JERICHO, NY – September 25, 2013 – First Long Island Investors (FLI), one of the first independent, employee-owned wealth management firms on Long Island, is celebrating its 30th anniversary in October. The firm has a venerable history since its beginnings in 1983 when FLI Chairman, CEO and Chief Investment Officer Robert D. Rosenthal and President and Chief Operating Officer Ralph F. Palleschi transitioned from their executive positions at Entenmann’s, then a division of General Foods, while retaining the Entenmann families as their first clients.

“By three methods we may learn wisdom:

First, by reflection, which is noblest;

Second, by imitation, which is easiest;

and third by experience, which is the bitterest.”

Confucius

Summary Review

The second quarter was a modestly positive experience for several asset classes led by equities. This is a continuation of a very strong first quarter where equities surprised most on the upside. On the other hand, bond yields increased, resulting in price declines and paper losses for many investors who were exposed to interest rate risk by extending out maturities to try to achieve modestly higher yields. There is probably more of that coming as the economy makes some progress and the Fed makes the smart but tough decision to somewhat taper bond purchases (this might well be perceived negatively in the short term but we believe is quite positive in the long run). Residential real estate also continued its rebound reflecting somewhat better employment as well as wealth gains in the stock market which have fueled consumer confidence.

Our strategies at First Long Island continued to make progress and most added to the large gains achieved in the first quarter (led by W.P. Stewart, Dividend Growth, FLI Select Equity, Value and Growth Funds). The strategy that did not appreciate was essentially flat (FLI Partners Fund) for the quarter, holding onto its significant gains recognized earlier in the year. Our bond portfolios were slightly down as we have kept maturities on the shorter side having been worried about the potential for rising rates. So, all in all, our second quarter was quite good.

Now we believe it is time for some reflection on investment wisdom and that is the reason for the above quote. We all know that our world has become more complex as the investment landscape has become truly global and, the “wall of worry” that we must reckon with extends beyond our borders. We think about geopolitical events in Syria, Egypt, North Korea, Iran and elsewhere. Economic issues in the Eurozone and emerging countries (e.g., China) as well as the pace of growth in the U.S. require intense consideration. The impact of policy changes (Affordable Care Act) as well as potential policy changes (tax reform and immigration) must also be put in the mix. And of course, finally, how does all of that affect the businesses, real estate, and bonds we invest in as well as their worth?

As Confucius has suggested, if we reflect, consider the thoughts of smart people we have access to, and then tap into our experiences of thirty years in this business, we should be able to derive a sound strategy for our clients. Our investment committee meets weekly (as do our strategy- specific subcommittees) and we counsel with several investors and strategists that we believe are smarter than we are (great investors like Bill Stewart and Bruce Berkowitz to name two, and strategists including Jason Trennert at Strategas Research Partners, LLC and Robert F. DeLucia, CFA, Consulting Economist for Prudential Retirement). We continue to think about the businesses we invest in, the conditions they face globally, the healing of our banking system, our politicians in Washington, stubborn unemployment, and consumers who make up 70% of our economy. We also think a lot about the future and see greater energy independence for America. We struggle with, but try to gain a perspective on, a world gripped by terrorism as well as the public defiance by people who are repressed in countries like Syria and Egypt. We remain strongly committed to domestic-equity investing while we continue to worry about the lack of real rates of return on bonds and cash. We believe that inflation will be tame; interest rates will slowly rise but remain “repressed” for the next few years; real estate will continue to appreciate although higher mortgage rates (albeit historically very low) could temper that somewhat; and other private investments (private equity) will also trend higher, following equity markets. Of course, unemployment and significant part-time employment (the U6 rate of 14.3% combining both) will likely remain stubbornly high as our country digests the impact of the new Affordable Care Act as well as uncertainty in policy from Washington. These will tend to moderate the potential growth we could achieve.

Where does all of this leave us after reflection, counseling with others and adopting many of their conclusions, and drawing upon our collective experiences being in this business for more than thirty years? First, keep to a prudent and diversified asset allocation that continues to give you exposure to asset classes that work over the long term. We continue to overweight both defensive and traditional equities; we are underweighting bonds and keeping maturities on the shorter side; and we believe that private investments (private equity, special situations, and real assets) are worth pursuing for patient investors who can tolerate illiquidity. (This is evidenced by our most recent creation of our partnership investing with Bruce Berkowitz’s Fairholme Investment Management for suitable investors.) Alternative investments, including many long/short hedge funds, on average have underperformed our traditional and defensive equities the last several years. We believe that will continue as volatility remains low and only seems, for now, to spike for short periods of time. So why do we remain so constructive on long-term defensive and traditional equities?

