On January 30, 2014, First Long Island Investors (FLI) Senior Vice President Edward Palleschi was presented with the Long Island Business News 40 Under 40 Award for his dedication and commitment to both his profession and community. The ceremony was held at the Crest Hollow Country Club, where Mr. Palleschi was joined by 39 other honorees from various industries who also received this honor.

“The underlying principles of sound investment should not alter from decade todecade, but the application of these principles must be adapted to significant changes in the financial mechanisms and climate.”

Benjamin Graham (father of modern security analysis)

First, 2013 was a surprisingly good year. In our thought piece for 2013, we suggested that domestic equity markets would be robust, however, even we were pleasantly surprised. Our asset allocation of overweighting defensive and traditional equity strategies paid off handsomely.

Several of our strategies exceeded their benchmarks, as well as delivered substantial absolute returns. Our concern about fixed income also came true, with very modest losses suffered by most who followed our advice while those who stretched out maturities to achieve somewhat higher income suffered larger losses. Also, we believed that housing would recover and that was the case. Private equity also saw solid returns as the initial public offering market came to life and there was an increase in debt deals and merger activity. Thus, the net result for 2013 was quite positive for our clients who followed our direction and sought a return on capital, as opposed to those still paralyzed from 2008 and early 2009 seeking just a return of capital. Those investors who over allocated to cash and fixed income continued to be victims of their own fear and the financial repression currently thrust upon us by our Federal Reserve Bank and central bankers around the world.

The essence of the quote from renowned investor Ben Graham is that the basic principles of sound investing by owning quality companies with earnings and cash flow growth, dividend streams, and reasonable valuations continues to make sense. We have routinely put this to work, doing so in 2013, and will continue to do so in 2014. We adjust our asset allocation recommendations for the prevailing financial environment and current economic climate.

Unprecedented (but necessary) monetary stimuli, financial repression with zero short-term interest rates, political paralysis, foreign economic uncertainty, and untested new financial regulations all contributed to our shift to underweighting fixed income and overweighting domestic defensive equities. This worked out quite well in 2013 and we believe it will continue to do so in 2014.

It is worth noting that the robust wealth creation of 2013 from the stock market and housing occurred despite the following:

- A government shut down

- Political paralysis

- Disruption from the onset of the Affordable Care Act

- The first tapering of Quantitative Easing

At the same time, the following worries seem to have faded (at least for now): - European fiscal and monetary crisis

- Iranian nuclear development

- Record U.S. national debt exceeding 17 trillion dollars

- Continuing domestic bank legal settlements for the misdeeds of the subprime and other crises

And the following factors contributed to some optimism:

- Domestic banks’ balance sheets are strong and getting stronger

- Corporate America achieved record earnings with abundant cash on their balance sheets

- Inflation remains stubbornly low despite accommodative fed monetary policy

- Consumers have delevered and are beginning to spend

- Housing is on an upswing

- America has become a major producer of energy and is heading towards energy

independence.

So, what do we, as investors, look forward to in 2014?

We believe that the following trends and factors will drive results for this year:

1. Short-term interest rates will remain low while longer-term rates will trend somewhat higher but remain well below historical levels. Fed tapering will be tolerated as long as the resulting somewhat higher rates do not impede economic progress. This doesn’t bode well for longer-duration fixed-income investments.

