Following the sharp decline in the equity markets to close 2018, investors have concern about the outlook for 2019. On February 7, 2019, members of the First Long Island Investors Investment Committee held a web seminar where they shared with clients and business colleagues our perspective on the markets, domestic and global economy and when the next recession is likely to occur. These factors and more were incorporated into our latest thinking on asset allocation to position client portfolios for long-term growth.

On October 30th, First Long Island Investors had the distinct honor of hosting Lawrence Levy, Executive Dean, National Center for Suburban Studies (NCSS) at Hofstra University, as our guest speaker at a Thought Leadership Breakfast for clients and friends of the firm.

Lawrence Levy, Executive Dean, National Center for Suburban Studies (NCSS) at Hofstra University (left) and Ralph Palleschi, President and Chief and Operating Officer, First Long Island Investors (right)

In 35 years as a reporter, editorial writer, columnist, and PBS host, Lawrence (Larry) Levy won many of journalism’s top awards, including Pulitzer Finalist, for in-depth works on suburban politics, education, taxation, housing, and other key issues. As a journalist, he was known for blending national trends and local perspectives and has covered seven presidential campaigns and 15 national conventions. In his leadership role at NCSS, which he was invited by Hofstra President Rabinowitz to create in 2007, Dean Levy has worked with Hofstra’s academic and local communities to shape an innovative, interdisciplinary agenda for suburban study, including a new Sustainability Studies degree.

Mr. Levy centered the conversation on the changing demographics on Long Island and how that has impacted education, business, real estate, politics, and more. He described Long Island as a diversified center for small business creation, at the best it has ever been economically. Exports are at highs not seen in decades, unemployment stands at 3.5%, and it has been aided by government defense spending as well as small businesses picking up a lot of the economic slack. On the flip side, he described Long Island as a place with an aging demographic as well as aging infrastructure (bridges, roads, sewers, etc.). The governmental fragmentation on Long Island makes it extremely hard to get initiatives passed to deal with some of Long Island’s issues such as its aging infrastructure.

The segregation of cultures that exists on Long Island is a core issue. Long Island currently has one of the highest segregation rates throughout the United States. This segregation dates back to the 1960’s when practices such as blacklisting, gerrymandering, and pure policy were used to ignite the movement of minority cultures into certain areas. Banks would reject people of certain ethnicities with equal standards simply because they did not want them taking out a mortgage for a home in certain areas. This has been detrimental to certain cultures that have spurred growth and diversity in Long Island.

According to Mr. Levy, a multitude of ethnicities have contributed to Long Island’s economic success. The Asian population, which has been growing at rapid rates, has helped support Long Island’s housing market. Latino groups continue to bring “new worlds” to communities, with an influx of diverse ideas and capital. Additionally, people of African ethnicities continue to choose suburban areas throughout Long Island as opposed to moving into New York City. Long Island has been “very fortunate” to have this cultural diffusion, in the words of Mr. Levy, but the segregation that exists on Long Island has caused some of these minorities to be placed at a disadvantage, particularly regarding the education that children receive in certain areas. For example, the Hempstead School District offers no advanced placement courses to its high school students, not only depriving them of advanced education but putting them at a disadvantage for continued education in college in comparison to their peers. According to Mr. Levy, 50% of students on Long Island are non-white, and 80% of them attend the poorest 15 districts (out of 125) on Long Island. He shared that issues like this only garner attention when they get penned as a “pocketbook” issue. He is concerned this segregation may never end and could require some external force such as artificial investment or de-stereotyping to make significant strides.

The conversation transitioned to a discussion of the notion that Long Island is being hit on both ends – the aging of our population and that young millennials are not choosing to live on Long Island because it is said to be too expensive. Mr. Levy disagrees with this pre-conceived notion and pointed to many booming “downtown” areas such as Rockville Centre and Huntington where apartments and housing are quite affordable. He believes the issue is more that young people are simply being raised to expect a luxurious house immediately after graduation. In order to combat this issue, there has been a focus on smart growth by which housing development aims to optimize housing for both younger and older residents who may not want a multi-purpose housing unit and converting unused parking lots into apartment complexes to bolster the housing supply. Naturally occurring retirement communities (NORC’s) have also aided in sustaining the elderly population as reinvestment in the property of these communities (wider doorways, simpler structures) are more appealing to this group.

More about the speaker:

Over the years Larry Levy has forged research alliances with other academic institutions, including Harvard, Columbia, Cornell, Boston College, Virginia Tech, New York University, Exeter, and Maynooths, as well as consulting relationships with not-for-profit groups, businesses and government agencies. One recent partnership of note, with the world-renowned Schomburg Center for Research in Black Culture, resulted in the heralded exhibition “Black Suburbia: From Levittown to Ferguson.” Along with Academic Director Christopher Niedt, NCSS has promoted the importance of studying suburbs nationally and internationally and has generated nearly $4 million in grants, gifts, and contracts. Dean Levy was recently invited to lecture at the Harvard Graduate School of Design and the Harvard Medical School on the challenges of the changing suburbs and gives about 30 talks a year to academic, civic, and business groups on a variety of topics. As a member of a Brookings Institution advisory panel, he was a featured speaker at a Brookings Metro Policy Summit in Washington, DC. He was recently appointed Chairman of the Community Research Advisory Board at the Feinstein Institute for Medical Research, one of the world’s leading such centers.

