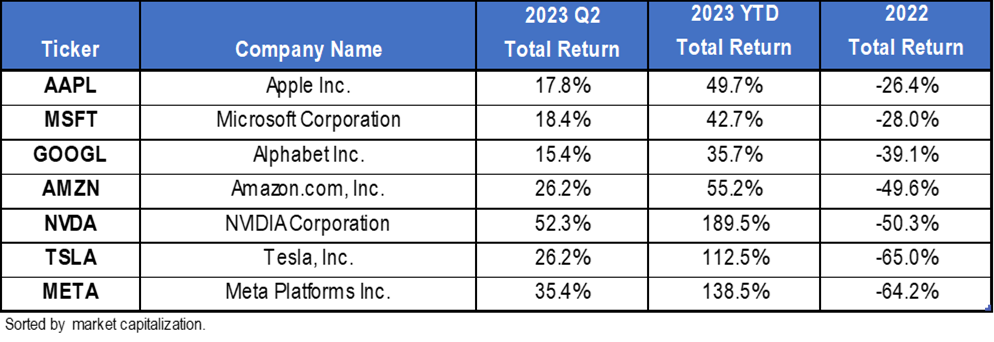

To give you some more specifics, here is a list of the seven S&P 500 Index companies leading the charge thus far this year versus how they fared in 2022: (We do not claim to have owned all of these companies but we do currently own the majority of them in a number of our strategies):

The above results demonstrate the crushing effect, in our opinion, that the spike in interest rates and supply chain disruptions had in 2022. It also portrays how the recovery stems from what most believe is the near end of interest rate increases, declining inflation, and the momentum caused by the recent focus on potential disruptive technology, particularly artificial intelligence (AI). If your portfolios contained these seven companies, you most likely have enjoyed huge gains. Of course, most portfolios are diversified and may own most of these seven companies (aggressive growth), some of these companies (growth-oriented strategies including core portfolios), or perhaps none of these companies if you are exposed to a highly value-oriented portfolio, which is likely in the last case as most of these companies pay no dividends or tiny ones that are not typical of value-type companies.

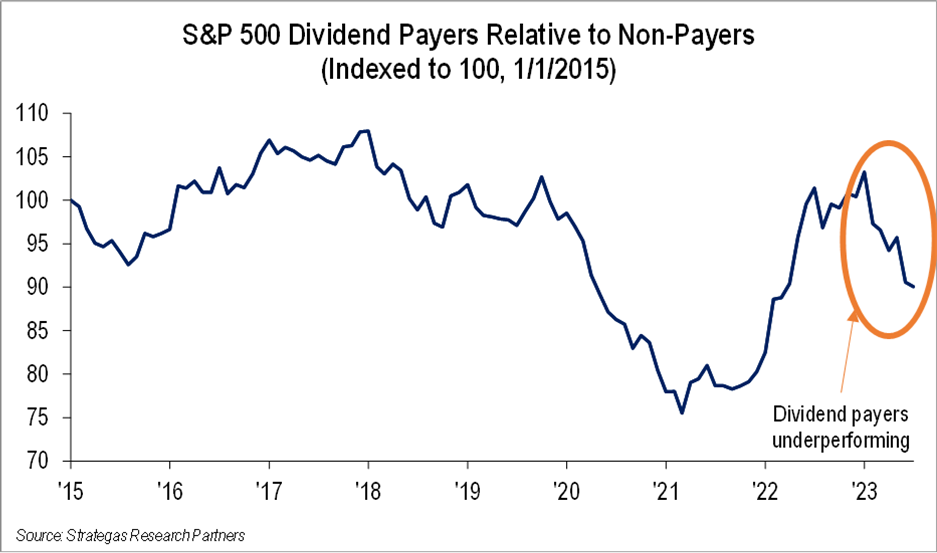

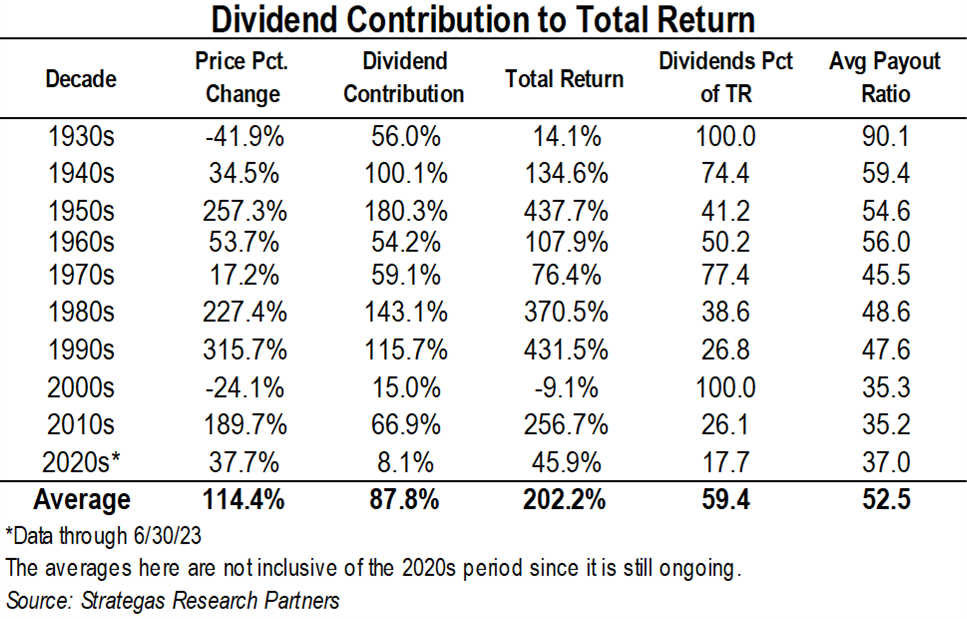

To boot, since I mentioned dividends, dividend paying stocks did not fare so well versus non-dividend-paying stocks for the first six months of this year as evidenced by the below chart. As you know, we offer a dividend growth strategy that has compounded at over 10% net* a year since its inception over 13 years ago, where an above-average dividend yield and dividend growth are paramount.

Our more growth-oriented strategies had a strong second quarter and year-to-date (gains of 7% to 18% net*) while our value-oriented strategies (both spanning our defensive and traditional baskets) had more modest gains (2% to 9% net*). The mix of both growth-oriented and value-oriented strategies has led to a good rebound from last year thus far for virtually all of our clients.

At the same time, our advice from March to have a buffer of short-term U.S. Treasury Bills to help weather the uncertainties we are facing (the proverbial “Wall of Worry”) has led to client’s earning current annualized yields of approximately 5% or more. Not so bad after U.S. Treasury Bills had yielded virtually nothing for many years and the 10-year U.S. Treasury was actually down 17.8% last year.

So, What Gives?

The referenced “Wall of Worry” consists of the following questions (that we know of), which are challenging and give us cause for pause and reflection:

· When will the Fed stop raising interest rates, and for how long will they remain elevated?

· Will inflation continue to abate?

· Will the recommencement of student loan repayments have a material effect on consumer spending?

· Is there a recession on the immediate horizon?

· If so, will the recession be a deep one?

· Will the geopolitical picture worsen?

· Will the political divisions plaguing our country get better or deteriorate even further?

· When will normality return from the COVID-19 hangover?