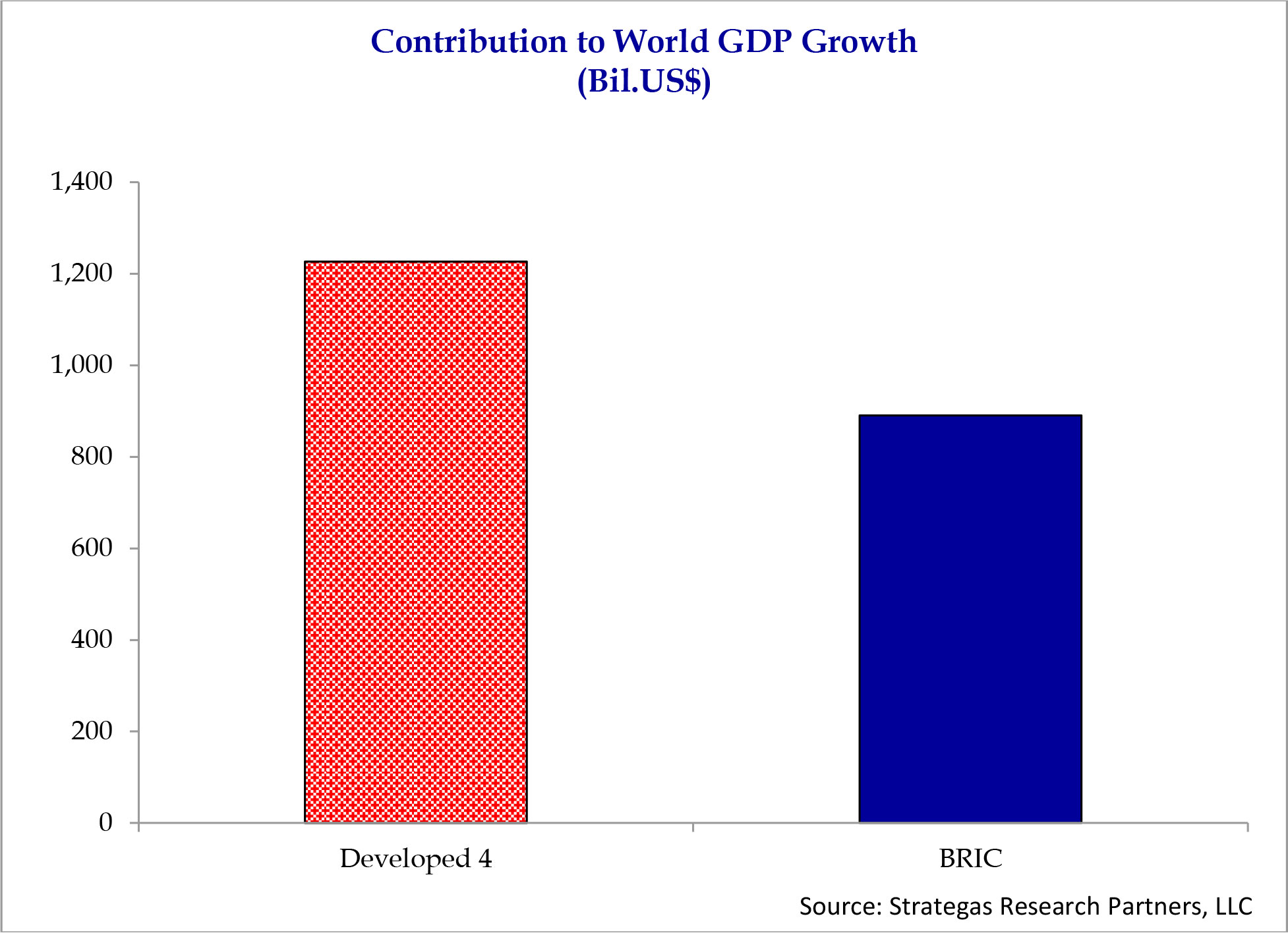

2. Corporate earnings will continue to grind higher supported by modest global economic growth. The U.S. should have real economic growth in the 2.5% to 3.5% range. Europe should achieve some economic growth after having recently emerged from recession (although some banking issues relating to loans are still a concern). Japan is working to inflate its way out of deflation. Finally, developing markets, led by China, will continue to grow at a somewhat slower rate than past years (while trying to control reckless borrowing). The importance of these growth estimates is depicted in the following chart, which shows that the biggest contributor to global growth will come from four of the largest developed countries (U.S., Japan, Britain, Germany), not the BRIC countries (Brazil, Russia, India, China):

This is important as we will continue to overweight domestic equities which we believe still represent the most consistent growth and have reasonable valuations.

3. As mentioned above, the increased domestic production of oil and gas using fracking and other high-tech methods of extraction will bring jobs and lower energy costs to our country. (Mexico is also promoting outside investment in the development of its offshore oil.) This has other benefits including reducing the cost of manufacturing, which we believe will boost domestic manufacturing and bring back some higher-paying jobs. Of course, environmental concerns will have to be considered and, given the increased

regulations coming out of Washington, we do not have to worry.

4. U.S. unemployment will continue to decline. However, the nature of the jobs being

created is in many cases part-time or lower-paying jobs. This will need to be addressed by fiscal policy initiatives coming out of Washington. We believe that increasing the minimum wage is a Band-Aid and not the answer. A bipartisan approach to some tax

Developed 4 BRIC

Contribution to World GDP Growth

(Bil.US$)

Source: Strategas Research Partners, LLC

4. reform and a pro-growth legislative agenda is the answer. We believe this will happen in small steps.