About the National Center for Suburban Studies (NCSS):

NCSS has collaborated on a number of local, national, and international scale conferences on aspects of suburban life, from diversity and housing, to ecology science and health care. The center also has participated in major consulting studies on sustainability, demographic change and education and health care challenges in suburbia. At NCSS, Dean Levy has co-authored major regional studies, including the LI2035 Sustainability Action Plan, all five Long Island Regional Economic Development plans, and many of the post Sandy recovery reports for Suffolk County communities. Before joining Hofstra, he was Senior Editorial Writer and Chief Political Columnist for Newsday; cohost of the PBS show Face-Off, and remains involved in the world of journalism and politics. Levy has been a guest contributor to BBC.com, CNN.com, Politico, Newsday, Citiwire, and Hearst Newspapers and wrote about presidential campaign issues for the New York Times.com Campaign Stops blog. (Most of these articles and some of the media appearances can be found at the NCSS website www.hofstra.edu/ncss). He appears regularly on local and national television. He is a graduate of Boston University’s School of Communication. He’s especially proud of organizing the Hofstra Celebration of Suburban Diversity, which annually brings together hundreds of people from different races, religions and other backgrounds and has raised more than $1 million for diversity related scholarships, research and community engagement. At the same time, the event, which has featured the region’s most influential business and labor leaders as keynote speakers, has dramatically raised Hofstra’s profile as a place that values diversity. He also is pleased to be able to “give back” by mentoring many young people in journalism and public life regardless of their ideological or political allegiance.

December 31, 2018

“Patience can be bitter, but its fruit is sweet.” -Aristotle

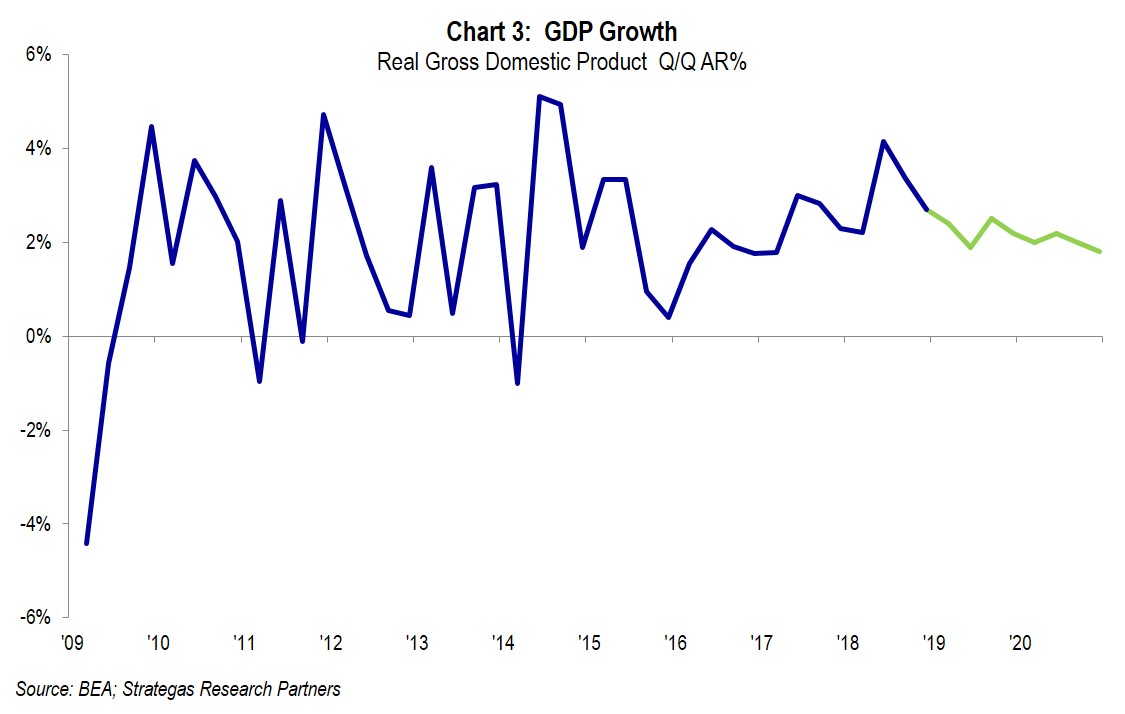

The fourth quarter witnessed a significant downturn for equity markets as well as a decline in energy prices. These downturns were in contrast to strong corporate earnings growth, estimated GDP growth of 2.7% and continued high demand for oil. The equity market downturn was widespread, however value stocks, which had trailed growth during the year, had less severe declines, but declined nonetheless. International stocks, including emerging markets, had substantial declines in the quarter contributing to full year results that significantly underperformed domestic stocks. Commercial real estate remains stable while residential real estate weakened, as mortgage rates slightly increased. This also depended on local market conditions.