Over the past several years (see our past quarterly letters) we have urged our clients to commit to the equity markets. This reflected our contrarian view versus many equity market naysayers. This under-loved asset class has had significant outflows versus bonds; corporate balance sheets are strong; dividends are higher; global growth continues albeit at a slower rate; valuations to us have been and remain attractive as corporate earnings continue to grow; and individuals, institutions and corporations have mountains of cash on the sidelines. Contrast this with the most obvious alternative for all investors, bonds. Bond yields are terribly low and starting what we predict will be a slow rise. Not a good prescription for bond investors. So, where do we stand today?

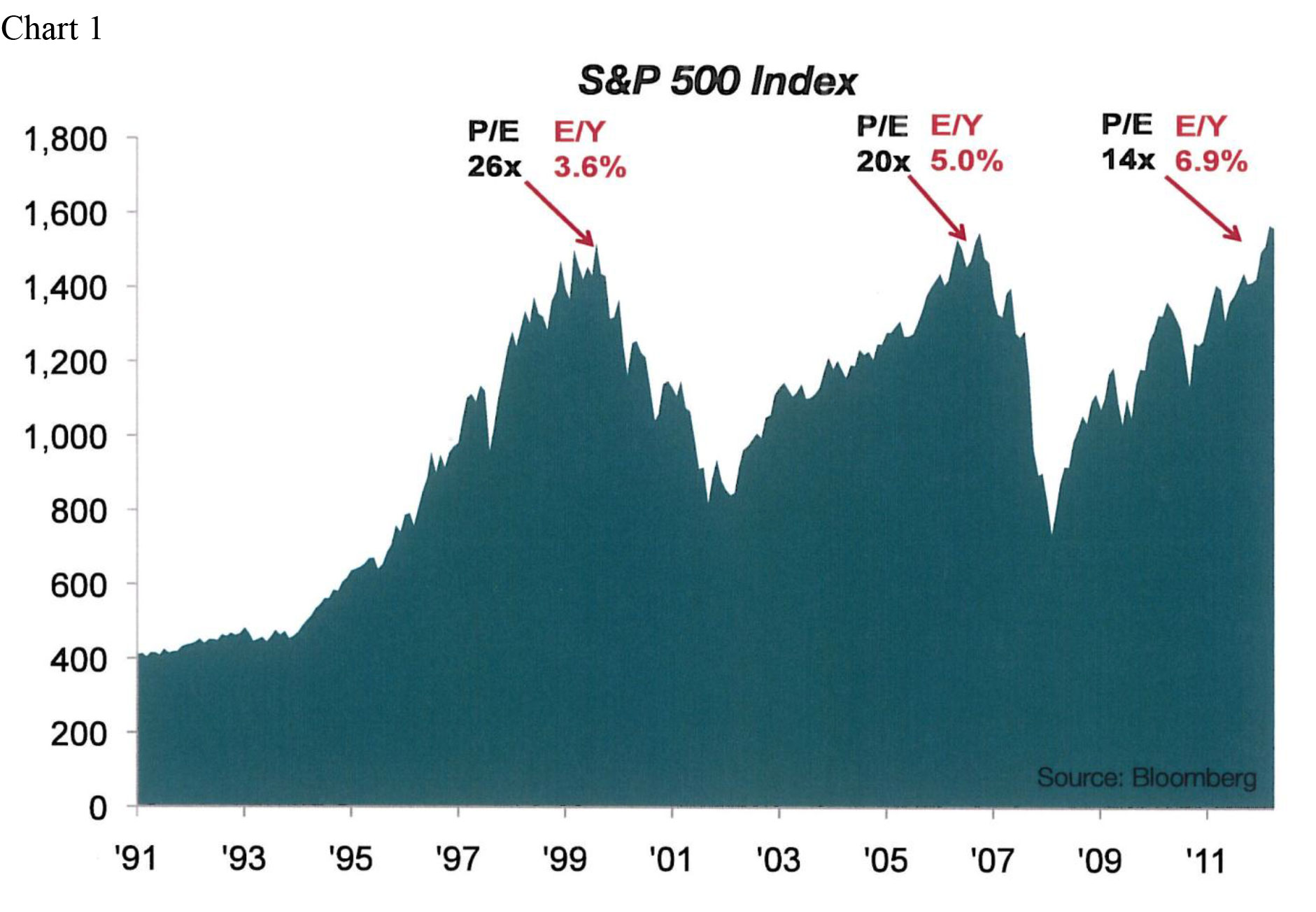

We believe that the average large-cap stock is somewhat undervalued despite the S&P 500 near a record high. The chart (Chart 1) below shows that despite the S&P 500 being slightly above the prior record highs recorded in 2000 and 2007, earnings are much higher, p/e’s are therefore much lower, and the highest quality investment alternative, the 10-year U.S. Treasury has a much lower yield.

In our view, unless earnings were to drop due to a recession, large-cap stocks are relatively cheap! Even if we were to normalize the 10-year U.S Treasury to a 4% rate (up from the current 2.5%) we believe the S&P 500 level today would still be attractive. Additionally, we do not see a recession on the horizon. We believe our economy is still growing between 2% and 3% per year; employment is getting somewhat better; and global growth from emerging economies is still more than offsetting weakness in Europe and Japan. Add to this the pain that bond investors are now feeling from paper losses and perhaps this next chart will change direction:

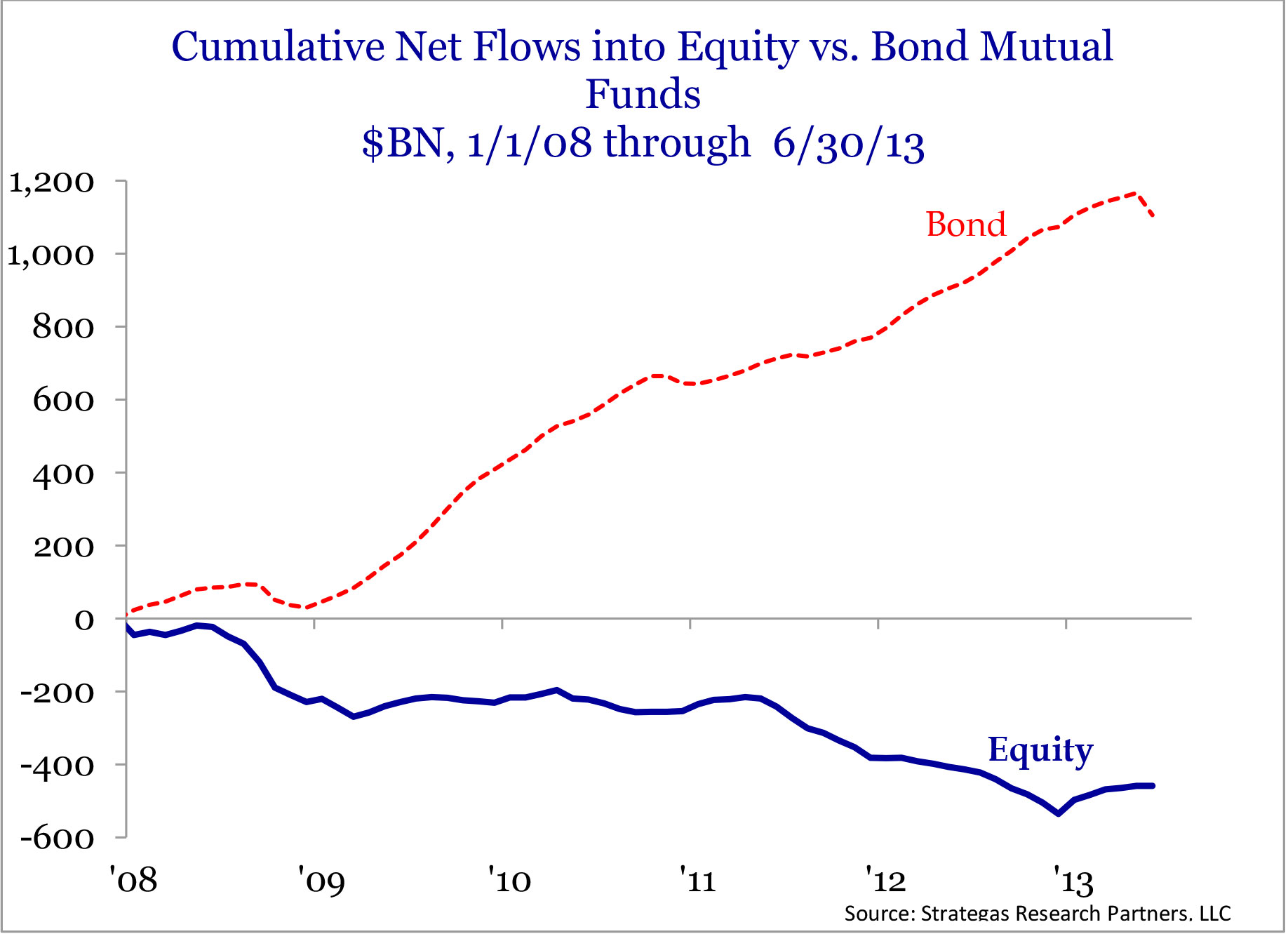

Chart 2

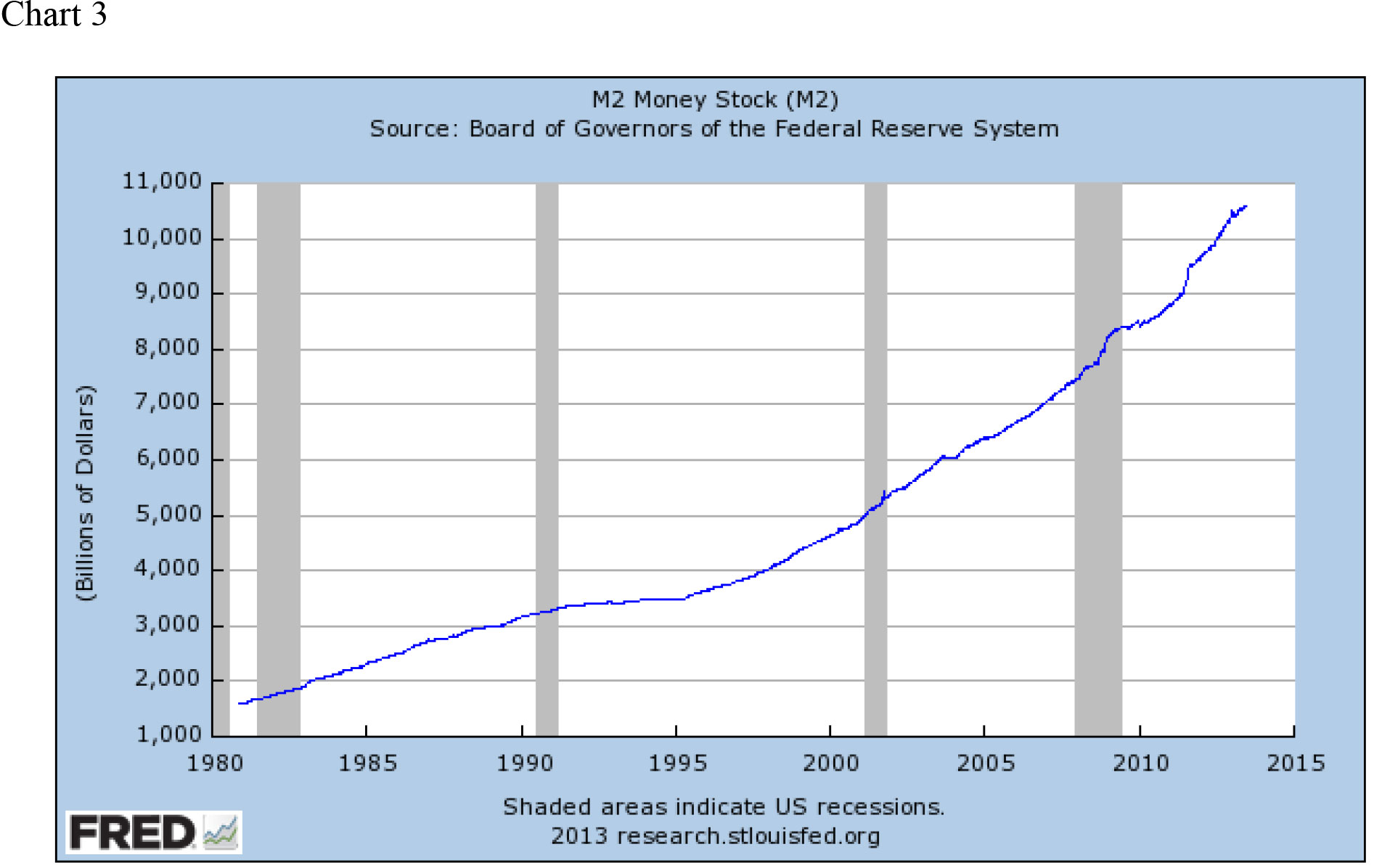

This chart (Chart 2) shows that despite the run up in stocks (following earnings growth) there has been an outflow from stock funds into bond funds. This herd mentality has the average investor chasing a bond market that is now in retreat. If some of the money in the following chart (Chart 3) plus some disillusioned bond investors were to move funds into equities, the appreciation in equities could continue for the foreseeable future in part from this increased demand. Of course, we don’t have a crystal ball, so we continue to preach asset allocation and diversification. We do not believe that the S&P 500 is overvalued when you consider that it is trading at what we believe to be a reasonable 14 times next year’s earnings. (By the way, there is a theory called the Rule of 20 that suggests a reasonable p/e is 20 minus the level of inflation. This would put us at a 17 to 18 multiple while we believe the market is at 14 times next year’s earnings.) While not all gurus believe p/e’s are as reasonable as we do, we are sticking to our belief.

Summary

We had a reasonable second quarter following a great first quarter. Many investors are worried that stock market advances cannot continue while they witness paper losses in their bond portfolios. We believe that prudent investors are starting to recognize that you can be a long-term