5. Mid-term elections will cause some religion in Washington. Both parties have much to gain or lose. The bipartisan budget deal (modest in size) accomplished by Congressman Ryan and Senator Murray will be a pattern for the future. Do not be shocked to see some improvement through small deals on immigration and tax reform. Extremists in both

parties are not going to have their way and cooler heads will prevail as 2014 is an

important election year. This bipartisan cooperation could be quite positive for the stock

market when coupled with the modest earnings growth we expect.

6. State and municipal spending will actually trend up in some states. This is in contrast to the austerity at state and local governments that we have seen since the “decession.” Also, the reduction in sequestration at the Federal level will help the domestic economy grow.

This increase in spending could be another positive for both the economy and the equity markets. On the “wall of worry” side, we have the following which we believe will cause some volatility for sure:

1. The full implementation of the Affordable Care Act is apt to cause disruption and higher costs as it expands coverage. The shaky start technologically will be followed by more disenfranchised Americans. High deductibles, loss of choice regarding doctors and hospitals, and doctors opting out of serving many due to cuts in pay, and other factors will counterbalance some of the positive elements of the law. In addition, because many states did not expand their Medicaid offerings, millions of Americans will still not be covered by the new law. It is estimated in the Economist that 40,000,000 Americans will still not be covered while only 11,000,000 will gain insurance coverage in 2014.

2. The mid-term elections will bring to the surface many long-term systemic issues that have faded, including the impending financial crises surrounding Social Security, Medicare, and the U.S.’s huge fiscal deficit. In particular, the future funding of Medicare is a big issue that must be addressed, especially as it is now being strained by the Affordable Care Act. Republicans need only six Senate seats to regain a majority. Of note, six Democratic Senators up for reelection are from states where a majority voted for Governor Romney in 2012. These, and other seats in Congress, will be bitterly contested. As a result of this, neither party will want to be viewed as obstructionist, thus fostering some level of bipartisanship on immigration, tax reform and infrastructure spending.

3. The U.S., Israel, and other nations will continue to deal with Iran and its nuclear ambition. The recent temporary agreement entered into by the U.S. and Iran expires in a matter of months. Critics are skeptical that anything of substance will be accomplished. This is worrisome to say the least and could lead to a military confrontation. This is especially worrisome as Syria, Lebanon, Libya, and Iraq face terror or are at war.

4. The gap between the middle and upper class continues to be worthy of much discussion. The increased cost of health care and education are factors weighing heavily on the middle class of this country. We don’t believe the answer is just raising taxes or engaging in class warfare. Encouraging business investment and retraining of the unemployed needs to be encouraged while infrastructure investment needs to be made and paid for. These and other factors must be addressed to give the middle class a way to achieve better jobs, higher pay and greater financial security. However, the income inequality rhetoric at the city, state, and federal level will continue to cause angst and chill job creation.

5. Price-earnings ratios expanded significantly last year and much of the gains in equity markets resulted from this expansion. Earnings growth provided a smaller portion of the gain. 2014 should be a year of continued earnings growth, but we would be surprised if P/E’s continued to expand. Any disappointment in earnings growth, or the growth in global GDP, could cause a contraction in price-earnings multiples that could cause a

market decline. Stock picking will be increasingly important.

6. There will always be issues and factors that we cannot forecast, but can cause disruption.

We are somewhat worried about the growing consensus by financial gurus advising

investing in the stock market while predicting doom for the bond market (you might recall our letter from October 28, 2010 urging stock market investing before you could “see a bandwagon”). We worry a bit when the herd is echoing our advice.

Our Strategy for 2014

We believe the following asset allocation makes sense:

1. Underweight fixed income – We expect that long-term interest rates will trend up, with the Fed tapering and eventually eliminating quantitative easing. This will cause paper losses for those who have extended out their bond maturities. At the same time, with Janet Yellen taking over the helm of the Fed, there will be an even greater focus on employment and wage gains as a measure of the health of the economy. Given this bias, we expect short-term rates to stay quite low until significantly more sustainable progress is made by the job market. Investors holding cash and short-term fixed income will likely be losers with returns less than the rate of inflation. Accordingly, we will recommend t hat our clients continue to underweight fixed income and keep duration/maturities reasonably short. Our clients do not like seeing paper losses even though they profess that they will hold to maturity and ignore the red ink. We will continue to only buy high-quality investment-grade bonds in a laddered manner (except for institutional clients with broader investment guidelines).

