September 30, 2019

“The future is never clear; you pay a very high price in the stock market for a cheery consensus. Uncertainty actually is the friend of the buyer of long-term values.” – Warren Buffett

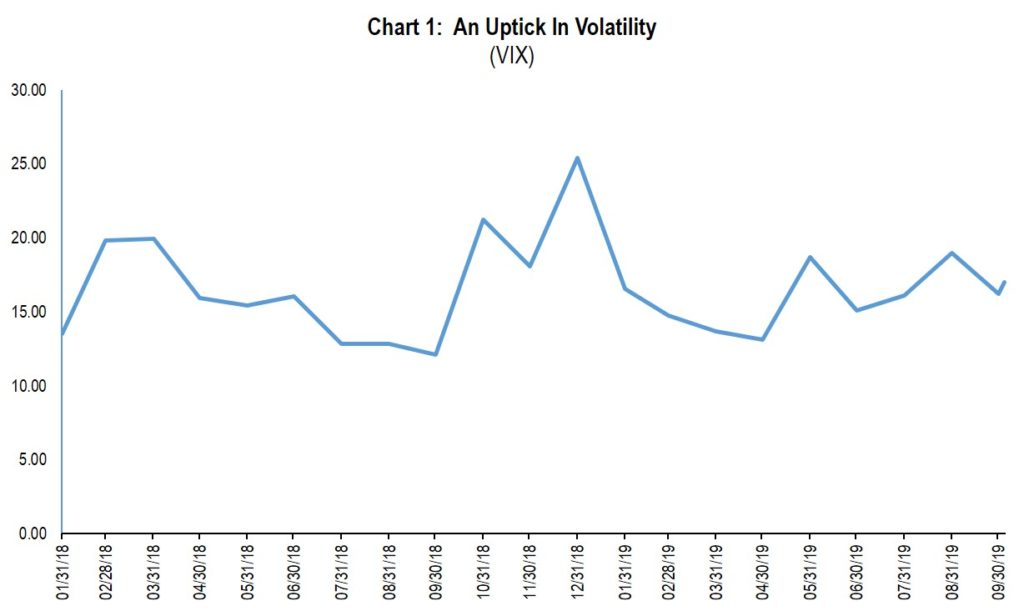

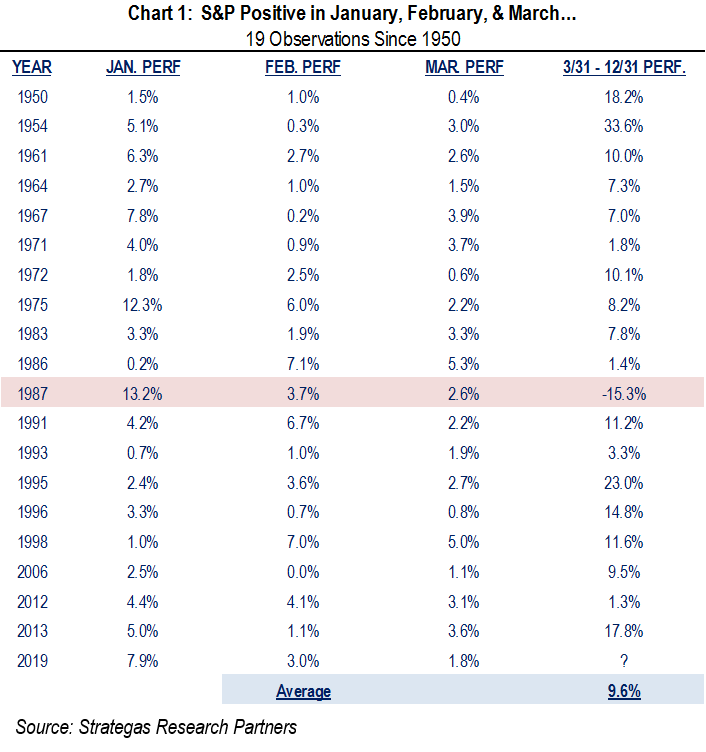

The third quarter ended on a higher note despite many uncertainties including the political maelstrom of potential impeachment of the President. This adds to an already long list of investor concerns including China trade, Iranian aggression in the Middle East, unknown proximity to a recession, an upcoming election cycle, and the future path of interest rates from the Federal Reserve. These factors increased volatility over the second quarter, as you can see in Chart 1.

Given the list enumerated above, it is no surprise that volatility picked up but probably not as much as one would have expected. As a matter of fact, up to this point, the volatility seen so far this year is not out of the ordinary from a historical standpoint. Of course, the year is not over and perhaps there is more to come.