investor in the equity markets as part of one’s overall asset allocation. Some have taken their profits only to watch the markets keep rising. Others are paralyzed in cash and over-allocations to bonds wondering if it is too late to add to or initiate equity investments. We continue to believe that there is more to come and the greed factor that typically takes equity markets to new heights is not even a factor yet. (Has your taxi-cab driver given you a stock tip lately?) Bond portfolios could be facing more losses on paper and stashing away cash, earning less than the rate of inflation, will only serve to deplete one’s purchasing power over time. (We are not suggesting eliminating one’s bond portfolio or having no cash cushion. We are just stating that these allocations should be underweighted or one must accept less potential appreciation and potential paper losses as well as a loss of purchasing power.)

Confucius speaks of reflection, imitation of smarter people, and use of experience in crafting a direction. We continue to do that for you from an investment standpoint. If one looks back at our quarterly letters for the past several years, you will see that our direction, so far, has been on the money (no pun intended). However, modesty gets us back to where we always preach diversification in one’s asset allocation to prepare for the unknown. We conclude with our quote from our last letter:

“Your ultimate success or failure will depend on your ability to ignore the worries of the world long enough to allow your investments to succeed.” Peter Lynch

Believe in America’s future as a global leader and, when properly advised, let your asset allocation work for you over the long term.

Have a great summer, and please call with any questions, comments or concerns.

Best regards,

Robert D. Rosenthal

Chairman and

Chief Executive Officer

Ralph F. Palleschi

President and

Chief Operating Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results.

Disclaimer: The views expressed are the views of Robert D. Rosenthal and Ralph F. Palleschi through the period ending June 30, 2013, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Content may not be reproduced, distributed or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC . Copyright © 2013 by First Long Island Investors, LLC. All rights reserved.

Michael Dowling, North Shore-LIJ Health System’s President and CEO, discussed with clients, colleagues and friends of First Long Island Investors the current state of healthcare in the United States, the ramifications of the Affordable Healthcare Act (what some call Obamacare) and the future of healthcare for hospitals, service providers and patients.

Robert D. Rosenthal, Chairman & CEO of First Long Island Investors LLC (left), and Michael J. Dowling,

President and CEO of the North Shore-LIJ Health System (right).