2. Overweight defensive strategies – We have two strategies that we believe are somewhat defensive. One strategy is concentrated in fine growth companies providing clients with above-average earnings growth, in addition to selling call options to capture an additional cash stream, which helps performance in low growth or declining markets. The other strategy relies on financially-strong, large companies that have a culture of returning cash in the form of dividends to its shareholders as part of its DNA. These companies, on average, have raised dividends for more than twenty years and we believe will continue to raise dividends annually. We believe that these two strategies give clients significantly better returns than fixed income for the foreseeable future. Both provide transparency, invest in high-quality businesses and provide some downside protection from either a growing dividend stream or from more rapid earnings growth coupled with the collection of cash premiums from selling call options. Given the significant increase in the stock market last year and the wall of worry that confronts us, these strategies make a lot of sense for every suitable investor in the event 2014 turns out to be a more challenging environment.

We will be adding a third strategy to this defensive basket (renamed “defensive” from

“defensive equities” to account for this addition) that will make sense for some of our

suitable clients. This investment will be less correlated to the equity markets. We have

been conducting due diligence on this investment for over a year. We will send out a

separate letter to those suitable clients regarding this with a full explanation of its merits for their consideration. Our pension fund and some of us at FLI (including me) have already made investments in this strategy.

3. Sensible allocation to traditional equities – Our traditional equity strategies did extremely well last year. Our primary focus on among best of breed managers with concentrated portfolios produced excellent results. Given our view that the global economy and corporate earnings will reasonably grow with the greatest contribution coming from the U.S., we believe that a full allocation to traditional equities makes sense. We are overallocating to domestic U.S. strategies. We believe that these strategies will provide us with ample exposure to Europe and Japan as well as modest exposure to emerging markets through the global footprint of U.S. companies. This should provide us with the safest investment opportunities (in the equity arena) with the least disruption from government instability and currency issues. Over the long term, we still believe that equities make great sense through investment in high-quality, well-managed businesses. Since the “decession,” we have implored clients to invest in both traditional and defensive equities and we believe this makes sense again this year. The mountain of money on the sidelines, as well as individual and institutional investors over-allocated to bonds, will likely continue to provide a source of funds to be invested in high-quality companies. This, along with growing earnings, should help this asset class reasonably appreciate. We believe that this allocation makes sense for all clients. However, the rising tide of 2013 will probably not be with us to the same extent in 2014. Thus, investing carefully in concentrated portfolios made up of the best companies backed by growing earnings and/or growing dividends at extremely attractive valuations is essential. We are confident that we can provide that to you in our various traditional equity strategies.

4. Modest allocation to private equity/real assets – Private equity should benefit from an improving economy, a more robust merger environment, and a better stock market supporting a greater number of initial public offerings. At the same time, the remnants of the financial crisis still represent some significant investment opportunities especially in the credit and distressed asset areas. We continue to look for reasonable investment opportunities to participate in this asset class. In addition, the recovery in real estate may also be a sustainable and fertile area for investment. However, pricing and available liquidity present challenges to finding attractive investments. We will continue to pursue this area and bring to our clients investments that we find attractive.

In summary, 2014 is a year where we advise staying the course with some defensive shift of one’s asset allocation based on the success of 2013 and the changing financial and political climate (as we believe Ben Graham would have suggested). The proverbial wall of worry still exists but the wall seems to have gotten shorter. Long-term equity investing is paying off and should continue to do so as domestic financial institutions are stronger, corporate earnings are growing and valuations are no longer cheap but reasonable in our opinion. Those pundits, who several years ago suggested that one could no longer be a long-term investor in great companies, did not know what they were talking about. Those who believed that the bull market in bonds would last forever are facing an uphill battle. Investing prudently, while considering the economic, political and geopolitical challenges, makes sense with a goal of achieving a fair return on capital as opposed to just a return of capital.

As asset allocations should be individualized, we look forward to working with you to help you achieve a prudent asset allocation for this year and years to come.

Best regards and best wishes for a healthy, happy and prosperous New Year,

Robert D. Rosenthal

Chairman, Chief Executive Officer

and Chief Investment Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may

differ materially. Past performance statistics may not be indicative of future results.

Disclaimer: The views expressed are the views of Robert D. Rosenthal and Ralph F. Palleschi through the period ending January 15, 2014, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Content may not be reproduced, distributed or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC .

Copyright © 2013 by First Long Island Investors, LLC. All rights reserved.