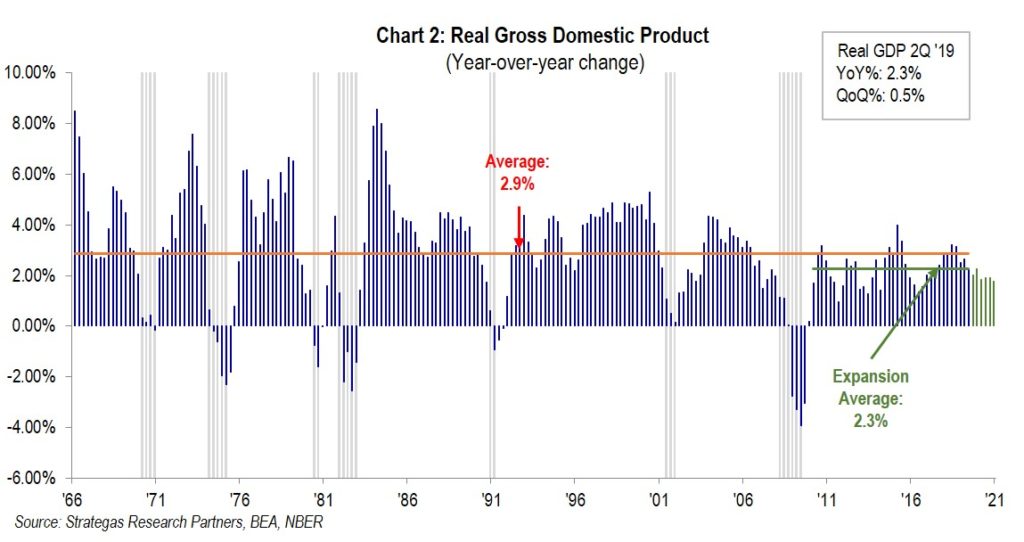

The quote we have chosen this quarter suggests (and we agree) that when the consensus is too optimistic we as investors should be concerned. While the current environment is not “cheery” we are still concerned and our level of concern is somewhat heightened when many believe the end of the bull market is here because we are on the brink of recession; or we are about to go to war; or valuations for the companies we invest in are in nosebleed territory. We do not think we are on the brink of recession; we do not believe we will have an all-out war because of the Iranian actions in the Middle East; and we do not believe that valuations for the companies we invest in are foolishly high. In our opinion, we do not believe the market in general is in nose bleed valuation territory nor that the economy is rolling over, just slowing somewhat. So, let us look at some charts that will help guide us in terms of valuation and overall economic health:

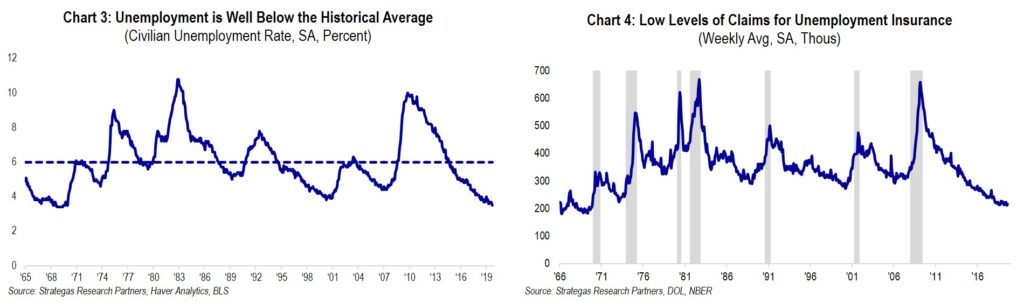

The above charts, measuring key economic data as the third quarter ends, indicate to us that the domestic economy continues to move forward, albeit at a slower pace, despite the concerns that currently prevail. GDP growth, coupled with strong employment, shows an underlying moderately growing and healthy economy. Chart 4 shows a very low level of weekly jobless claims which demonstrates a continued strong labor market and certainly is not a sign of imminent recession.