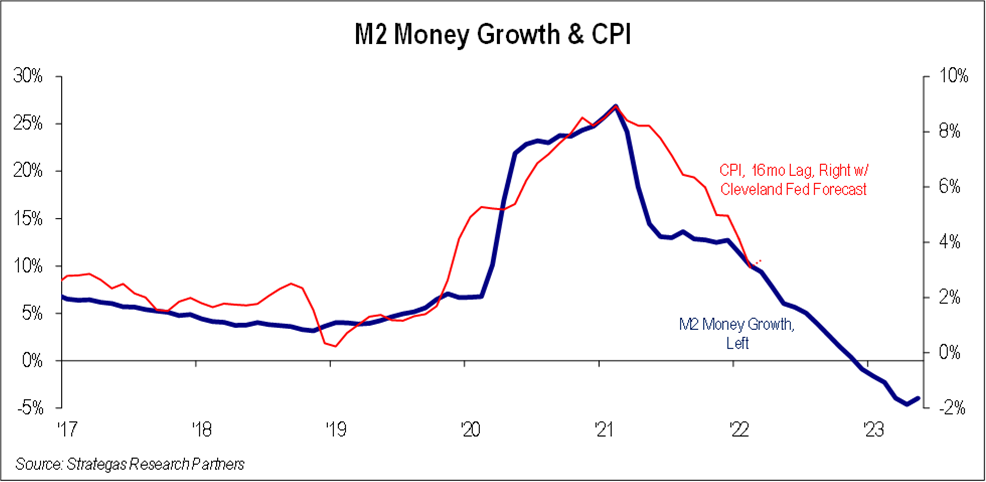

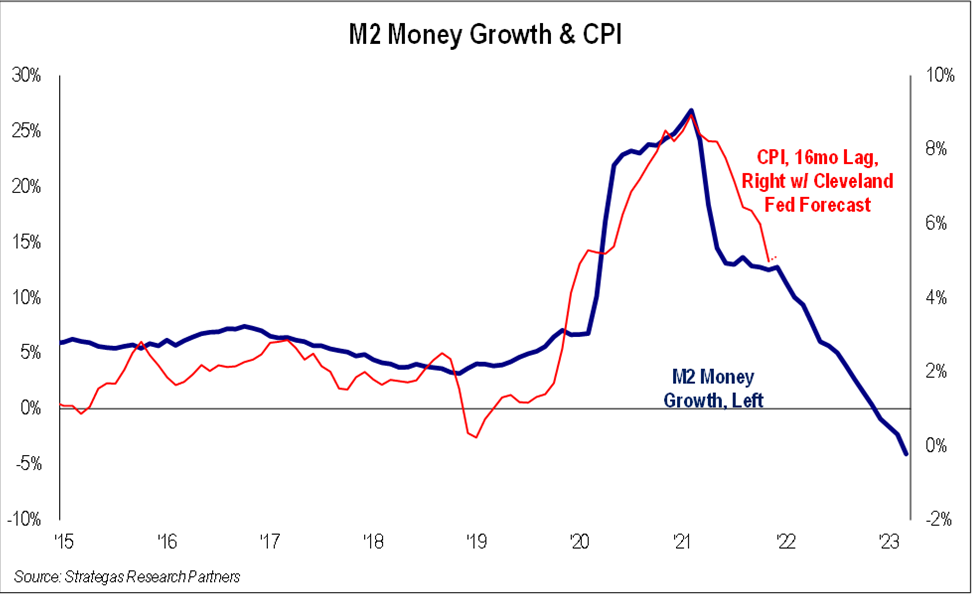

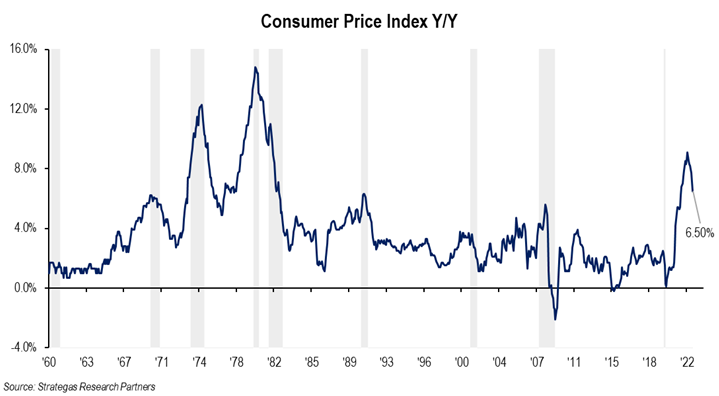

In answering the above, let us start with our view on interest rate increases and inflation. The following chart, which we have referenced in the past, shows that negative trending monetary growth is typically followed by a decline in inflation:

As you can see, as monetary growth declines, inflation typically follows within 16 months or so. Currently, we have negative monetary growth, which has not occurred since the Great Depression (except for one month of de minimis negative growth in 1958). In our opinion, this should lead to, and already is leading to, a decline in inflation, which should give the Fed the ability to pause its interest rate increases by the end of this year when we expect inflation to be in the 3% to 4% range or possibly even lower. This should be good for the equity markets, including both growth and value stocks. We could also see a broadening of performance within the S&P 500 Index, where quality value stocks make up some ground on growth stocks, which seem to have, in certain cases, somewhat stretched valuations, in our opinion. An improvement in the performance of value stocks would be healthy for diversified investors.

However, slowing inflation and declining monetary growth should also slow our economy. In a perfect world, maybe recession is avoided. In our view, it is inevitable and we hope it does not impact us as investors until sometime in 2024. The counter view to an imminent recession is stubbornly strong employment, despite these rate increases and quantitative tightening (shrinking of the Fed balance sheet). Renewed economic growth in China and federal spending prior to the 2024 presidential election cycle could also fend off recession. However, a war raging in Ukraine, a cold war with China, and certain Middle Eastern countries seemingly getting friendlier with the Communist Chinese also could contribute to what may be an inevitable recession and declining corporate profits, in our opinion.

In any event, we believe that a recession will be modest because of robust employment, even if that worsens somewhat, along with strong balance sheets for most companies including our major banks, which just passed a somewhat more stringent stress test. We are still keeping a careful eye on commercial real estate, particularly office buildings, where declines in value have occurred because of higher interest rates and the decline in office occupancy from the relatively recent phenomenon of “remote working” stemming from the COVID-19 pandemic. Additionally, geopolitical instability is something we must become more accustomed to. A near coup in Russia and a cold war brewing with China gives us pause and cause for concern. The resulting need for an even stronger U.S. military to counter these geopolitical stresses will also cause budget woes as our government must eventually deal with our growing debt and the cost of carrying that debt. Certainly, this will be an issue in the upcoming 2024 presidential election cycle along with many other economic and social issues.

Our Challenge: Invest for the long term in quality equities and real estate or hide out in cash?

When times are fearful as now, it is typically a good time to invest for the patient long-term investor. U.S. Treasury Bill yields will ultimately come down, in our opinion, likely sometime over the next year or so. Over the long term, cash or short-term liquid investments (other than maintaining a prudent buffer) have been a relatively poor returning asset class despite feeling attractive at this time.

In spite of dividend paying stocks only moving modestly higher thus far this year, over the long run we believe dividends will contribute to meaningful appreciation as they have historically. We still believe in this beloved concept that requires patience but has rewarded investors over the long term:

A poor 2022 and a current “Wall of Worry” can make us challenge our own long-term assumptions about investing. But with any thought and reflection, common sense investing still means having a prudently diversified asset allocation among quality bonds and mostly companies generating earnings growth, free cash flow, and returning cash to shareholders through dividends and buybacks, all while utilizing a valuation filter. This should be our compass. The same goes for real-estate-type investments, where location and cash flow will reward investors. Of course, everyone’s asset allocation must reflect their individual life circumstances and the advice of trusted professionals like the investment team at First Long Island Investors.

So, our long-held ideas mentioned in the preceding sentences still resonate with us. Yesterday was the internet and today we look to the prospects of AI and blockchain being disruptive opportunities. We might have to be patient, absorb some volatility, and look over the valley of periodic investment setbacks. Wealth compounding is a long-term proposition. Wealth growth above inflation requires some measured risk taking. We believe that FLI is up to the task of navigating these uncertain waters. Having faced difficult investment environments over the past 40 years (FLI is celebrating its 40th anniversary this year), gives us confidence in our ability to sail these challenging investment waters. As we have often quoted Warren Buffett, “never bet against America”!

Please do not hesitate to contact anyone on our investment and wealth management teams should you need assistance or guidance in your wealth and money management needs.

Have a wonderful summer!

Best regards,

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

DISCLAIMER

The views expressed herein are those of Robert D. Rosenthal or First Long Island Investors, LLC (“FLI”), are for informational purposes, and are based on facts, assumptions, and understandings as of July 26, 2023 (the “Publication Date”). This information is subject to change at any time based on market and other conditions. This communication is not an offer to sell any securities or a solicitation of an offer to purchase or sell any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

This communication may not be reproduced, distributed, or transmitted, in whole or in part, by any means, without written permission from FLI.

All performance data presented throughout this communication is net of fees, expenses, and incentive allocations through or as of June 30, 2023, as the case may be, unless otherwise noted. Past performance of FLI and its affiliates, including any strategies or funds mentioned herein, is not indicative of future results. Any forecasts included in this communication are based on the reasonable beliefs of Mr. Rosenthal or FLI as of the Publication Date and are not a guarantee of future performance. This communication may contain forward-looking statements, including observations about markets and industry and regulatory trends. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect the views of the author as of the Publication Date with respect to possible future events. Actual results may differ materially.

FLI believes the information contained herein to be reliable as of the Publication Date but does not warrant its accuracy or completeness. This communication is subject to modification, change, or supplement without prior notice to you. Some of the data presented in and relied upon in this document are based upon data and information provided by unaffiliated third-parties and is subject to change without notice.