Jericho, NY: The Diabetes Research Institute Foundation (DRIF), the nonprofit organization whose sole mission is to support the cure-focused work of the Diabetes Research Institute at the University of Miami Miller School of Medicine, is pleased to announce that Bruce A. Siegel of New York, NY, has been appointed to serve as co-chairman of its recently-consolidated Northeast Region Board, according to National Chairman Harold G. Doran, Jr. He will serve alongside Marc S. Goldfarb of Short Hills, NJ.

Robert Rosenthal, FLI’s Chairman, CEO, and CIO, welcomed friends and clients of the firm to the Garden City Hotel to discuss the future of higher private education with Stuart Rabinowitz, President of Hofstra University. This event also celebrated the 30th anniversary of First Long Island Investors, a milestone achievement for a wealth management company on Long Island, and one that many in attendance have benefitted from over the years. President Rabinowitz addressed the challenges facing higher private education institutions today and the keys to success going forward.

Bob Rosenthal welcomes clients and friends to First Long Island Investors’ 30th anniversary celebration.

Stuart Rabinowitz, President of Hofstra University discusses the future of private higher education.

President Rabinowitz started by acknowledging the widespread concern about the cost of college tuition and made clear that private universities must justify the value of the education that they provide. For most private schools (those without huge endowments), tuition supports almost all of the university’s expenses, of which as much as 75% are for personnel expenses. These expenses can include union jobs, which have contracted pay increases, and generous healthcare and pension contributions for all employees and their families.

President Rabinowitz explained that students at private universities, on average, pay 40 to 50% less than the stated tuition rates. However, by discounting tuition, in order to attract a better and more diverse student body, a university is accepting less revenue. Hofstra has positioned itself as a “premier private institution on Long Island; and the public sees a Hofstra degree as a valuable asset.” To continue to be competitive, Hofstra must focus on quality and reducing unnecessary operating costs.

President Rabinowitz focused on three keys to success for higher private education institutions in the future. First, universities must have a strong endowment to help defray rising costs as students are less willing to pay increasing tuition bills. Second, universities will need to reduce costs by becoming more efficient and cutting ancillary services. Finally, universities must focus on building a solid brand. Hofstra has made great strides in improving its brand by partnering with North Shore-LIJ on a state-of-the-art medical school, and becoming just the second university to host back-to-back presidential debates. President Rabinowitz finished by emphasizing the importance of providing an education that justifies the price, by giving students not only a degree but a quality education.

Stuart Rabinowitz

Stuart Rabinowitz

Stuart Rabinowitz was chosen by the Hofstra University Board of Trustees to serve as the eighth president of the University on December 20, 2000. Prior to his appointment, he served as dean of Hofstra University School of Law from September 1989 through June 2001. He joined the faculty of the Law School in 1972. President Rabinowitz currently holds the Andrew M. Boas and Mark L. Claster Distinguished Professor of Law.

“The stock market is filled with individuals who know the price of everything, but the value of nothing.”

Philip Fisher (Noted investor and author of Common Stocks and Uncommon Profits)

Summary Review

The third quarter was a very successful one for our clients where meaningful gains were achieved in our defensive and traditional equity investment strategies. These followed substantial gains achieved in the first two quarters. Performance of equity strategies for the year now ranges from 10.7% (one of our defensive strategies) to 19.3%, net of all fees. At the same time, bond markets continued to trade in a narrow range for the quarter, somewhat helped by the Fed’s decision at a meeting in September to not taper its bond purchases. This resulted in very modest recent gains for bond investors. Still most bond investors, including our clients, have incurred small losses year to date. Alternative investment classes did not fare nearly as well as traditional equities (in particular, long/short and market neutral strategies). The “wall of worry” continues to gnaw at investors as they digested the government shut down, weaker economic data, and geopolitical issues. This is causing some investors to continue to leave large amounts in cash, or overly allocated to bonds, which have virtually no expected return after inflation.

The above quote is timely as it speaks to the issue of value given the recent rise in the stock market and the continuing low-interest-rate environment. So, one asks, where do we go from here and where is there true value for investors? Is it in stocks, bonds, real estate or private investments? Our job as wealth managers and investors is to constantly evaluate the long-term prospects of the asset classes we invest in, and the opportunities within those asset classes. We use a disciplined approach to valuation and compare the reasonableness of valuations across the different asset classes to which we deploy capital. We recommend that our clients allocate their capital where we believe the expected risk-adjusted return is most compelling. At the same time (because we do not have a crystal ball), we maintain needed diversification throughout our security, defensive equity, and traditional equity baskets, as well as private investments (where appropriate). This provides some insulation from unwelcome surprises. It also provides access to investments that are not always correlated to each other.