For the most part, our defensive and traditional equity strategies fared well in that most met or exceeded their respective benchmarks during the quarter, despite almost all experiencing a significant drop during the quarter. For the full year, all but two of our many defensive and traditional strategies met or exceeded their benchmarks.

Quality, for the moment, did not seem to matter. Strong earnings growth, for the moment, in our portfolio companies for the most part did not matter (there were some exceptions). Better than targeted dividend growth (13.9% on average for the year) in our Dividend Growth Strategy, for the moment, did not matter as well. Overall, when looked at over the two year period of 2017 and 2018 our approach to asset allocation and investment strategies achieved solid results for our clients.

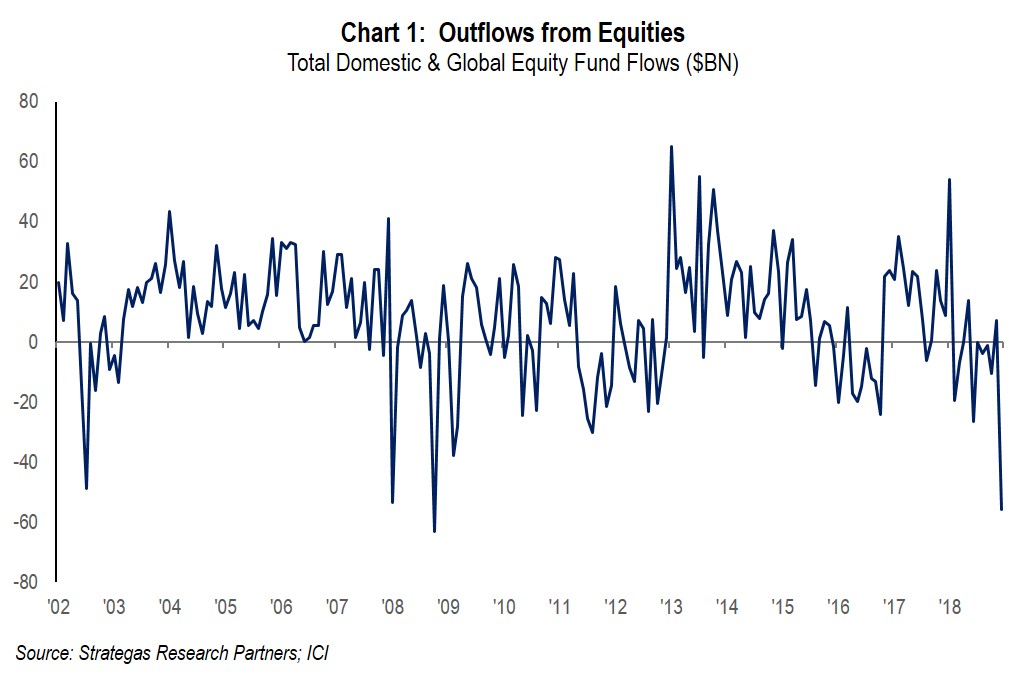

Apparently, what did matter were, in our opinion, missteps in communications by the new Fed Chair on interest rate and balance sheet policy, an attack on him by our President, a take back by the President of what seemed to be progress in talks with the Chinese, and the realization of the obvious — that corporate earnings would likely grow in 2019 but at a much slower pace. In our opinion, these factors, and probably others, led to the largest one-week outflow from equities on record, even greater than in 2008/2009! This makes no sense to us given underlying fundamentals and the strength of our banking system. We believe that withdrawals from ETFs and index funds (passive investing) is what contributed to the widespread decline irrespective of quality, earnings growth, or dividend increases.

It just seems strange to us that record outflows (See Chart 1) would occur when earnings growth is projected to continue and GDP growth also continues, albeit at a slower pace (see Charts 2 and 3).