NO ASSURANCE CAN BE MADE THAT PROFITS WILL BE ACHIEVED OR THAT SUBSTANTIAL LOSSES WILL NOT BE INCURRED.

Copyright © 2023 by First Long Island Investors, LLC. All rights reserved.

March 31, 2023

“Out of intense complexities intense simplicities emerge.”

– Winston Churchill

The first quarter of 2023 was highlighted by positive results for the major indices despite significant volatility and what we will call, at this point, a mini banking crisis. This crisis, in our opinion, was brought on by the meteoric rise in interest rates over the past twelve months and resulted in a depositor run on two regional banks that led to their closure; the forced acquisition of Credit Suisse by its neighbor UBS; and the closure of a smaller bank brought on by its exposure to cryptocurrency. To say the least, this first quarter compressed good news, bad news, uncertainty, continuation of a war, and the coming together of a new potential axis of evil (Russia, China, and Iran).

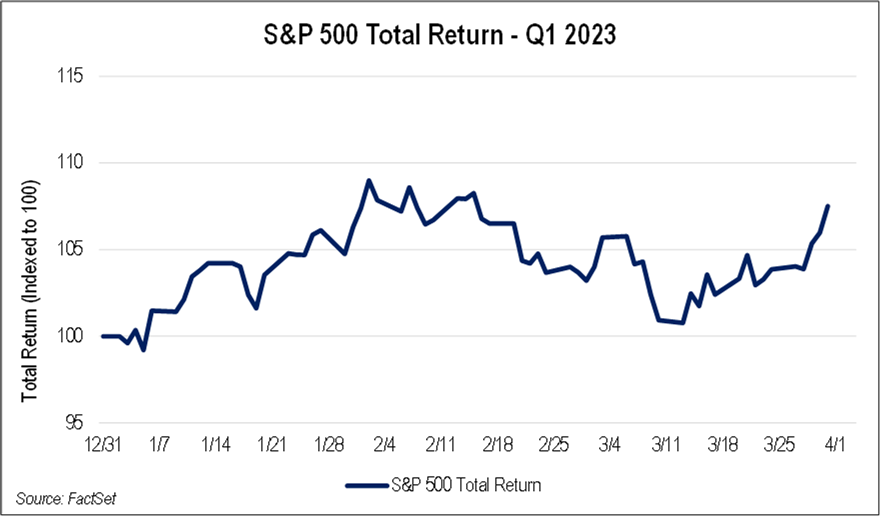

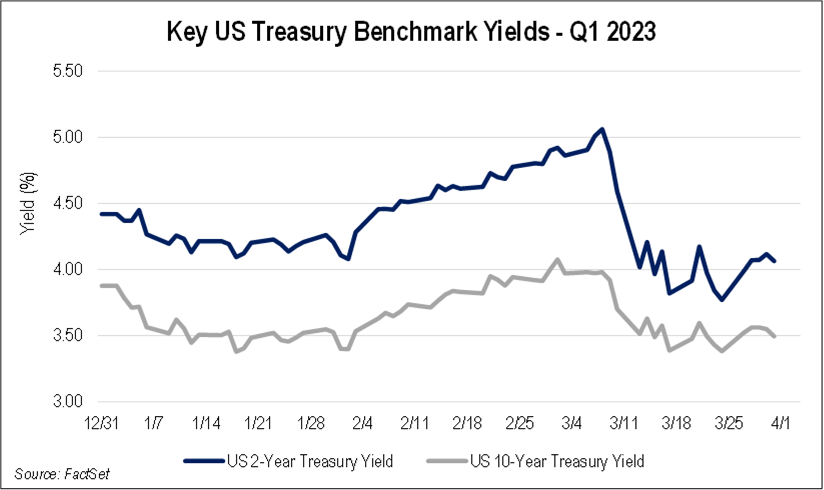

After a terrible 2022, equity markets started strongly in January only to be derailed in February by stronger (worse) than expected inflation news; strident rhetoric by the Fed along with two 25 basis point interest rate increases; fears of a recession; and then the unthinkable closing of both Silicon Valley Bank and Signature Bank. The following chart depicts the gyrations in Q1 for the S&P 500:

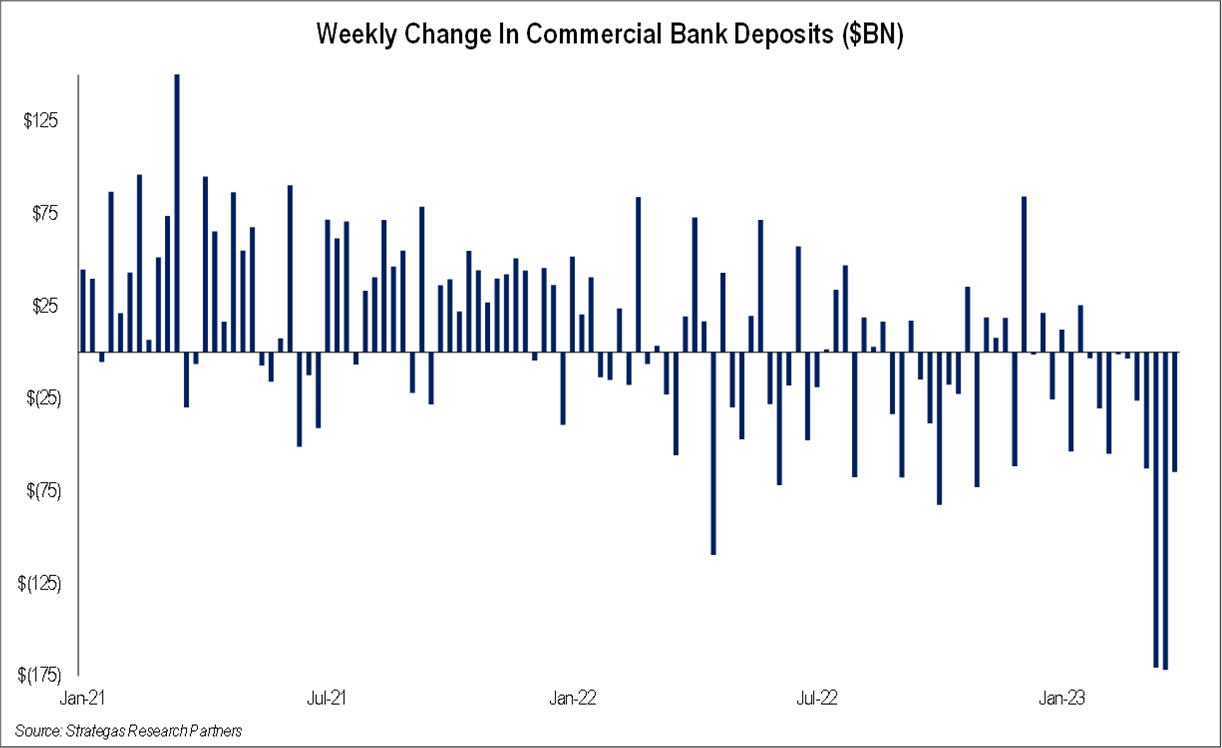

At the same time, while this dreary set of financial events occurred, many investors sought cover in U.S. Treasury Bills, Notes, and Bonds where short-term yields even reached a bit above 5% for a period of time. Short-term yields reached the highest levels in over a decade and turned out to be a very attractive asset class to hide out in. The following chart shows the significant outflow of funds from bank deposits, much of which found its way to U.S. Treasuries and money market funds:

What came into focus was the lack of deposit insurance above the FDIC limit ($250,000 for individuals as an example). Despite the overall strength of our banking system, as evidenced by last summer’s stress test of the 34 largest banks, panic and fear started to prevail. This impacted the stocks of all banks but in particular, regional and super-regional banks. Meanwhile, growth shares outperformed value-oriented stocks in an about-face from last year when growth shares were trounced as an asset class category. The concerns about the strength of our banking system led many investors to believe that the Fed would be forced to cut rates to stem this banking crisis, which brought back the horrible memories of the Global Financial Crisis of 2008/2009. Treasury Secretary Janet Yellen, after consultation with other government officials, stepped in with an FDIC plan to insure all deposits above the FDIC threshold for these two regional banks. At the same time, a number of large banks stepped in with thirty billion dollars of temporary deposits to bolster another bank facing massive outflows, First Republic Bank. Secretary Yellen has been unclear as to whether this guaranty of all deposits above FDIC limits will be available should any other banks fail.