For now, we still view our defensive equity investments as providing the greatest risk-adjusted return opportunities over the longer term. This reflects our optimism about select corporate earnings; cash flow from both dividends and selling call options, balanced with the uncertainty in Washington from both a political and monetary standpoint. In addition, given the low interest rate environment, mountain of money on the sidelines, and the continued skepticism of many individual and institutional investors to owning stocks, we still believe there is value and upside in both our defensive and traditional equity strategies. Bonds, on the other hand, do not present much value in our opinion and returns will be hard pressed to exceed the rate of inflation on an after-tax basis. This is especially the case as modest interest rate increases can be expected in connection with the Fed’s ultimate decision to taper its bond purchases. Thereafter, sometime in late 2014 or 2015 we expect an increase in the Federal Funds Rate. These changes to Fed policy will likely result in some volatility. Just how much will be determined by the extent to which an offset could be forthcoming from a better economy. At this time with global growth still modest and pro-growth fiscal policies still impeded by political paralysis, it is hard to predict just how severe the volatility will be. Over time however, the earnings yield, dividend yield and growth prospects of the companies we invest in (depending upon the specific strategy) should continue to provide appreciation potential as well as dividend growth.

Internationally, emerging markets are not as strong as had been hoped for, and the demand for commodities remains tepid, slowing commodity-driven economies, such as Brazil. Europe, having stabilized, seems to be growing at a very modest pace and possibly still faces some banking issues. These factors have not been reflected sufficiently in valuations for companies outside the U.S., in our opinion. Accordingly, we remain underweight international strategies, but are watching closely for any signs of significant economic improvement or more compelling valuations.

The combination of Washington dysfunction, eventual Fed tapering, weaker emerging markets, slow employment growth, and a solid housing recovery coupled with modest inflation makes for an interesting investment environment. This should auger well for investment in companies that can generate revenue and earnings growth while growing free cash flow. The unsettling factors keep us somewhat skewed towards our defensive equity strategies (one of which continues to perform better than its benchmark for the sixth year in a row, while the other ranks in the top 10% of large-cap investment strategies since its inception based on the PSN database), while still maintaining a meaningful exposure to traditional equities. This seems to be the right path while continuing our modest fixed-income exposure until rates are more compelling. We still believe that corporate earnings are growing thereby supporting equity investing, and stock market skepticism, along with low-returning bonds and cash, should ultimately give way to greater allocations to equities. This could provide the next leg up in the equity markets.

As you know, some of our strategies utilize among best of breed outside managers. We meet and or speak with them on a quarterly basis. Most recently, one of our small-cap growth managers came to visit us from Minneapolis. This manager has a great record and they are seasoned veterans. The point we would like to share with you is our continued amazement at the great companies that are spawned in our country. This manager’s portfolio consists of about 50 companies, virtually none of which one would know by name, that are growing robustly and have great future growth potential. When one views these as business investments and not just stock symbols, they take on an added dimension. We and the outside managers we work with continue to find such opportunities for you.

Finding value in bonds, stocks, or private investments is a very necessary pursuit for us as investors (and remember, we invest side by side with you in all strategies except bonds, which are personalized for each client). We as professionals spend the majority of our time doing that for our clients. It requires skill, time, experience, and judgment. We remain committed to that process on your behalf and believe that you, as our clients, will have the opportunity to grow your net worth while we never lose sight of preserving your capital.

Please call us with any questions you might have. As a reminder, our Thought Leadership Series continues on November 12th at The Garden City Hotel. Stuart Rabinowitz, the President of Hofstra University, will be our guest speaker. He will discuss the future of private higher education. This is a very hot topic being discussed around the country, including by President Obama. We are also very pleased to announce that we are celebrating our thirtieth anniversary this month, and we will make special note of that at our seminar (including a useful give away). Please join us if you can. (Please RSVP to Lisa@fliinvestors.com.)

Best regards,

Robert D. Rosenthal

Chairman and

Chief Executive Officer

Ralph F. Palleschi

President and

Chief Operating Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results.

Disclaimer: The views expressed are the views of Robert D. Rosenthal and Ralph F. Palleschi through the period ending September 30, 2013, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Content may not be reproduced, distributed or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC . Copyright © 2013 by First Long Island Investors, LLC. All rights reserved.