Here are some of the highlights from the discussion:

Hospitals are Big Business and an essential component of the health delivery system

- People don’t like to think of them as such, but they are

- North Shore-LIJ employs over 47,000 people, making it the largest employer on Long Island, and it faces the same challenges as other employers

- Quality care and a high level of service are important, and patients want the best value for their dollar

Healthcare Today

- Changes in lifestyle is one of the reasons that has led to poorer health in the US

- Obesity rates, particularly among children and teens have risen significantly

- We are doing a better job of keeping people alive longer

- We have added 35 years to life in the last 100 years, and have gotten so good at extending life that taking care of the elderly has added to high costs

- The government doesn’t focus primarily on the total costs of healthcare, just the cost to the government

- More than 60% of hospital reimbursements come from the government (Fed & State)

- We are using a fee for service payment model which causes interests to be misaligned

- It is to the hospital’s advantage to have beds full, so they are not compensated for providing well-care, and may do things they would not do with a different reimbursement structure

- Some estimates suggest that 20% of the patients in hospitals shouldn’t be there

- More procedures should be done outside of hospitals

- The terminally ill should if possible be dying in their homes, not in hospitals

The Affordable Care Act

- The Affordable Care Act (also known as Obamacare) is a maze of confusion, not completely understood by many and the White House has already begun to make adjustments

- Not everyone is covered under the Affordable Care Act and the plan doesn’t lower costs (no proof yet that it will)

- The politicians who wrote the bill have limited knowledge about the healthcare business – especially what it takes to implement at the ground level

North Shore- LIJ

- The country needs more quality, well-rounded doctors

- Opened a new medical school with Hofstra, which threw out the traditional method of medical education and focuses on training doctors in a different way

- Involved in more research

- Would be surprised if a North Shore-LIJ employee doesn’t win a Nobel prize soon

- Building more ambulatory centers, 400 and growing

- Working with CVS to operate in-store clinics manned by nurse practitioners

- Will lower emergency room visits

- Partnering with the Cleveland Clinic and Mayo Clinic to become more innovative

- Want to be like Starbucks, be in the community and deliver a quality product

The Future of Healthcare

- The business model of healthcare should change

- Want to be paid not just for services but for keeping the population healthy and out of the doctor’s office and hospital as well

- North Shore-LIJ is spending time and money on population well-care

- North Shore-LIJ is building its own health insurance company, and is working in conjunction with other insurance companies, to hopefully obtain an insurance license by the end of the year

- Incentives for hospitals will be turned around, and hospitals will want to keep you out of the hospital to reduce total health care costs

- Medical tests, which are overused in the US, will be reduced

- There will be fewer independent practices, as more doctors will be employed by hospitals

- Nurses and nurse practitioners will become more important and take on more roles of the primary care physician

- Prices for treatments will become more transparent and a larger proportion of the cost of treatment will fall to the patient, perhaps leading to a change in their lifestyle

- “Healthcare is what we do to ourselves, and unless we think of it that way we are not addressing the problem”

Michael J. Dowling

Michael J. Dowling

Mr. Dowling is president and chief executive officer of the North Shore-LIJ Health System, which delivers world-class clinical care throughout the New York Metropolitan area, pioneering research at The Feinstein Institute for Medical Research and a visionary approach to medical education, highlighted by the Hofstra North Shore-LIJ School of Medicine. North Shore-LIJ operates 16 hospitals and nearly 400 outpatient physician practices and is the nation’s third-largest non-profit secular health system. Mr. Dowling has been recently recognized as one of the 100 most powerful people in healthcare by Modern Healthcare magazine. Prior to joining North Shore-LIJ in 1995, Mr. Dowling served in New York State government, as director of Health, Education and Human Services, and as deputy secretary to the governor.

JERICHO, NY – First Long Island Investors, LLC (FLI), a wealth management firm based in Jericho, announced today that its Dividend Growth Strategy has been ranked in the top one percent of large-cap U.S. equity managers by PSN Enterprise, a division of Informa Investment Solutions, for both the three-year and two-year periods, ended March 31, 2013. Informa Investment Solutions compiles investment returns and ranks more than 3,500 money managers. FLI Dividend Growth’s performance since inception on March 31, 2010 is up a cumulative 53% and has outpaced the S&P 500 Index by 10%.