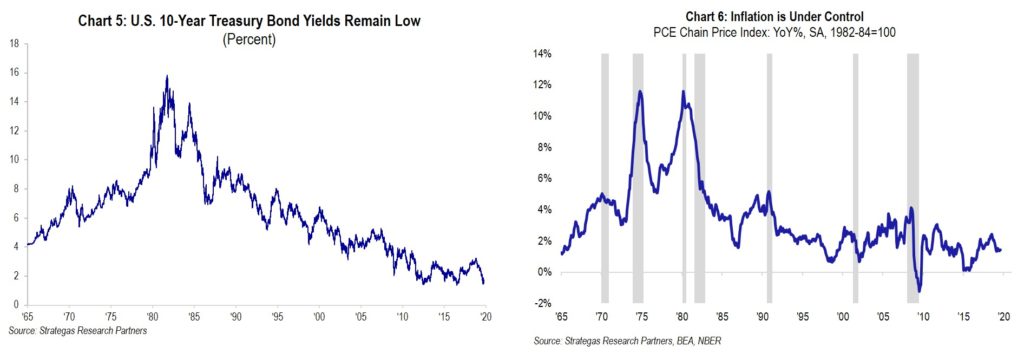

As for interest rates and inflation, the following charts indicate that at current levels both are supportive of a growing economy led by the consumer:

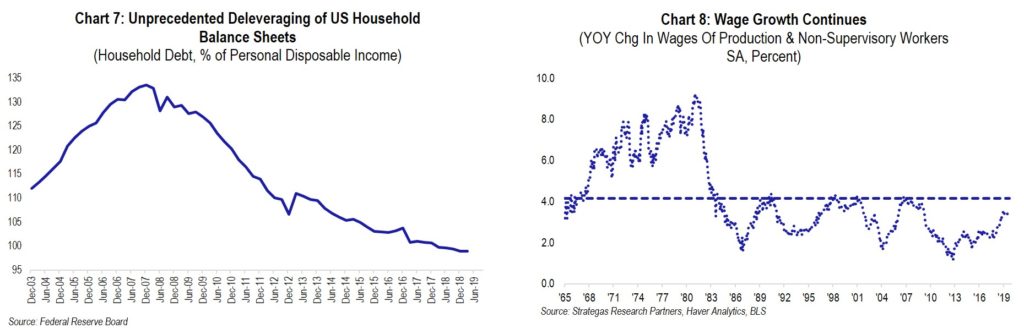

Charts 5 and 6 are both significant when focusing on the importance and health of the consumer. Low interest rates and low inflation are important factors, in our opinion, when determining the underlying strength of the consumer which makes up approximately 68% of the U.S. economy. Add to this the low level of consumer debt (Chart 7) as well as continued moderate wage growth (Chart 8), and this suggests to us that a meaningful driver of our economy remains strong:

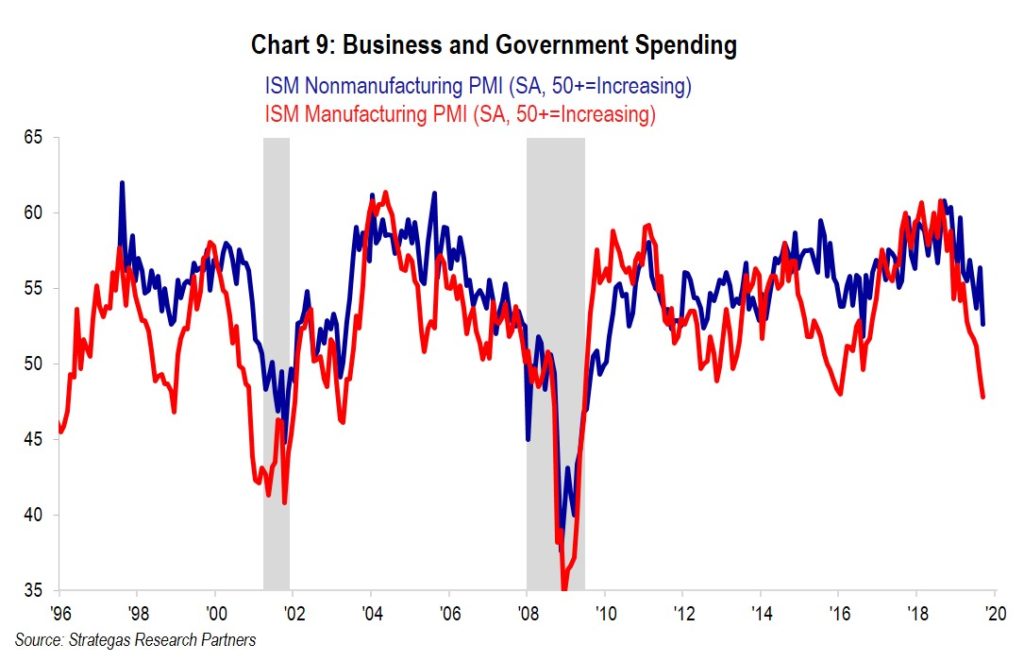

Other factors that contribute to our domestic economy include the strength of business and government spending. Here the picture is more mixed and presents a meaningful concern:

Chart 9 (above) shows that business spending has slowed, and in our opinion this reflects fallout from the trade war with China. It also could reflect the beginning of business concerns about the domestic political environment. The back and forth negotiations, which have been ongoing for more than a year, have resulted in harmful tariffs impacting the U.S. and China as well as other parts of the world, particularly Europe. Our economic consultants believe that this will likely shave one half of one percent from growth in our gross domestic product. On the other hand, as we enter an election cycle (which historically has been good for equities), it is well known that the incumbent administration attempts to spend more to help the economy along. Government spending has accelerated thus far this year and in our opinion will continue to. We are not sure that government spending can offset the reluctance of businesses to spend, but it will help. We will watch carefully to see if the slowdown in the industrial sector spending spreads to the service sector which would add to our worry about business output.

On the global scene, it appears that Europe’s economy is barely growing and has led to the EU reducing interest rates. We believe the continuing uncertainty regarding the UK’s exit from the EU only adds to European economic worries. China’s economy is also slowing as its government is trying to induce growth through fiscal stimuli. We believe that this is being done in an attempt to offset the impact of the trade war with the U.S. In all, these factors have led the World Trade Organization and the World Bank to modestly reduce their forecasts for global trade and global growth which was not robust to begin with, but certainly is not recessionary.

In our opinion, the slower global growth and the continuing concern over a trade war influenced the Federal Reserve’s recent decision to reduce interest rates by another 25 basis points. The investment community expects that the Fed will reduce rates at least one more time this year. We believe it is important for that additional decrease to happen, or equity markets will be very disappointed. (This could result in a rolling over of the equity markets at year end.) We will be watching the last two meetings of the Fed this year very carefully.

The politics of our country certainly make it easy for investors to not be too cheery. The imposing and impending vitriol of impeachment is of concern as it will bring Congress to a standstill (a Congressman told me that gridlock is now worse than ever). As the headlines fly from the media surrounding the President’s phone call with the President of Ukraine as well as alleged pay for play activities of former Vice President Biden and his son, we can expect increased volatility. Thus far, in general, this has not negatively impacted the equity markets. In fact, the quarter just ended resulted in the S&P 500 actually increasing 1.7% in the face of the trade war, an attack on the Saudi oil supply, and the initiation of an impeachment inquiry. Many of our equity investments had a positive quarter despite these factors and all have significant gains year-to-date.

Finally, one of our economic consultants, Strategas Research Partners, points to a nine factor checklist to estimate the likelihood of a bull market top. As of October 1, 2019, all nine do not have check marks next to them suggesting that we are not yet facing a market top and to reiterate, we do not see a recession in the foreseeable future. One of these boxes looks to a market top blow-off where investor optimism results in a buying frenzy. We certainly have not seen that lately. We have included that nine box survey in Appendix I for you to review.

Summary

We had a reasonably good quarter on balance. Equity investing paid off despite the growing wall of worry. Our internally managed defensive equity strategies both had positive quarters. Our Dividend Growth strategy led the way with a 2.8% net gain contributing to a year-to-date net return of nearly 18% (dividends for the strategy up to this point have grown approximately 10% on average). So, our continued bias to being somewhat defensive has certainly contributed to the net worth of our clients while taking less than market risk!