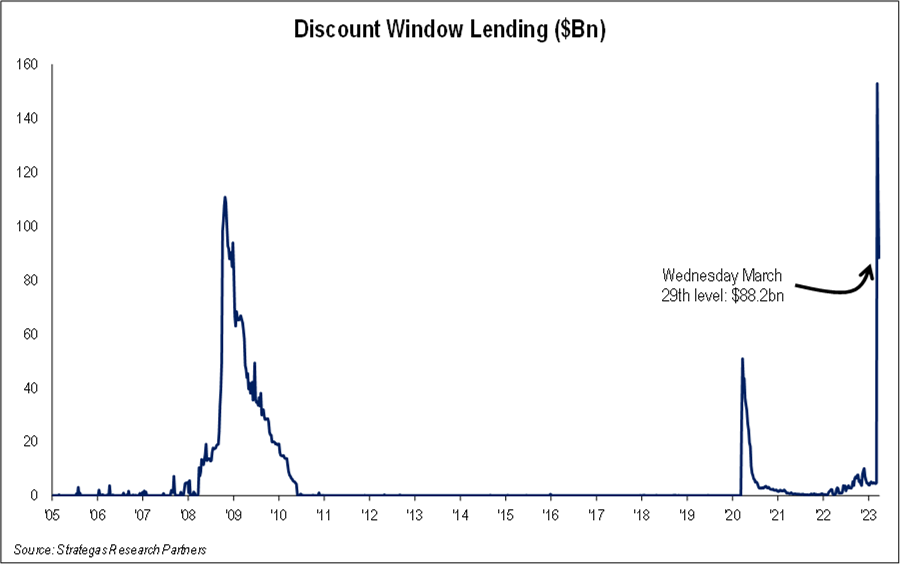

As of this writing, it appears that this mini bank crisis has been contained. The trouble caused by rapidly rising interest rates, combined with some banks mismanaging their balance sheets by purchasing long-dated U.S. Treasuries while paying depositors paltry interest rates, however, has not gone away. This situation could result in more restrictive lending policies as banks try to manage the temporary paper losses they have from long-dated bonds purchased during a much lower interest rate environment. To help minimize this mini bank crisis and in addition to the Fed affording banks the opportunity to avail themselves of using the Federal Reserve discount window, the Fed introduced a new program called the Bank Term Funding Program where banks can borrow at face value against the U.S. Treasuries, agency debt, and mortgage-backed securities they own, many of which are underwater (a scary picture in the chart on the top of the next page). The government infused about $300 billion into the financial system in the last weeks of the quarter.

The cost of insulating depositors from this crisis will probably be borne by other banks through increased fees, as was the case after the 2008/2009 Global Financial Crisis. Another factor to be watched is the impact this will all have on commercial real estate. Rates to refinance have more than doubled, and cash flow for real estate borrowers in some cases has declined as utilization of office space has remained poor post the COVID-19 pandemic. Another crisis could emerge and must be watched carefully while banks will likely increase loan loss reserves in anticipation of this problem.

On the brighter side, towards the very end of the quarter, inflation started to moderate once again. This is key to the future path of interest rates and will guide the Fed’s interest rate policy. It was also reflected in the bond market with weaker short-term yields, at least for now. The chart below shows how shorter-term rates rose during the quarter, only to fall as the mini banking crisis emerged and the quarter came to an end. With the decrease in short-term rates, equity markets (and in particular, the growth-oriented NASDAQ Composite) rallied.

It is our view that in the very short term, interest rates will fluctuate with monthly data on inflation as well as if there are any additional bank closures. It is well known that economic activity will be impacted by the past rise in interest rates with a delay of anywhere from six months to a year. As a result, economic activity, including employment, should moderate in the near future if not eventually lead to what we believe will be a modest recession. This should reduce inflation and, at the least, cause the Fed to stop increasing interest rates and possibly lead to rate cuts (we believe the Fed will pause at this point). This is likely to be good for the equity markets and ease pressure on commercial real estate.

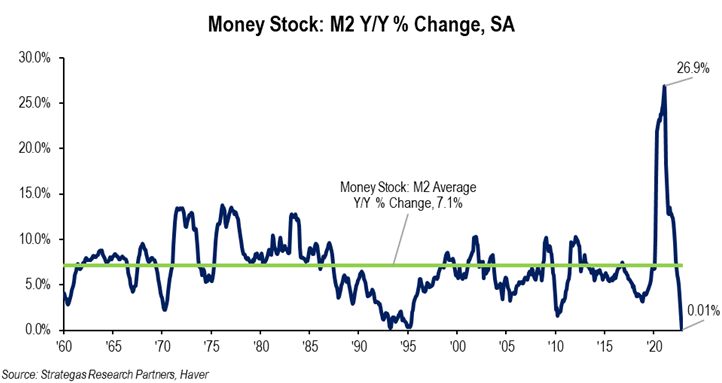

The chart above is one that we believe demonstrates that the growth in money supply (M2) has been a reliable forecaster, with a lag, of inflation as measured by the CPI. The enormous monetary growth caused by the government stimulus in response to the COVID-19 pandemic resulted in a large spike in inflation. Now that the stimulus programs have ended, M2 growth has collapsed. We are optimistic that inflation will fall as M2 growth is now negative on an annual basis for the first time that I can remember or for that matter in history.

In our opinion, it appears that inflation will be tamed by the meteoric rise in interest rates; the improvement in supply chain issues; continued layoffs, especially in the tech sector, which should lessen wage inflation; and the reduced excess savings that consumers have at their disposal.

That leaves only two major issues for us as investors to be concerned with as we try to build on the improved equity market performance of the first quarter, those being earnings and the other being the alarming geopolitical situation. As for earnings, the impact on banks’ results due to the confluence of cash sorting (moving from deposits to money market funds and U.S. Treasuries) and additional fees, as well as stricter regulations, will impact the industry’s profitability going forward. A general slowdown in the economy caused by the ultimate impact of higher interest rates will also impact earnings for some companies. Oil prices have declined since the beginning of the year, which should also reduce oil company profits. Geopolitical factors (the growing closeness of Saudi Arabia and Iran) and the improvement in the Chinese economy, however, could bolster prices at some point. Finally, the resilience of the consumer will be tested as their excess savings dwindle with government handouts to many having ended. Thus, the earnings picture for the S&P 500 Index and many smaller companies will probably slow and could decline from 2022 levels this year.

As earnings may turn down for some companies, it will be a stock pickers market. We will, as always, look to companies with growing earnings, despite the economic slowdown, as well as companies that can continue to grow their cash dividends above inflation (dividend growth in 2022 was 11.8% on average for our Dividend Growth strategy and thus far is averaging 8.4% in 2023 with more than half the portfolio not yet scheduled to announce dividend increases). The outside managers we work and counsel with remain steadfast in their belief that their portfolio companies will grow their earnings in 2023. Should the Fed pause and inflation trend down, we believe those companies we invest in that can continue to prosper will be rewarded with higher share prices. We also expect dividend growers that can outpace inflation to be rewarded as they have in the past.

Summary

To paraphrase our quote, significant complexity demands intense simplicities. To us at FLI, simplicity is a prudent, diversified allocation to short- and medium-term, high-quality fixed income; a continued overweight to our defensive strategies (where we have concentrated exposure to both quality growth and value companies as well as certain hedged credit opportunities); and a continued allocation to traditional equities where high-quality, undervalued companies with consistently growing earnings will reward long-term investors seeking comfort in uncertain times. We continue to underweight international exposure while also reducing our exposure to banks. To us, the current risks overseas, as well as what legislative and regulatory burdens will impact banks is too hard to handicap, including the possible severity of commercial real estate problems (mainly office buildings).

We are pleased that the choppy and volatile first quarter ended in positive fashion, while U.S. Treasury Bonds (longer term) eked out a positive return after their worst year in over 90 years. Uncertainty and complexity remain, both economically and geopolitically. We remain vigilant as we seek high-quality investments that are intensely simple solutions to the current complex investment environment. We continue to have conviction in our four investment baskets over the long term.

We are proud to announce that Dylan Klein, Assistant Vice President—Private Wealth Management, has passed level three of the CFA® exam and is now a CFA® charterholder.

Please call upon us with any of your investment and wealth management needs.

Best regards,

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

PS: It is premature to discuss the approaching 2024 election cycle, as well as the historic criminal indictment of a former President who is also an announced candidate for the Presidency in 2024 and ongoing investigations of the family of the current administration. Both situations can and will likely add to volatility. More to say in the future.

CFA® is a registered trademark owned by CFA Institute.

DISCLAIMER

The views expressed herein are those of Robert D. Rosenthal or First Long Island Investors, LLC (“FLI”), are for informational purposes, and are based on facts, assumptions, and understandings as of April 27, 2023 (the “Publication Date”). This information is subject to change at any time based on market and other conditions. This communication is not an offer to sell any securities or a solicitation of an offer to purchase or sell any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

This communication may not be reproduced, distributed, or transmitted, in whole or in part, by any means, without written permission from FLI.