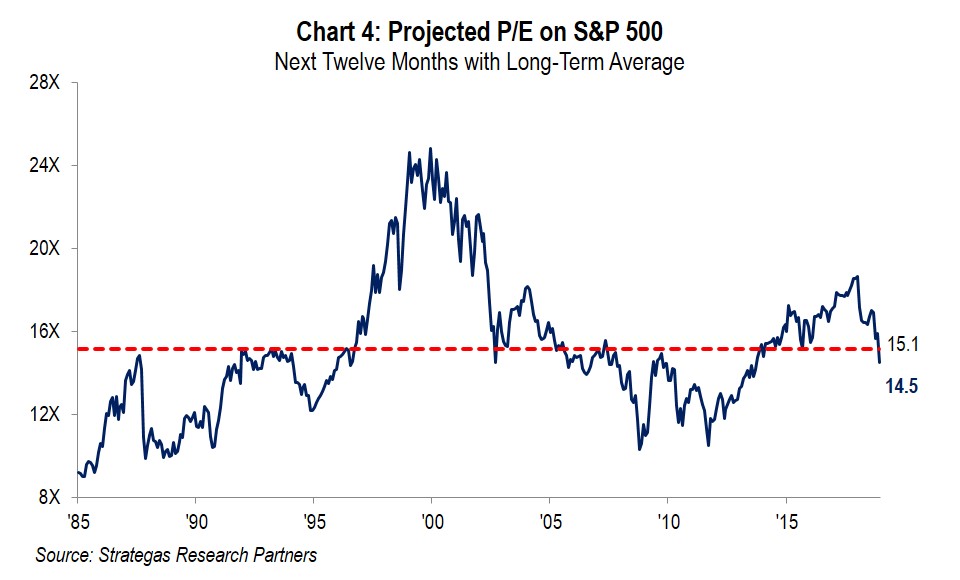

So, without repeating what we spoke of in our annual thought piece, the economy and earnings remain moderately strong while stocks were taken to the “woodshed” in the final quarter of 2018. The result being a below average P/E on 2019 projected earnings.

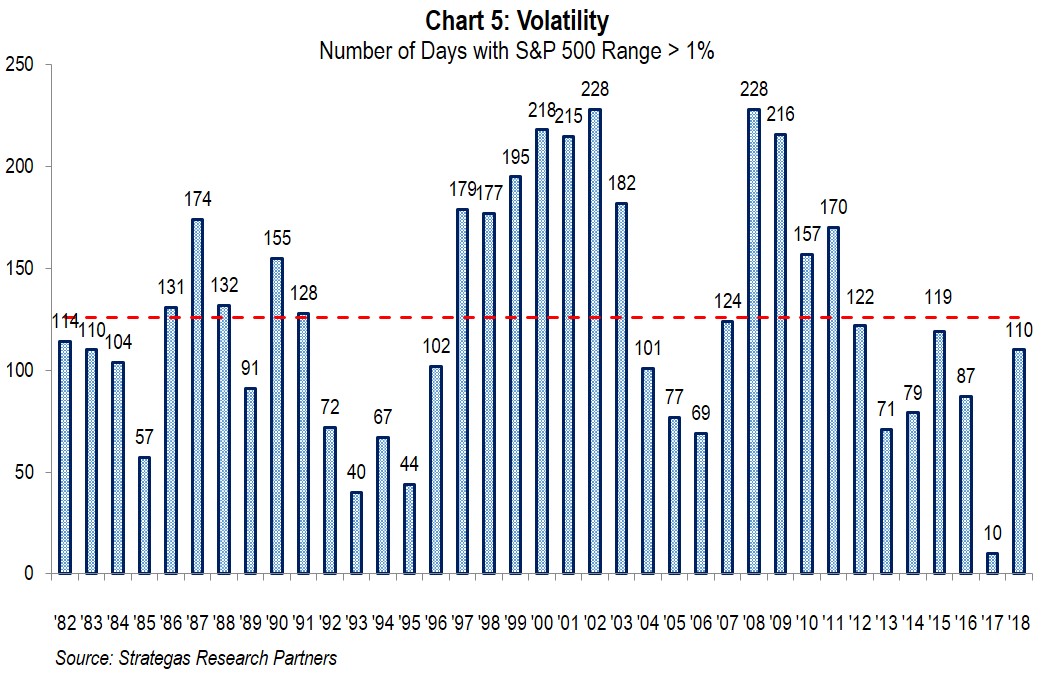

Additionally, volatility picked up in the fourth quarter. In numerous quarterly reports we have warned of increased volatility. Well, it is here but in Chart 5 below you can see that volatility is normal, and where we came from was abnormally low.

By the way, the increased volatility, if it continues, should help one of our defensive equity strategies.

What does it all mean?

The fourth quarter was very difficult for most investors. Equities sharply declined wiping out three quarters of gains for the S&P 500 and then some while short-term interest rates increased while longer-term bond yields declined. Oil prices declined, we believe because of oversupply, which will help consumers and many businesses (acts like a tax decrease). Valuations are now far more reasonable going forward; some would argue cheap when considering where interest rates are.

However, looking forward we now have a split government, a President and his campaign under investigation, key cabinet members departing, a partial government shutdown, and a Chinese trade war still evolving. This is a prescription for more volatility while economic fundamentals remain quite reasonable, for now. We as a firm still do not see a recession for 2019. That is a positive in our opinion.

We will be watching the fundamentals which we continue to believe will reward us as long-term and PATIENT investors. Just think about the impact of we or you having panicked the day or so before the Dow appreciated by over 1,000 points. Prudent asset allocation is our path to withstanding these periods of extreme volatility while prospering over the long term (the last several years have been good to us), and being patient to achieve the sweetness of the bitter environment we have just endured.

We hope you will join us on Thursday, February 7th at 2 PM EST for our web seminar where we will discuss our overall outlook for 2019 and how we are recommending clients portfolios be allocated for long-term results.

The start of the New Year is always a good time to reevaluate your asset allocation and ensure it is aligned to meet your goals. We would be happy to sit down and discuss your individual situation.