“Your ultimate success or failure will depend on your ability to ignore the worries of the world long enough to allow your investments to succeed.” Peter Lynch

Summary Review

The first quarter resulted in very substantial gains for domestic equity markets (S&P 500 +11%), treading water in bonds, and a slow but continuing recovery in real estate. This is on top of last year’s significant appreciation in equities. Meanwhile, yields on bonds remain low as the Fed continues to buy bonds, unemployment remains stubbornly high and inflation remains low. Investors who have not participated in the record-setting domestic-equity market feel left out and somewhat trapped in their low-yielding bond investments and cash. Prudent asset allocation continues to be the answer for all investors enabling participation in the equity markets while being diversified. Meanwhile, we are pleased to report that we believe all of our clients have appropriate allocations to both defensive and traditional equity holdings and have participated in the escalating equity markets. In particular, our Dividend Growth strategy, one of our defensive equity strategies, led the pack for us in the first quarter appreciating by 14%. (For the three years since inception this strategy has appreciated by 53.3% and has outpaced the S&P 500 which appreciated by 43.1% while still being a defensive equity strategy, in our opinion.)

We believe those investors who have been too skeptical about “stocks” now seem to be finding a way to invest, in part, through buying companies that we own in our Dividend Growth strategy. These stodgy, larger, financially-strong companies that pay generous and growing dividends continue to attract investor interest. However, we believe, based on academic support, that the appreciation for these companies will result from the combination of their higher yields and dividend growth. We also believe that the current market appreciation is not overdone and equities remain a reasonable place to invest as compared to bonds that offer little yield and risk paper-losses if interest rates increase. Corporate earnings continue to grow modestly and price-earnings ratios for large companies (about 15 to 16 on forward twelve month earnings) remain well below that seen in either of the last two market tops in 2000 and 2007 when p/e’s were 26 and 20 respectively. Add to that the fact that bond yields were much higher then and thus more attractive versus the financially-repressed low rates of today. In our view, that combination of reasonable p/e’s and unattractive interest rates continue to make for an investor-friendly equityenvironment. This is further bolstered by the fact that money on the sidelines (both individual, institutional and corporate) is at very high levels and some of it appears to be migrating to quality equities.

Having said that, one needs to focus on our quote from Peter Lynch. What stops investors from achieving attractive long-term gains on investments is their understandable distracting focus on the worries of the world. Certainly there are many to be concerned with, including:

- Geopolitical issues resulting in dreadful headlines about both North Korea and the Middle East.

- Worries about U.S. debt and the viability of entitlement programs such as Social Security, Medicare, and Obamacare.

- The continued haggling in Washington over so many unresolved social (gun control, immigration, and same-sex marriage) and economic issues.

- Our inability to meaningfully bring down unemployment and spur better than weak economic growth.

Meanwhile, American business remains financially healthy and is fostering slow but profitable growth in part through efficiency and global demand. And, for the most part, businesses are sitting on a stockpile of cash giving us comfort that they are stable and can weather unforeseen crises that come on unexpectedly, and typically don’t last too long. Even our large banks seem to be healing and are subject to new regulations that may somewhat protect us in the future.

So it remains our view that there are opportunities to make reasonable returns over the long term from a prudent and diversified asset allocation among our investment baskets of security, defensive equities, traditional equities and private investments. A customized asset allocation among these baskets hopefully permits you to “ignore” the worries and let your investments work for you over the long term. And even though there will definitely be periods of volatility and market corrections, we can see from past history that those who stay the course for the long term are ultimately rewarded with meaningful appreciation. The key is in the asset allocation that provides the strength to weather the worries of the world. Having exposure to bonds, defensive equity strategies (Dividend Growth and FLI Partners Fund), traditional equities and private investments (private equity and real assets) with a quality and concentrated bias is a prudent formula for all of our clients. Patience remains a critical characteristic of the successful investor.

Please call upon us if we can be of further assistance in making sure you have an asset allocation that gives you the ability to ignore some of the worries and let your money compound for you.

Best regards,

Robert D. Rosenthal

Chairman and

Chief Executive Officer

Ralph F. Palleschi

President and

Chief Operating Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results.

Disclaimer: The views expressed are the views of Robert D. Rosenthal and Ralph F. Palleschi through the period ending March 31, 2013, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Content may not be reproduced, distributed or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC . Copyright © 2013 by First Long Island Investors, LLC. All rights reserved.