All performance data presented throughout this communication is net of fees, expenses, and incentive allocations through or as of March 31, 2023, as the case may be, unless otherwise noted. Past performance of FLI and its affiliates, including any strategies or funds mentioned herein, is not indicative of future results. Any forecasts included in this communication are based on the reasonable beliefs of Mr. Rosenthal or FLI as of the Publication Date and are not a guarantee of future performance. This communication may contain forward-looking statements, including observations about markets and industry and regulatory trends. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect the views of the author as of the Publication Date with respect to possible future events. Actual results may differ materially.

FLI believes the information contained herein to be reliable as of the Publication Date but does not warrant its accuracy or completeness. This communication is subject to modification, change, or supplement without prior notice to you. Some of the data presented in and relied upon in this document are based upon data and information provided by unaffiliated third-parties and is subject to change without notice.

NO ASSURANCE CAN BE MADE THAT PROFITS WILL BE ACHIEVED OR THAT SUBSTANTIAL LOSSES WILL NOT BE INCURRED.

Copyright © 2023 by First Long Island Investors, LLC. All rights reserved.

2022 was a difficult year for most markets. What does 2023 hold in store? How will elevated interest rates impact the economy and the equity markets? How much farther will the Fed go in raising interest rates in 2023? When will the next recession begin and how severe will it be?

These are just some of the questions we hear from clients and business partners. In this web seminar we share our current outlook for the markets as well as how we are positioning client portfolios for long-term growth.

DISCLAIMER

This presentation has been prepared for informational and educational purposes only by First Long Island Investors, LLC (“FLI”). This presentation should only be considered current as of February 16, 2023 (or as otherwise indicated in the presentation) without regard to the date on which it was received or accessed. As a consequence, events may transpire subsequent to the date of this presentation that can render the contents inaccurate or obsolete. FLI believes the information contained in this presentation to be reliable as of the presentation date but does not warrant its accuracy or completeness. No party is obligated to update the contents of this presentation. However, FLI maintains the right to delete, modify or supplement this presentation without prior notice.

The contents of this presentation are not intended to provide investment advice and under no circumstances does anything contained in this presentation represent a recommendation to buy or sell any particular security or to invest in any particular product. Nothing set forth herein shall constitute an offer to sell any securities or constitute a solicitation of an offer to purchase any securities. Past performance is not indicative of future results. Investment returns will fluctuate over time and may be volatile.

The names “First Long Island”, “FLI”, and all derivations thereof are the property of their respective owners and may not be used or copied without prior authorization. You acquire no rights or licenses to download, upload, post, transmit, publish, or distribute this presentation or any other material in any way that infringes or otherwise contravenes the rights of FLI or any third party, including any copyright, trademark, patent, rights of privacy or publicity or any other proprietary right.

In no event shall FLI be liable to any party for any damages, costs, fees, expenses, or losses of any kind in connection with any use of the contents of this presentation even if advised of the possibility of such damages.

2023: Our Thoughtful View

“There are 60,000 economists in the U.S., many of them employed full-time trying to forecast recessions and interest rates, and if they could do it successfully twice in a row, they’d all be millionaires by now… But as far as I know, most of them are still gainfully employed, which ought to tell us something.” – Peter Lynch

“The true investor welcomes volatility… That’s true because a wildly fluctuating market means that irrationally low prices will periodically be attached to solid businesses.” – Warren Buffett

2023 and Beyond

Each year at this time while on my year-end holiday, I contemplate the year that just ended and give great thought to what lies ahead. It is easy to describe 2022 as ugly. Major indices sharply declined: the Dow Jones Industrial Average declined 8.8% and, for the more meaningful indices, the S&P 500 Index was down 18.1% and the growth-oriented NASDAQ Composite declined by 32.5%! For virtually all equities, this was the worst year since 2008, but it was preceded by several years of meaningful gains. All three of the above indices still made compounded gains for the three- and five-year periods ended December 31, 2022; however, 2022’s disappointment for all of us as traditional equity investors was palpable. (I should mention some hedge funds did fare better.)

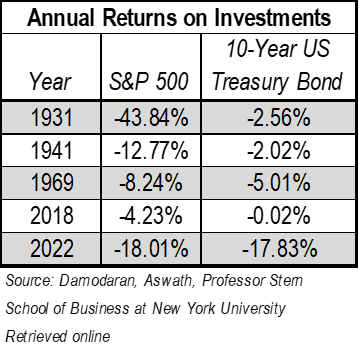

What made the year even more disappointing is that the normally safe haven of “risk-free” U.S. government bonds declined by 17.8% (as exemplified by the 10-year U.S. Treasury). In reviewing data going back to 1928, 2022 is the first and only time where both equity markets and U.S. Treasuries (as exemplified by the 10-year U.S. Treasury) were both down by double digits in the same year! This left virtually no place to hide except for cash, which had only a nominal return for much of the year. It is also too soon to tell how adversely affected both real estate and private equity will be by the conditions that caused such difficulty with publicly traded financial assets.

The rareness of the above was also accompanied by a crash in Bitcoin as well as the drying up of the hot SPAC market, both of which we have avoided. What was also so hurtful to consumers and businesses alike, however, was the increase in inflation, which reached a 40-year high. All of these troubling results caused a gloom among investors who attempted to make sense of the following:

1. The Fed raising rates at an unprecedented pace of 75 basis points for four consecutive meetings and most recently 50 basis points with more projected to come. In all there were seven rate increases in 2022!

2. A raging war in Ukraine resulting from an unprovoked invasion by Russia. The U.S. and other allies have contributed billions in defensive weaponry as well as humanitarian aid (and the vast majority of aid has come from the U.S.). Putin and his comrades have even threatened to use tactical nuclear weapons. (The potential for Russia to be a geopolitical hotspot was mentioned in last year’s thought piece, and this conflict was specifically referenced during our February 10, 2022 Market Update Webinar.)

3. The consensus of many economists that a recession will occur sometime in the next six to twenty-four months (see the first quote above). A leading sign of potential recession is the inversion of the yield curve where shorter-term interest rates are higher than longer-term interest rates. This is occurring now with the 3-month and 2-year U.S. Treasuries yielding more than the 10-year U.S. Treasury.

4. A newly divided government with a slim majority gained by Republicans in the House. The Republican agenda is intent on conducting political investigations as well as trying to bring an end to inflationary government spending and the immigration crisis on our southern border.

5. A housing market impacted by mortgage rates that have doubled over the past year, while sales of homes as well as rents are starting to drop in many areas.

6. Energy prices escalating where gasoline on average was 31% higher at year end. Food prices also rose 10% adding to consumer gloom.

7. The continuing impact of COVID-19 both here and abroad. China is experiencing new strains causing lock downs and economic turmoil.

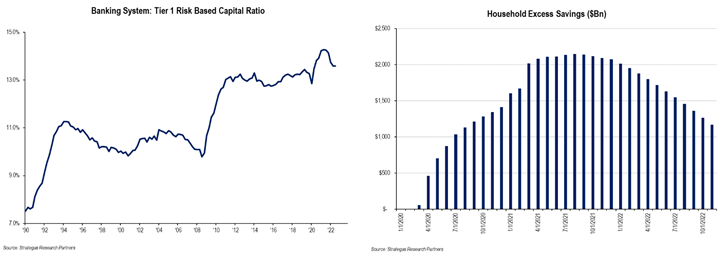

These troubling conditions impacting this past year contributed to declining price-earnings multiples, especially among growth stocks. Even dominant and financially strong companies including Microsoft, Apple, Alphabet, Meta Platforms, and Amazon.com (these may or may not be owned in various FLI strategies) did not escape the carnage, experiencing significant share price losses for the year. Not only are price-earnings multiples now pricing in higher interest rates, but, in our opinion, also the likelihood of an upcoming recession. However, the troubling factors listed above must also be balanced with our strong banking system, high level of employment, decent consumer confidence, and remaining excess savings held by many consumers:

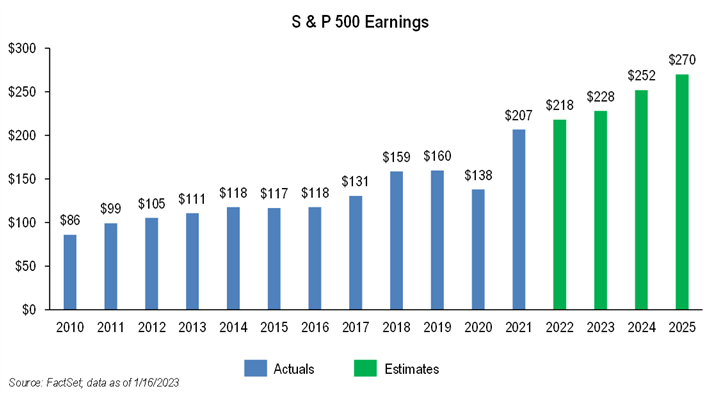

In addition, corporate earnings, aided by energy companies, rose for the S&P 500 Index in 2022 and are projected to increase modestly in 2023 based on consensus estimates. However, recent speculation suggests that earnings could decrease in 2023 if a recession should occur.