Best regards,

![]()

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. Partnership returns are estimated and are subject to change without notice. Performance information for Dividend Growth, FLI Core and AB Concentrated US Growth strategies represent the performance of their respective composites. FLI average performance figures are dollar weighted based on assets.

The views expressed are the views of Robert D. Rosenthal through the period ending January 25, 2019, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC. Copyright © 2019 by First Long Island Investors, LLC. All rights reserved.

2019 and Beyond

“Patience can be bitter, but its fruit is sweet.” – Aristotle

As we focus on the outlook and issues confronting us as long-term investors, it is appropriate to first say thank you. We at FLI have just celebrated our 35th anniversary in representing you, our clients, some of whom have been with us from our very inception. Without you, we would not be writing this note. I mention this because during that period we have been through much and have gained invaluable experience from many good and some perilous periods for our clients (where patience was always required). We now seem to be confronted by a sharply declining and volatile market with some predicting an imminent recession (we are not). Thus after a nine year period of positive results have we either hit a big bump in the road or worse are in a bear market, where many still remember and are influenced by the “decession” of 2008/2009; where many are fretting over the current occupant of the White House and our government in general; where we have a new Fed Chair seemingly mechanically intent on raising short-term interest rates while unwinding its balance sheet; and where the likes of China, Iran, and Russia threaten our way of life and that of many allies? We have a big “wall of worry” to understand and overcome! We must determine how much, if any, of this market decline is based on fundamentals versus investor fear from this imposing wall of worry. Is this a correction, or a transition to a bear market? In either case, we must be patient investors.

For many years FLI held annual seminars where I presented a yearly outlook leading off with the current and seemingly insurmountable wall of worry (now instead I write this thought piece and we hold a web seminar in February). In every outlook and web seminar I have always listed major worries AND the other side of the coin. The flip side being some positives which always included the resourcefulness of American business and American workers, as well as our free enterprise way of life supported by the best, but not perfect, form of government in the world. Our situation seems very much the same today.

I have listed many of the elements contributing to today’s wall of worry in the first paragraph above. A quickly and fiercely declining stock market signifies something, but the real economic factors suggest a disconnect with the recent market volatility (mostly declining).

– Corporate earnings continue to rise (See Chart 1)

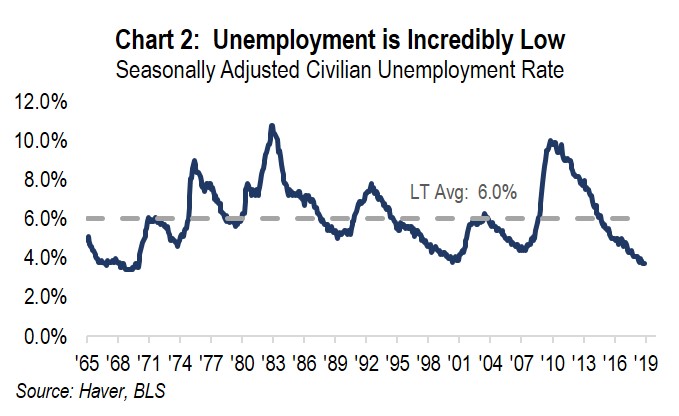

– Unemployment is incredibly low (See Chart 2)

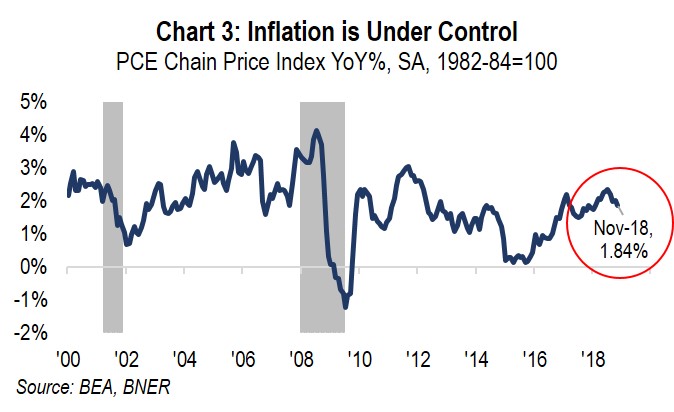

– Inflation is under control (See Chart 3)

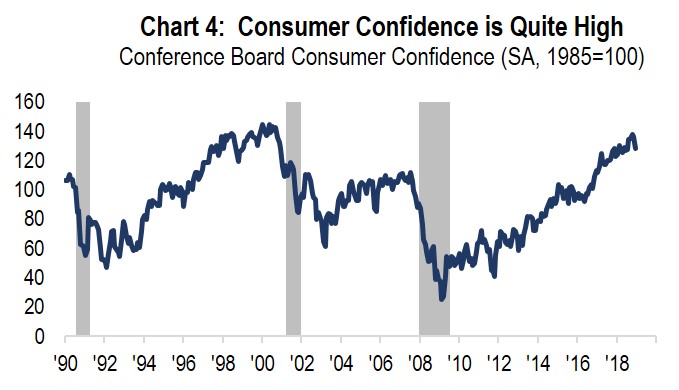

– Consumer confidence is quite high (See Chart 4)