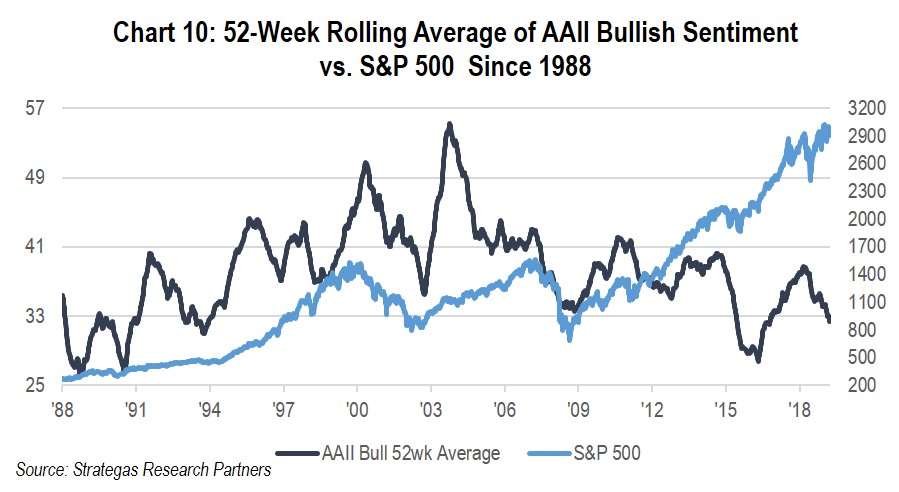

We pride ourselves on being conservative and prioritize return of capital as our most important concern. We also want to exploit the volatility and investor anxiety where we can find opportunity. As Buffett stated, when there is not a cheery market there just might be some opportunity. We do not believe we are in a “cheery market”. The following chart suggests that the individual investor has still not recovered in terms of market enthusiasm since the great “decession” of 2008/2009:

We believe chart 10 (above) suggests an unenthusiastic individual investor, and supports our belief that this has been the most unloved bull market in history. We do not share the same sentiment and will continue to look for high quality equity opportunities. But we can do it while continuing our bias to our defensive equity strategies.

Thus far this year, we have achieved strong performance for our clients with less risk by underweighting fixed income (although bonds have had good returns year-to-date) and overweighting our defensive equity strategies while somewhat underweighting our traditional equity strategies. Going forward, we still believe that recession is not imminent. However, we must take seriously the Democrat’s launch of an impeachment inquiry that could lead to articles of impeachment. Although, at this point, it appears to be a long shot that the Senate will vote to convict the President, the distraction and acrimony in Washington, D.C. could weigh on our economy. At the same time, the President will use whatever tools are available to him to fight the allegations of inappropriate behavior. He is known for being a counter puncher and will do whatever he can to ensure a strong economy which he believes is key to his reelection. History suggests a strong equity market in the final two years of a Presidential term (this being the third and next election year being the fourth). However, an impeachment inquiry possibly followed by articles of impeachment make it difficult to rely on history.

The fundamentals of low interest rates, low inflation, growing GDP, low unemployment, a vibrant consumer, as well as modestly growing corporate earnings should support a reasonable economy and equity market in the fourth quarter. However, anxiety and emotions will remain high given our current political turmoil and international complexities. We view one’s asset allocation to be critical to avoid being too aggressive on one hand or too conservative on the other. Our active management approach continues to focus on companies to invest in that we believe are either reasonably valued with growth opportunities or downright undervalued. We also believe that extremely low yielding fixed income does not present a capital appreciation opportunity or a way to earn after-tax returns above inflation, but remains an anchor in volatile times. So, a modest allocation remains our recommendation for most clients. Our defensive equity strategies, in our opinion, remain an overweight recommendation given their risk/reward profiles in what could be a more volatile fourth quarter and 2020.

Stay tuned! We look forward to reporting to you after year-end. In the meantime, have a wonderful fall and holiday season. We hope you can join us on November 7th for our next Thought Leadership Breakfast at the Garden City Hotel featuring Jon Ledecky, Co-Owner of the NY Islanders. Please call or visit with us for any of your wealth/money management needs.

Best regards,

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. Partnership returns are estimated and are subject to change without notice. Performance information for Dividend Growth, FLI Core and AB Concentrated US Growth strategies represent the performance of their respective composites. FLI average performance figures are dollar weighted based on assets.

The views expressed are the views of Robert D. Rosenthal through the period ending October 23, 2019, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC. Copyright © 2019 by First Long Island Investors, LLC. All rights reserved.

Investors often react emotionally, especially when the market is volatile. U.S. News and World Report recently interviewed our Senior Vice President, Wealth Management and Director of Research, Philip W. Malakoff as part of an article to take a deeper look at stock market corrections and what they really mean.

So far 2019 has seen an up and down stock market which has led to many questions on the minds of investors including will the economy go into recession, the effects of trade wars/tariffs, interest rates, and so much more.

On September 18, 2019 members of the First Long Island Investors Investment Committee held a web seminar where they reviewed the positive economic factors as well as the elements contributing to the wall of worry, all with the goal of making sense of the markets. They covered our approach to investing and how we are recommending that clients adjust their portfolios for long-term growth.

June 30, 2019

“The conventional view serves to protect us from the painful job of thinking.”