The strong earnings of recent years are facing headwinds from the rocket-like increase in interest rates (contributing to a stronger dollar, which hurts multinational companies’ earnings) as well as the Fed engaging in quantitative tightening (no longer buying U.S. Treasuries and allowing maturing bonds to roll off). Both are designed to slow the economy, increase unemployment, and reduce monetary growth, the latter of which we believe was the precursor to higher inflation. The following chart shows the upsurge in M2 growth, its recent collapse, and its average growth over many years.

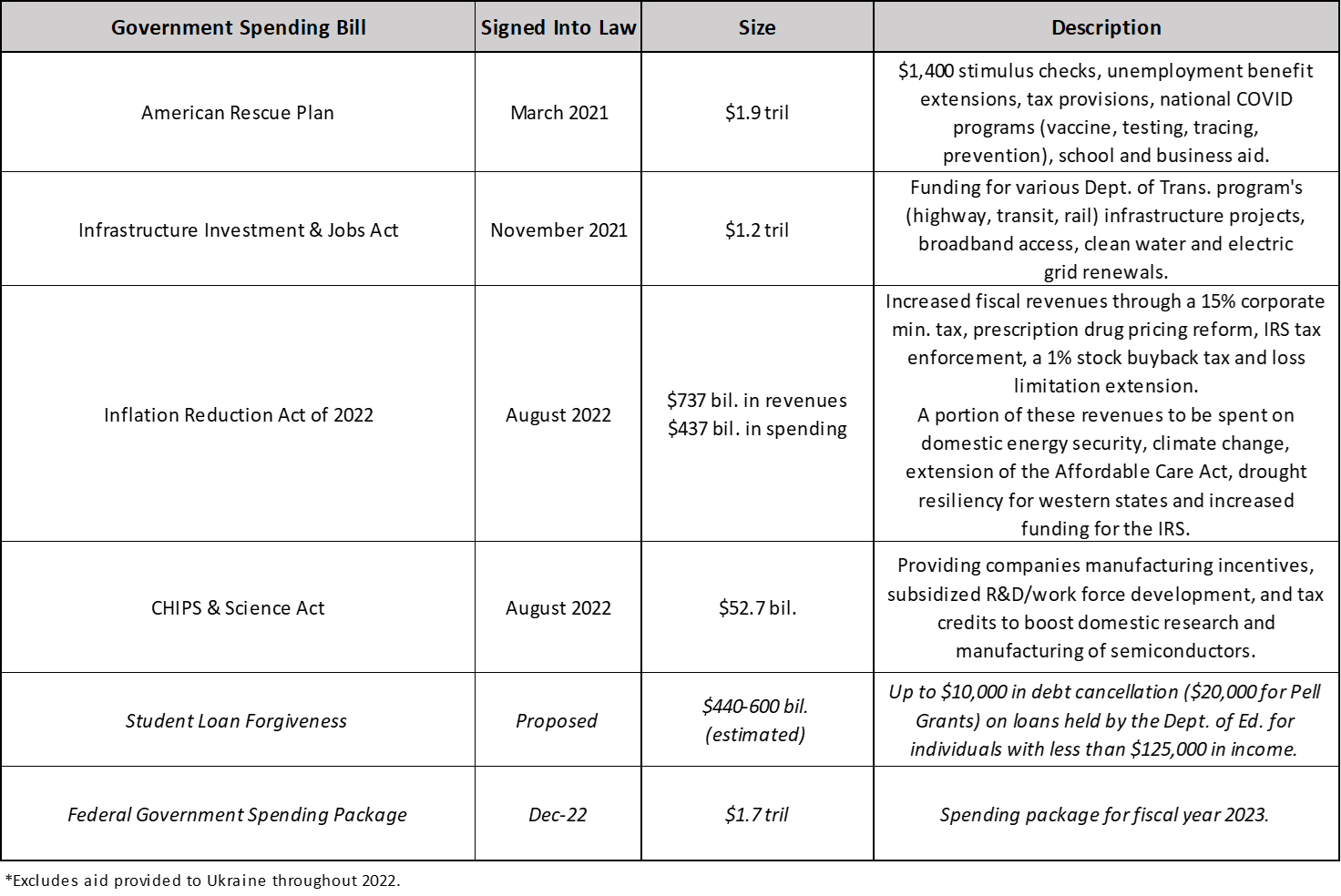

This dramatic growth in liquidity, which is inflationary by its nature (in our opinion), was caused by the monetary (the Fed) and fiscal (Congress) responses to the unprecedented COVID-19 pandemic. In addition, policy initiatives by the current administration, in our opinion, exacerbated the problem. It has been argued by economists on both sides of the aisle (notably Larry Summers who served in the Clinton and Obama administrations) that Congress went too far with excessive spending that went beyond the pandemic need for relief. We are still enduring additional recent spending bills. These bills are listed below to illuminate the sheer magnitude of the trillions in relief and other policy spending:

The COVID-19 Hangover and 2023

We strongly believe that the pandemic and its continuing impact have not only crippled investment performance in 2022, but will continue to be impactful in 2023. Call it a bad hangover as we battle persistent but weaker COVID-19 strains, conflicting government health advice, impact on our children’s learning and socialization, and continuing economic fallout (especially given the current unfolding situation in China). In 2019, the U.S. enjoyed a robust economy featuring above-average GDP growth, low inflation, and multi-decade low unemployment. The pandemic hit in early 2020 and global governments mandated shutdowns of numerous economies, which affected consumers and businesses alike. Many segments of the economy shut down and goods in many cases became hard to come by while e-commerce became an even larger portion of retail sales. Companies that benefit from people spending more time at home saw demand pulled forward and subsequently saw a significant, and in some cases unsustainable, improvement in financial results. Working from home transformed business practices. Consumers, both those who continued to work and those not able to work, some of whom received stimulus money from the government, accumulated savings as their spending patterns changed dramatically.

Excess savings are depicted in the chart above, but inflation near a 40-year high is eating away at it:

Now, from 2021 into 2022 and 2023 the barn door opened and the rush to spend on goods, travel, and other experiential desires are resulting in some shortages in availability, not just from supply disruptions and labor shortages but also from increased demand. We call this increased spending velocity. Insufficient supply of goods and labor to meet this demand leads to more inflation. As an example, the increase in the cost of jet and other fuels are just a part of the inflation problem as more people travel while also dealing with climate change that has led to record cold temperatures and storms in parts of the country. Meanwhile, the current administration’s bias against domestic fossil fuel exploration, coupled with other macroeconomic and political factors, has exacerbated energy shortages and elevated prices, while attempts to obtain additional foreign oil supplies have gone unrealized. This has forced our government to foolishly, in our opinion, deplete our strategic petroleum reserve. We believe this is a bad and dangerous policy given the global strife.

Investment Implications for 2023

This COVID-19 hangover coupled with the Fed playing catch-up (we believe it should have raised rates earlier) are a wicked combination. The Fed must bring down inflation (it is slowly beginning to happen) through rate increases resulting in higher interest rates than what we have been used to more recently, the latter of which Chairman Powell states will last longer than many had expected. At the same time, money supply, also known as M2, growth is abruptly decelerating and putting a strain on an economy that needs monetary growth, in our opinion, to grow at a reasonable rate. Right now, the Fed is dramatically reducing monetary growth in order to reduce inflation. In our opinion, it needs to constrain growth and subsequently force the increase of unemployment to stifle further wage inflation while also bringing down demand and overall inflation.

Short-term interest rates, as measured by the 3-month and 2-year U.S. Treasuries, are higher than the 10-year U.S. Treasury. This inversion has been a precursor to recessions in the past. The good news is that investors with dry powder or the cash buffer that we have urged for some time, can now achieve a pretax return of greater than 4% from U.S. Treasuries maturing in a year or two. The less than good news is that with the 10-year U.S. Treasury at 3.9%, mortgage rates have more than doubled from a year ago, putting pressure on housing prices and slowing demand for new homes. (Today’s 30-year fixed rate mortgage is still below the long-term average dating back to 1971.) This will, in our opinion, negatively impact the value of both residential and commercial real estate. Lending for real estate acquisitions or refinancings in our view will be more expensive; however, this increased cost of borrowing may present an opportunity for banks and some alternative investors (including certain FLI strategies), yet probably slow economic growth.