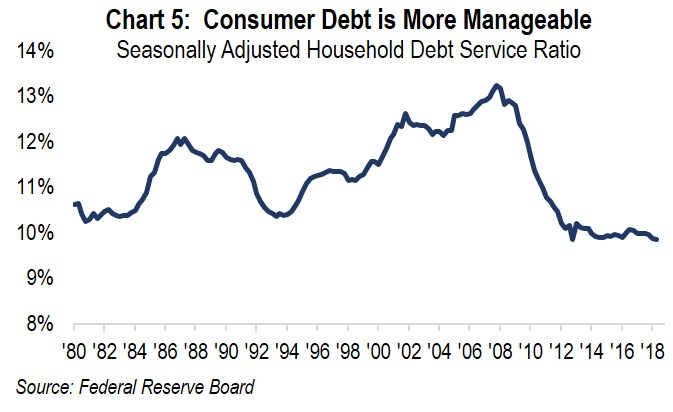

– Consumer debt is more manageable (See Chart 5)

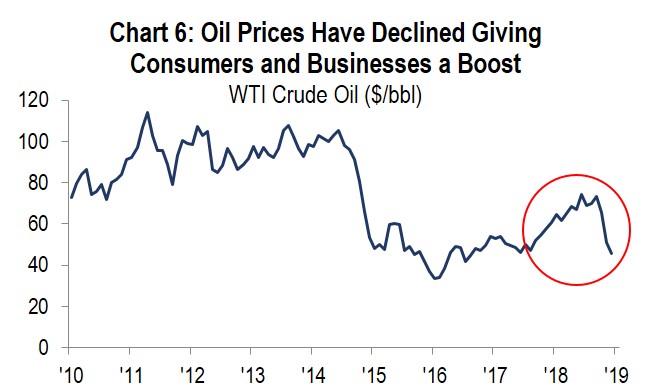

– Oil prices have declined, giving both consumers and businesses a boost (See Chart 6)

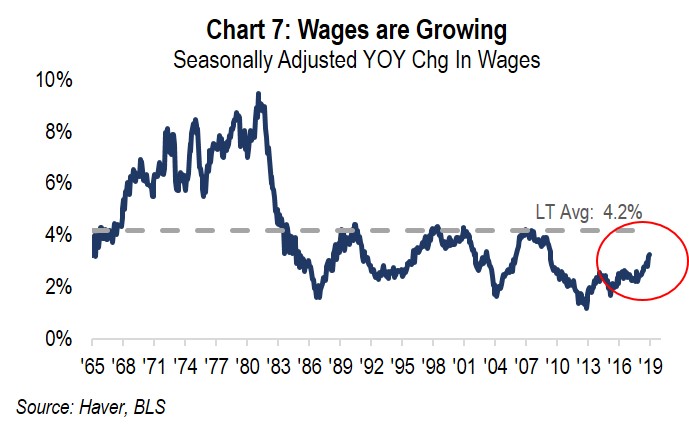

– Wages are growing (See Chart 7)

– And interest rates, despite recent increases, remain historically low (See Chart 8)

Therefore, unless some exogenous event occurs, our domestic economy appears to be reasonably strong. The many charts shown above mostly describe our current fundamentals and characteristics.

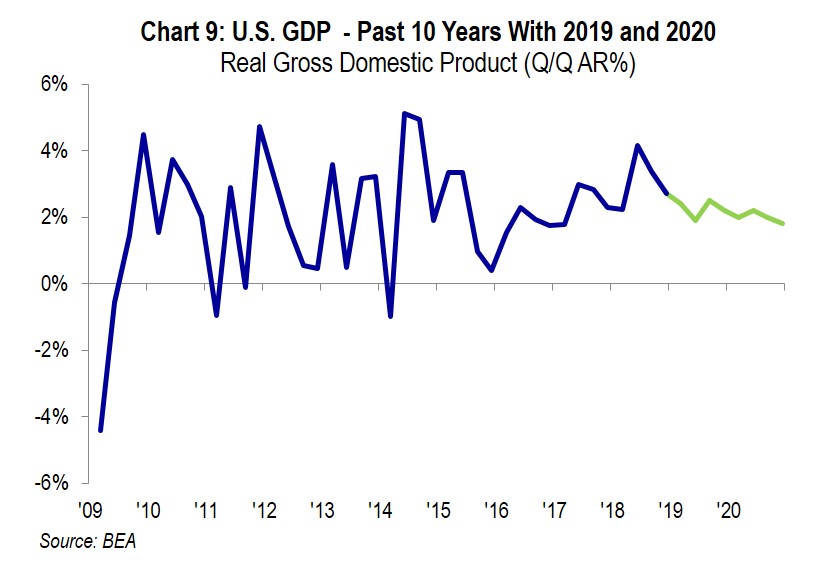

U.S. corporate earnings grew in 2018, in part from the change in tax law as well as from growth in gross domestic product. Looking forward to 2019, U.S. corporate earnings and gross domestic product are both projected to grow (See Chart 1 and Chart 9) although slower than they did in 2018. Notwithstanding this somewhat slower GDP growth, the political uncertainty across the globe and a strengthening dollar leads us to continue to underweight foreign stocks.