John Kenneth Galbraith

The second quarter of 2019 followed two quarters of significant volatility. The decisive decline in equity markets during the fourth quarter of 2018 in our opinion was the result of a Fed misstep as well as an acrimonious mid-term election and a trade war, all of which contrasted with a sound and fundamentally strong economy as well as signs of strength within many of the companies we invest in. The first quarter saw significant volatility but with sizable upside to equity markets reflecting a retreating Fed (altering its position from seeking to raise rates to holding rates unchanged, and now possibly cutting rates), better than expected earnings, and continued employment growth. At the conclusion of the first quarter we communicated that historically when the year begins with three positive months that has typically meant better results for the balance of the year, as you can see in Chart 1 below:

The historical record depicted above is very positive, albeit history is a guide and not a guarantee. It is important to keep in mind that in each of these years of positive performance there has been a drawdown at some point during the period from April to December.

The second quarter saw its share of volatility with the month of April yielding a somewhat higher stock market, followed by a poor May (the S&P 500 was down 6.4%) only to be bailed out by a higher June, leaving us with the S&P 500 up 4.3% for the quarter. Year-to-date the S&P 500 is up 18.5%, which is higher than where it stood at the end of the first quarter, thus following history as depicted in Chart 1. The robust increase was biased towards growth stocks, with the Russell 1000 Growth Index outpacing the Russell 1000 Value Index by 0.8% for the quarter and 5.3% for the year. This continues a pattern of the last two years. Thus, most of our clients, who have followed our guidance on diversification, fared well this quarter by having somewhat greater exposure to growth while still maintaining an appropriate value allocation.

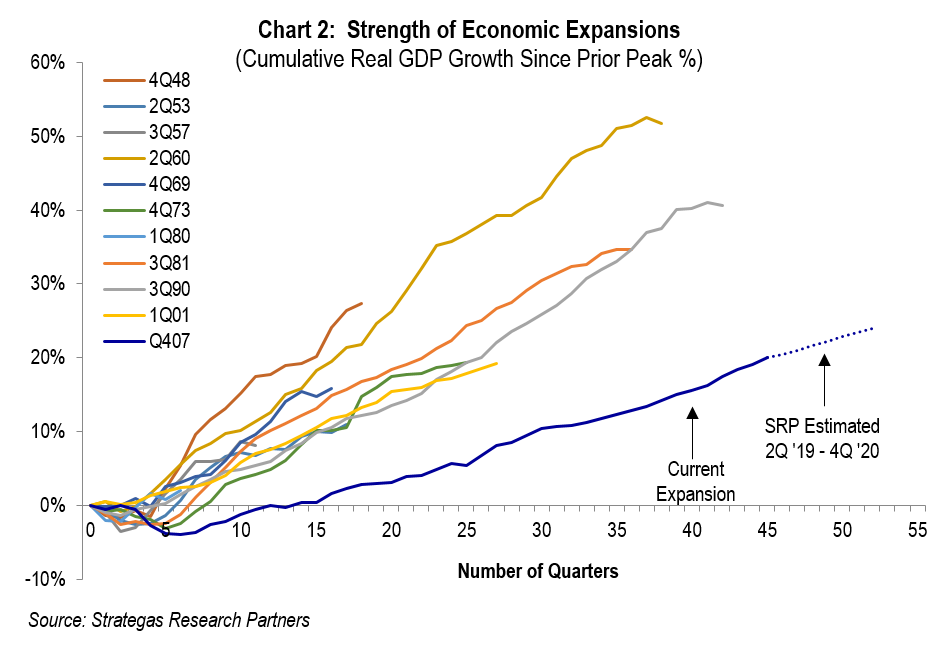

As evidenced by fourth quarter outflows from equities (not from our clients), it would appear that conventional wisdom suggested exiting equities and buying bonds. Cited reasons were that many believed recession was right around the corner (later this year) and that the trade war with China would damage our economy and result in higher inflation. Pundits also cited the length of the long bull market. Our analysis led us to take the contrarian view and with that we stayed the course in our equity investments among both our defensive and traditional equity baskets. Our view was that the economy would continue to grow, which was evident in the fourth quarter of last year and the first quarter of this year. Growing employment in both quarters also supported our thesis. In addition, we studied the strength of prior economic expansions post-recession. In other words, how robust has this current economic expansion been (not just how long has it lasted)? Thus we did the “painful” job of thinking as opposed to following the conventional thought of getting out of the equity markets. The following chart clearly shows that despite the age of this expansion, the cumulative growth in real GDP is still below the average of other such economic recoveries:

The dark blue line represents the current economic expansion and is below that of the others, clearly demonstrating that this economic expansion has not yet provided the annualized growth rate that all but one since 1948 has. In our opinion, given the low level of interest rates and inflation, continued strong employment growth (but slowing somewhat), moderate wage growth and a high level of consumer confidence plus recent tax cuts this expansion is not over and that recession is still a ways off!