From an equity standpoint, last year demonstrated a big reversal where value stocks (still negative for the most part except for Energy and Utilities) vastly outperformed growth stocks that for several years prior had appreciated much more than value stocks. As a measure, since 2008, despite the terrible set back in 2022, growth stocks (the Russell 1000 Growth Index declined by 29.1%) have outpaced the Russell 1000 Value Index by a significant 274%. Companies like the growth darlings mentioned earlier suffered declines last year of anywhere from 25% to 65% despite being market dominant, financially strong, and profitable. More marginal (in some cases unprofitable) but hot growth stocks (i.e. Peloton Interactive and Beyond Meat) declined by upwards of 75%! Value oriented shares fared better and dividend growing stocks also performed relatively well, especially when compared to growth shares. Energy companies in general fared very well and as a sector were in positive territory (one of only two S&P 500 sectors to be in positive territory).

In our opinion, 2023 faces many of the same issues mentioned above that characterized 2022. Higher interest rates, high but slowly declining inflation, COVID-19 residuals, divided government, and worries about a recession that could reduce earnings for many companies all represent our wall of worry for 2023. And there is no end in sight to the war in Ukraine, which creates a level of fear for investors. I would also add that with the “death,” recently announced by President Biden, of a possible nuclear deal with Iran (in our opinion ill-conceived from the get go), the likelihood of an Israeli attack to attempt to eliminate a nuclear threat from Iran is a distinct possibility at some point. Newly elected Israeli Prime Minister Netanyahu has made it clear that in his opinion, a nuclear Iran is an existential threat to Israel and a threat to the “Great Satan,” the U.S. Also, we cannot ignore the growing hostility between the U.S. and China. Despite significant economic ties and dependence, relations between the two super-economies of the world are worrisome to say the least.

From an investment strategy standpoint, we believe significant tax loss selling was undertaken by many taxable investors over the last several months including in certain strategies we manage. This probably contributed to the lack of a Santa Claus rally typically seen at yearend. There may just be an opportunity now for some beaten down but financially strong and profitable companies, particularly in the growth space as our second quote suggests. These companies, some of which were mentioned earlier, in our opinion, can still grow their earnings this year even if the economy slows. Being able to defend margins (through possible cost cutting and layoffs) and grow profits in a slowing economy will stand out and could get rewarded! In addition, companies that consistently grew their dividends typically fared better than the overall equity market on a relative basis as they were somewhat insulated by higher yields and growing dividends. Our own Dividend Growth strategy saw the companies in the portfolio increase their dividends by an average of 11.8% in 2022 (well above the horrendous inflation rate of 8.0% last year). We believe dividend growth and an above-average yield will continue to be strong contributors to overall returns in the coming years. However, fair valuations based on earnings and interest rates must always be considered. We also do believe that some companies’ excessive share price drops may present an opportunity for the long-term investor!