But can we be sure these positive economic and fundamental factors will remain in 2019?

In the last six weeks we have spoken with fourteen outside, among best-of-breed, equity investment managers, our partners in our real estate mezzanine loan strategy ,and two highly regarded economic consultants. Generally, their opinions remain positive as to the continuing but slowing growth of the U.S. economy, while the vast majority of companies in which they invest appear to be poised for continued success in 2019 and in many cases beyond.

So, what gives? Certainly earnings growth will slow and eventually we will face a recession (as defined by two consecutive quarters of negative GDP growth). We do not see that for at least the next eighteen months and in our opinion, it should not resemble the “decession” of 2008/2009, which is still fresh in the minds of many investors. The fear of a repeat drove their outflows from equity markets in the past two months. As a matter of fact, these outflows are at record levels, which makes no sense to us given the current positive state of our economy. By the way, we as professional investors, where we have managed wealth for the past 35 years, have weathered many recessions. For now, we do not see significant asset bubbles or an overstretched banking system, the main drivers of the pain and near disaster in 2008/2009. Today’s landscape is quite to the contrary, and we believe the overall contraction in price-earnings multiples, for the most part, is overdone.

However, our national debt continues to increase and that is a concern down the road that must be dealt with by our elected Federal officials. This growing debt is not stalling our economy at this time and with interest rates reasonably low now and for the immediate future, it is not an issue at this point. Inflation, which caused severe economic distress in the late 70’s and early 80’s is below 2% and there do not appear to be signs of increasing inflation. Thus, hyper-inflation which caused poor equity markets in the late 70’s and early 80’s is not in our view. As a matter of fact, until mid-2018 there was more concern about deflation than inflation.

History tells us that bull markets do not typically die of old age, but rather usually end when valuations become too stretched or meet a recession, amongst other factors. Today, in part based on the recent sharp equity decline, equities are somewhat cheap at roughly 14.5 times 2019’s growing earnings. GDP growth for the third quarter of 2018 was 3.4% and the fourth quarter is projected at 2.7% growth. Not even close to a recession. Additionally, the consumer remains buoyant as evidenced by holiday sales increasing by a robust 5.1% over the prior year according to Mastercard. That same consumer is now also benefitting from a significant drop in the price of oil (seems to be supply-driven and not from a decrease in demand). This will give consumers more dollars to spend, save, and/or de-lever.

So what gives and how should we act as investors? BE PATIENT!

Selling into a panicked market where the exits are crowded (record outflows) makes no sense to us especially since there are some pretty positive economic indicators and strong company fundamentals.

We would suggest plain old-fashioned patience and reflection on one’s asset allocation. From our perspective we believe fear and uncertainty have gripped investors who still remember the pain of 2008/2009. We have a new dynamic adding to this pain — the current erratic state in Washington D.C. With the mid-terms resulting in the Democrats taking the House and Republicans remaining in control of the Senate, we have a split government. In addition, we have a President whose policies and demeanor are giving no comfort to many on either side of the aisle. Despite a pro-growth tax bill, deregulation, and criminal justice reform as positives (although some rightfully are concerned about growing deficits), our President has lost several key cabinet members (including Haley and Mattis) and has become inconsistent, in my opinion, on trade with China as well as policy in Syria, while he, his campaign, and other entities remain under serious investigation. These are legitimate worries with little end in sight that could add to greater volatility.

In our opinion, the uncertainty about our President, his trade war with China (yes, both sides of the aisle agree they engage in unfair trade practices), a partial government shutdown, and a Fed Chair who is new in his role (and has not made many investor friends with his statements and increased interest rates) have driven many investors into fear mode irrespective of the many economic and company-specific positives listed above. This negative sentiment is a real worry but should the growing economy and improved company fundamentals prevail (which we believe will be the case), the tug of war should favor patient long-term investors.

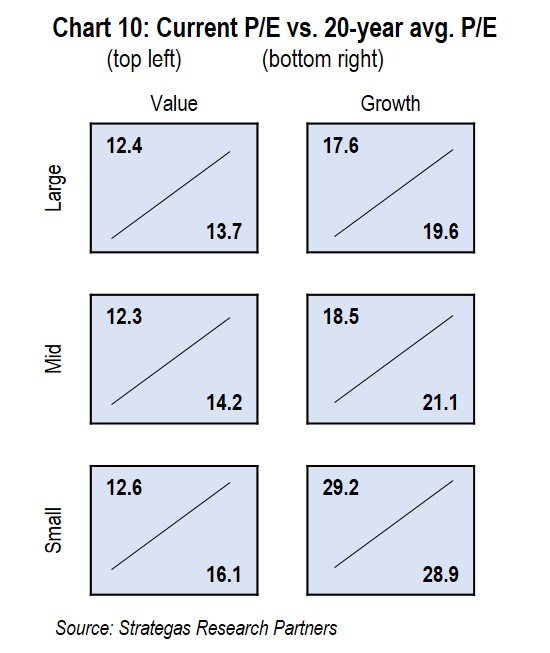

In our view, we still seem to have growing earnings and historically cheap to reasonable valuations (See Chart 10) in a period of stubbornly low interest rates with a modestly growing economy, which would normally suggest higher asset prices for quality companies and quality real estate.