The Bottom Line

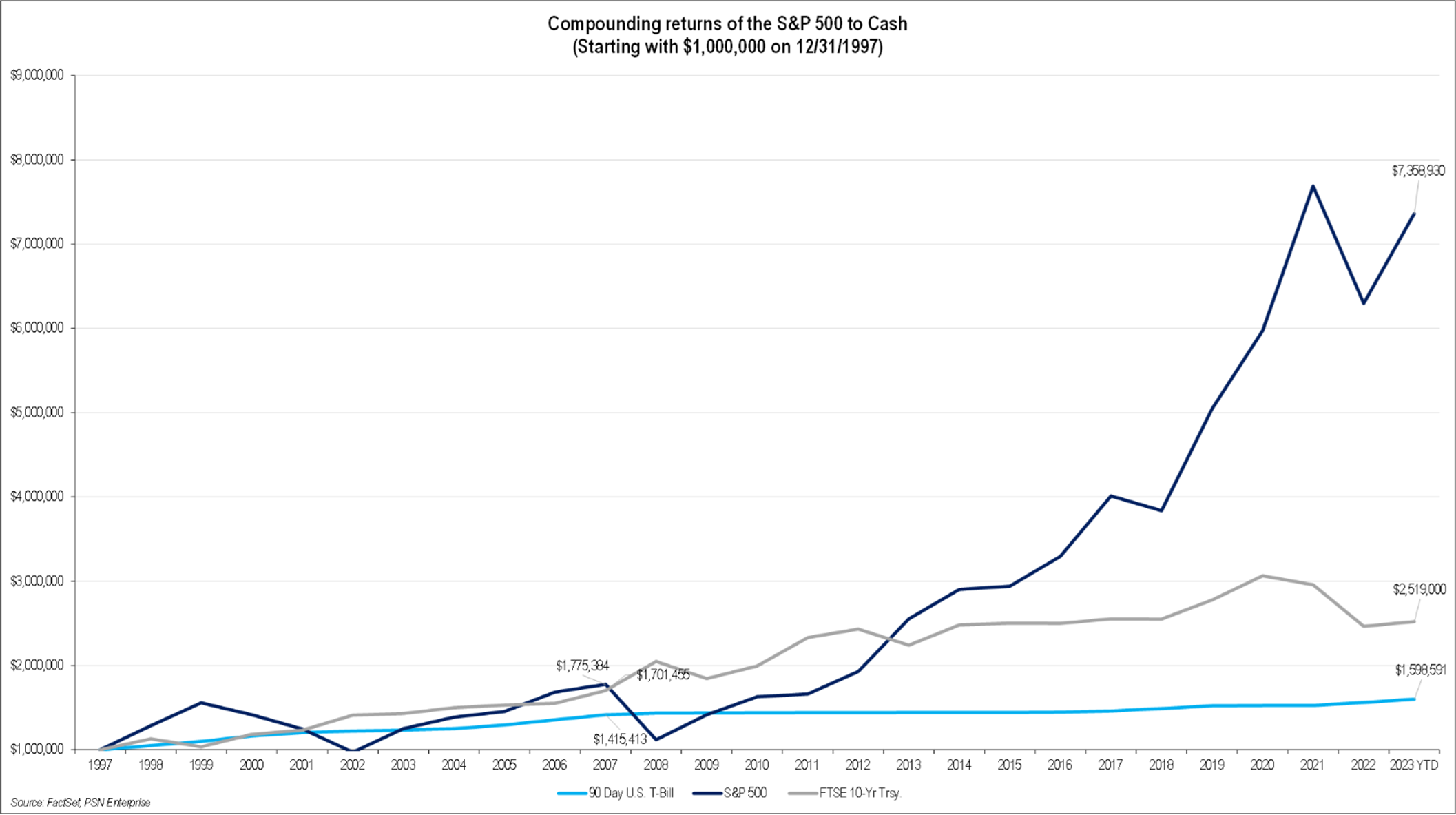

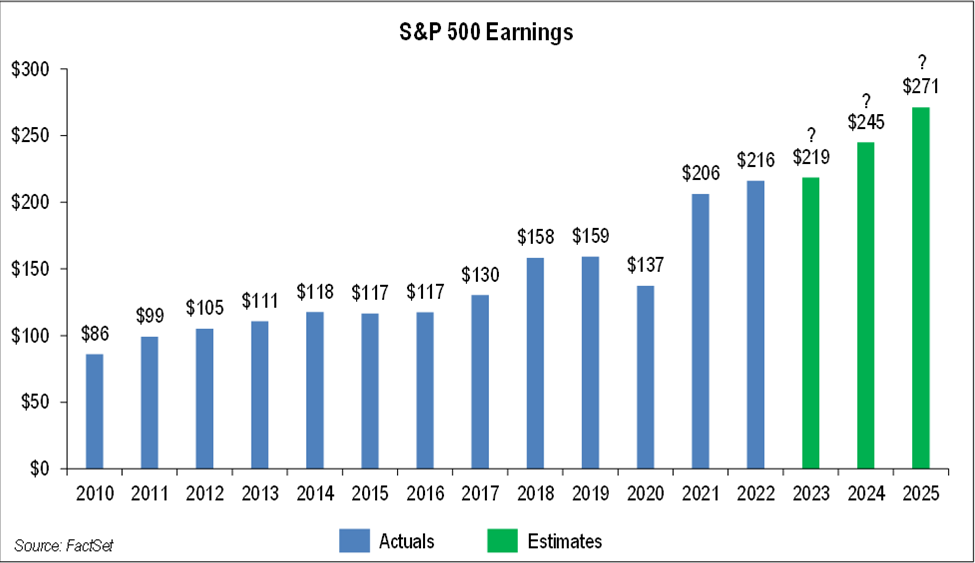

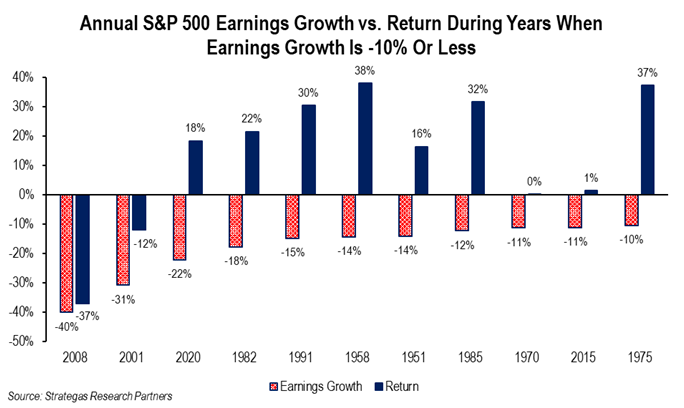

2022 was terrible. Both the Fed and Treasury Secretary mistook inflation to be transitory. The medicine to combat persistent inflation has been dramatically higher interest rates (a blast off) from the starting point of near zero. The fallout was collapsing price-earnings multiples especially for favored growth companies. Perhaps therein, selectively by individual company, lies the opportunity for longer-term investors. Higher-yielding dividend growers are the other side of this barbell approach to investing. Value-oriented companies, including dividend growers, coupled with fundamentally strong earnings growth companies make for a prudent, long-term asset allocation. Add to this mix a greater allocation to short- to medium-term U.S. Treasuries, municipal bonds, or high-grade corporate bonds as the absolute return on fixed-income investments is now more attractive than recently at least on a pre-inflation basis. We do, however, expect inflation to come down over the next year or so. At some point with a meaningful decline in inflation, the Fed will pause or even reverse course. We just do not know when. Interest rate increases take time to slow the economy and reduce inflation. If that were to happen (and we believe it will) both equities, especially profitable growth equities, and fixed income would respond in positive fashion, in our opinion. This can be the case even in the face of what we expect to be a mild recession in the next year or two. In the event of a recession and a reduction in S&P 500 earnings, share prices can still appreciate as evidenced in the chart below:

Make no mistake, we as investors are in a difficult environment both economically and geopolitically. As investors, we have been there before and will come out of this as we did after 2008, 2001-2002, 1973-1974, and many times before, but patience is required. A longer-term perspective is also needed and an adherence to owning high-quality, financially strong, cash flow generating, dividend growing, and market dominant companies in their space is a prescription, in our humble opinion, to get through this ugly period. That is a smarter approach rather than trying to discern the many different opinions from thousands of economists who are book smart, but typically do not invest anyone’s money. We do. Just as Buffett suggests, “wild” price fluctuations in strong businesses might just present the long-term investor with opportunities in select companies. We do not recommend index funds or industry ETFs at this point given the current difficult environment. We believe concentrated portfolios of quality, financially strong companies, or bonds, will provide positive results over time.

Additionally, this will serve as our Investment Perspective for our upcoming quarterly letter.

We at FLI hope your holiday season was pleasant and happy, despite an ugly year for us as investors. We wish you a healthy, happy, and more prosperous 2023. We remain committed to helping our clients navigate this difficult investment environment, and seeing over the valley to better times. Know that you can always contact any of us on our investment committee and/or our wealth management team.

Best Regards,

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

PS: Given the current environment and the aftermath of 2022, we deviate from the norm of one thought-provoking quote, and used two. We believe both are relevant today.

DISCLAIMER

The views expressed herein are those of Robert D. Rosenthal or First Long Island Investors, LLC (“FLI”), are for informational purposes, and are based on facts, assumptions, and understandings as of January 20, 2023 (the “Publication Date”). This information is subject to change at any time based on market and other conditions. This communication is not an offer to sell any securities or a solicitation of an offer to purchase or sell any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

This communication may not be reproduced, distributed, or transmitted, in whole or in part, by any means, without written permission from FLI.

All performance data presented throughout this communication is net of fees, expenses, and incentive allocations through or as of December 31, 2022, as the case may be, unless otherwise noted. Past performance of FLI and its affiliates, including any strategies or funds mentioned herein, is not indicative of future results. Any forecasts included in this communication are based on the reasonable beliefs of Mr. Rosenthal or FLI as of the Publication Date and are not a guarantee of future performance. This communication may contain forward-looking statements, including observations about markets and industry and regulatory trends. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect the views of the author as of the Publication Date with respect to possible future events. Actual results may differ materially.

FLI believes the information contained herein to be reliable as of the Publication Date but does not warrant its accuracy or completeness. This communication is subject to modification, change, or supplement without prior notice to you. Some of the data presented in and relied upon in this document are based upon data and information provided by unaffiliated third-parties and is subject to change without notice.

NO ASSURANCE CAN BE MADE THAT PROFITS WILL BE ACHIEVED OR THAT SUBSTANTIAL LOSSES WILL NOT BE INCURRED.

Copyright © 2023 by First Long Island Investors, LLC. All rights reserved.

On Thursday December 1, 2022 First Long Island Investors held an online web seminar with Dr. Bruce Farber, MD, where he presented the current state of infectious disease in the U.S. and globally (including COVID-19, the flu, and RSV).

Dr. Bruce Farber graduated from Northwestern University’s Honors Program in Medical Education with a B.S. and M.D. with distinction. He then did a three-year residency in Internal Medicine at the University of Virginia. After completion of that training, he spent a year doing a Fellowship in Hospital Infection Control at the University of Virginia, followed by a Clinical and Research Fellowship in Infectious Diseases at Massachusetts General Hospital and Harvard Medical School and the New England Deaconess Hospital. He served on the faculty of the University of Pittsburgh Medical School and joined the staff of North Shore University Hospital in Manhasset in 1986 and LIJ Medical Center in 1996. He is currently the Jane and Dayton Brown Professor of Medicine at Hofstra Northwell School of Medicine and Chief of Public Health and Epidemiology for Northwell Health. He has been the hospital epidemiologist at North Shore University and Chief of Infectious Disease at North Shore University Hospital and LIJ Medical Center. He is currently the Chief of Public Health and Epidemiology at Northwell Health. He has been a consultant to the NYS Department of Health, National Hockey League, Madison Square Garden, NY Islanders and numerous other companies and groups throughout the pandemic. He has authored over 50 peer reviewed papers, edited two books, and has written dozens of abstracts and reviews.

This presentation has been prepared for informational and educational purposes only and may contain observations about, among other things, public health conditions, public health statistics, medical therapies, financial markets, the economy, and various social, medical, financial, and other trends. The views expressed in this presentation reflect the opinions of the speakers appearing in the video in their individual capacities. While the speakers believe that the information contained in the presentation is accurate, neither they, nor First Long Island Investors, LLC (together with its owners, employees, and affiliates, “FLI”) are able to warrant as to its completeness or accuracy. The views and information expressed herein are not endorsed by and do not constitute the official position of FLI.

In addition, the information in the presentation is subject to change without notice. This presentation should only be considered current as of December 1, 2022 (or as otherwise indicated within the presentation) without regard to the date on which it was received or accessed. As a consequence, events may transpire subsequent to the date of this presentation that can render the contents incomplete, inaccurate or obsolete. There can be no guarantee that the information contained herein continues to be accurate or timely or that the speakers will continue to hold the views contained in the presentation. No party has any obligation to update the contents of this presentation. However, FLI maintains the right to delete or modify this presentation without prior notice.

The contents of this presentation are not intended to provide investment advice and under no circumstances does anything contained in this presentation represent a recommendation to buy or sell any particular security or to invest in any particular product. Nothing set forth herein shall constitute an offer to sell any securities or constitute a solicitation of an offer to purchase any securities.

The names “First Long Island”, “FLI”, and all derivations thereof are the property of their respective owners and may not be used or copied without prior authorization. You acquire no rights or licenses to download, upload, post, transmit, publish, or distribute this presentation or any other material in any way that infringes or otherwise contravenes the rights of FLI or any third party, including any copyright, trademark, patent, rights of privacy or publicity or any other proprietary right.

In no event shall FLI be liable to any party for any damages, costs, fees, expenses, or losses of any kind in connection with any use of the contents of this presentation even if advised of the possibility of such damages.