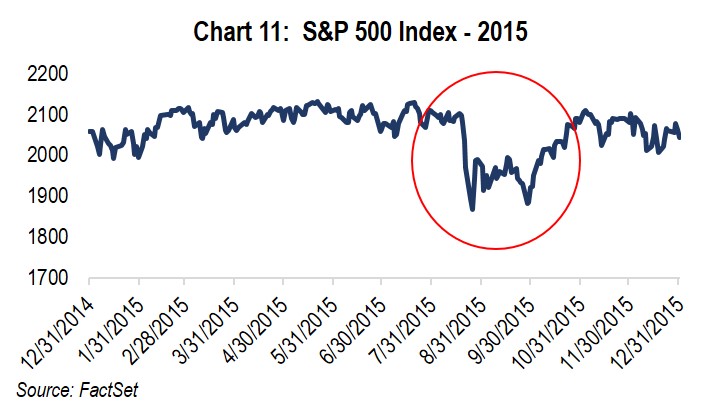

In 2015 we faced a similar conundrum of steep equity losses which turned out to be a correction, and NOT a bear market (See Chart 11). Recently, further steep declines had us at the classic definition of a bear market having dropped 20% from recently achieved highs until a record 1,000 point advance in the Dow and 116.6 point advance in the S&P 500 snatched us from the jaws of the bear.

Summary

None of us have a crystal ball, so we must evaluate all of the above. Relatively strong fundamentals go unnoticed by many investors who are panicked. Could the panic and uncertainty cripple consumer confidence (consumers make up almost 70% of our economy)? Maybe, but we do not think so based on recent holiday sales and dropping oil prices (along with many benefitting from the tax reform). Is the uncertainty enough to completely derail business growth despite pro-growth tax reform and deregulation helping many businesses? Again, we do not think so. Can our erratic government drive investors to more than temporarily accept low cash and bond returns? Again, we do not think so especially as Americans can change the makeup of two branches of government in less than two years.

We think the selling is overdone and equity valuations, in most cases, have gotten more attractive, creating opportunity. Furthermore, we believe that growing passive investing (through ETFs and index funds) which does not differentiate between high-quality and lesser-quality companies has exacerbated the decline. Will we face a recession at some point? Yes, but we do not believe it will be in 2019.

So, stay the course with a prudent asset allocation. We continue to urge our clients to take a defensive posture which overweights our defensive basket while still underweighting fixed income and modestly underweighting traditional equities. Private investments make sense for those qualified.

A defensive asset allocation (including a modest amount of cash to weather this uncertainty) can still provide some appreciation while better weathering the ultimate recession or exogenous event no one can predict. We should all consider rebalancing our asset allocations to take into account the current volatility which has made the valuations of even traditional equities more attractive. We are here to help with all of this and any other wealth management needs of you and your family.

Most of all, be patient. As the quote suggests, the fruit of that patience is an opportunity to earn an overall better return than that of bonds or cash and that better return compounds over time. But we must be patient and endure the bitterness of both corrections and bear markets. It is the price we pay for better returns over long periods of time.

As always, we welcome your questions. We hope you will join us on Thursday, February 7th at 2 PM EST for our web seminar where we will discuss the topics mentioned here in more detail and answer your questions.

Best regards,

![]()

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. The views expressed are the views of Robert D. Rosenthal through the period ending January 8, 2019, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC.

FLI average performance figures are dollar weighted based on assets.

All performance data presented throughout this communication is net of fees, expenses, and incentive allocation through or as of December 31, 2018, as the case may be, unless otherwise noted.

FLI believes the information contained herein to be reliable as of the date hereof, but does not warrant its accuracy or completeness. This communication is subject to modification, change, or supplement without prior notice to you. Some of the data presented in and relied upon in this document are based upon data and information provided by unaffiliated third-parties and is subject to change without notice.

NO ASSURANCE CAN BE MADE THAT PROFITS WILL BE ACHIEVED OR THAT SUBSTANTIAL LOSSES WILL NOT BE INCURRED.

Copyright © 2019 by First Long Island Investors, LLC. All rights reserved.

The Tax Cuts and Jobs Act of 2017 limited itemized deductions which impacts the deductibility of charitable contributions. As part of a recent Family Wealth Roundtable discussion that FLI held for clients, we discussed ways that philanthropic clients can adjust how and when they make charitable contributions to reduce their Federal income taxes.