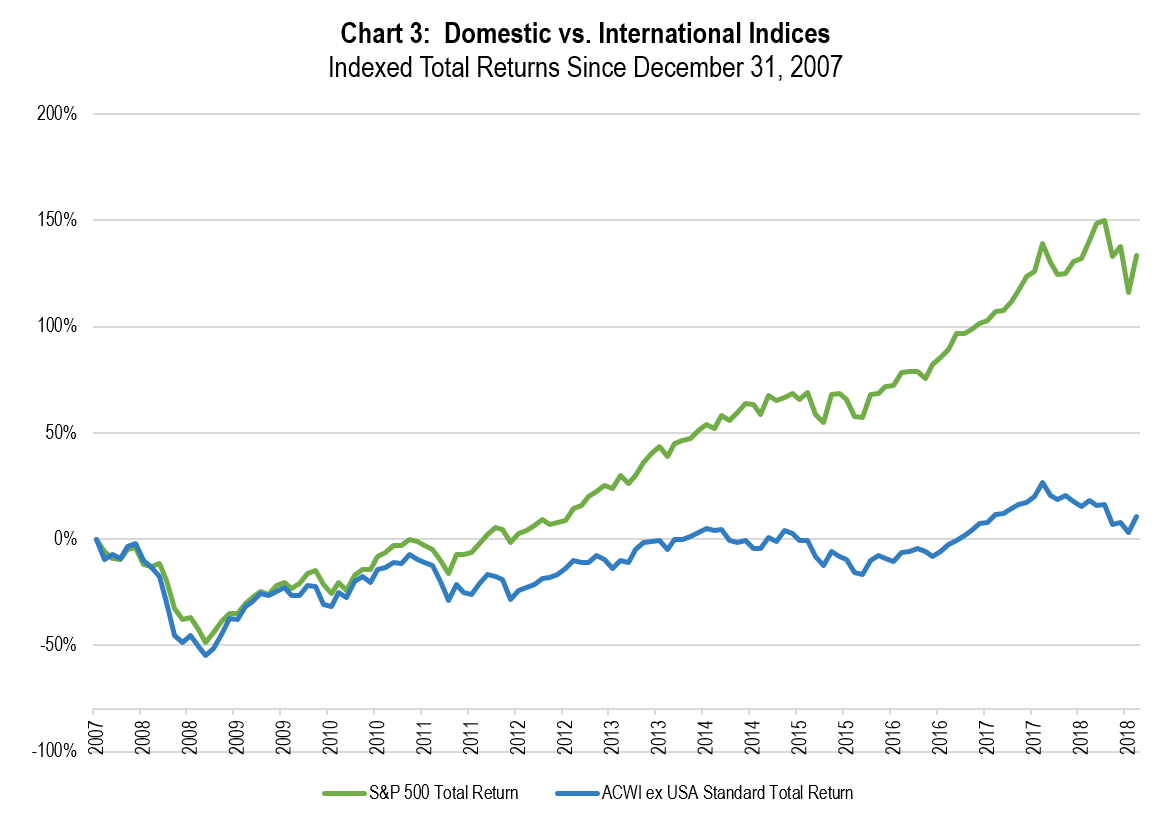

Additionally, we believed that the Fed would back track on the position it stated in late September that it would continue to raise rates. In fact, Chairman Powell stated in January that rates would be held steady, and in June more than hinted that rates just might be reduced (Fed futures are now pricing in multiple rate cuts). We believe that the current low interest rates (U.S. ten-Year Treasury is 2.0%, as of June 30, 2019) help equity valuations as well as the economy. We believe that low interest rates globally (German bund at –0.3% and Japan ten-year at -0.2%, both as of June 30, 2019) reflect low inflation and indicate that those governments are trying to induce investment and growth. GDP growth in certain European countries and Japan is near zero, leaving the United States and China as the primary drivers of the global economy. Accordingly, we continue to underweight international equities as we still see better investing opportunities through domestically domiciled companies (domestic equity indices have outpaced international indices for seven of the past ten years). Thus for now, our overweighting domestic equities has helped our clients:

Our advice has been something other than the conventional, based on our evaluation of fundamentals of companies and a study of the economy. We have over-weighted equities, both in our defensive and traditional baskets while underweighting fixed income and alternatives for most clients (hedge funds continue to lag equity markets in most cases). Our equity bias has been to U.S. domiciled companies with an underweight to international, including emerging markets. We do not see a recession for the next year or longer unless something out of the ordinary (such as a war) should befall us. The yield curve is puzzling with one widely followed measure suggesting a recession (the three month compared to the ten-year is inverted) while the comparison of the two-year Treasury with the ten-year Treasury is not inverted (suggesting no recession in the next year or so). Our banking system remains very strong (all major banks passed their most recent Dodd-Frank Act Stress Test) while we continue to see reasonable (2% to 3%) GDP growth in the U.S. with continued low interest rates and low inflation. This should favor equities, particularly growth stocks. If the economy should pick up steam towards the higher end of our range then we believe we would see more cyclical and industrial stocks start to outpace growth companies.

We believe, for now, that an overweight to our defensive equity strategies, a modest underweight to our traditional equity strategies (with a bias to growth stocks in both baskets for now), and an underweight to fixed income (yields remain very low and if there was an interest rate surprise to the upside, longer duration portfolios would be hurt) is the best course for most clients. In other words, there is a high degree of risk to bond values when the ten-year U.S. Treasury is trading in the 2.0% to 2.5% range (not as to quality of the U.S. Treasury, but as to price sensitivity to higher interest rates). We continue to recommend that suitable clients round out their asset allocation with some investments in the private equity and real estate space.

Summary

We have had strong absolute returns for all of our equity-based strategies for the year through June 30, 2019. Bond returns are more modest, and those outside of FLI who fled to bonds in the fourth quarter missed out on solid equity returns. The economy, as mentioned, continues to grow moderately despite some headwinds from the trade war with China and concerns about hot spots in the Middle East. The agreement to restart trade talks with the Chinese is positive but there is no guaranty that an agreement can be reached. The fact that President Trump has not put a deadline on an agreement is also positive, but will most likely result in the negotiations dragging out. The political situation in Washington remains murky at best with little or no collaboration between Republicans and Democrats (other than the most recent aid bill for the Southern border). This will only worsen, in our opinion, as the looming 2020 election cycle picks up steam. Valuations for average equities are obviously somewhat higher now than the beginning of the year and requires continued monitoring (the S&P 500 is trading at about 16x 2020 projected earnings (which is about average for the past ten years). In our opinion, active management with concentrated portfolios like ours should prove helpful as gains become somewhat more difficult.

However, the 180 degree turn by the Fed from raising rates (September 2018) to holding rates (January 2019) to possibly reducing rates (June 2019) is significant. If short term rates are cut (the next Fed meeting is July 30-31, 2019), it could bode well in elongating our economic expansion which in our opinion would lead to higher earnings for the companies we invest in. These rate reductions, if implemented by the Fed, would serve to possibly mitigate some of the economic upsets mentioned throughout this report (in particular negative consequences from a continuation of the trade war with China or a possible oil disruption in the Middle East).

With all of these factors to consider, we remain with a defensive tilt given the balance of uncertainty as well as the positive factors of a still growing economy and the prospects for lower short-term interest rates. We achieve this by recommending that clients overweight our defensive basket. We would not be too concerned if the economy slows somewhat in the short term as we believe it is human nature for businesses to somewhat pull back on their investing and hiring activities while trade talks with China and the potential greater tariffs cloud their vision of the future. Finally, there remains the potential for some escalation in hostilities between the U.S. and Iran. This in our opinion would also cause some short-term volatility especially if other countries join in.

We are pleased that thus far this year our clients are enjoying better than reasonable returns in all of our equity-based strategies (and reasonable returns in our multi-strategy hedged investment strategy). Modest gains thus far for our bond portfolios have been achieved, while keeping duration short. The risk of higher rates down the road could cause bond losses on paper for longer-duration bonds bought to achieve higher yields in this low rate environment. Our current real estate debt investments are progressing. However, we are mindful of the worries (and perhaps something that we cannot predict) that come from political, geopolitical, and economic factors which could derail our strong start six months into the year. We will watch the factors mentioned throughout this report very carefully and take action where appropriate (while being mindful of taxes for our taxable clients).

Please remember, the conventional view is easy to accept as it protects one from the painful job of thinking and doing homework. We at FLI will not succumb to this and will continue to do our homework on behalf of our clients, and ourselves, as we continue to invest side-by-side.

We hope that you have an enjoyable summer and please do not hesitate to call upon us for any of your wealth and investment management needs.

Best regards,

![]()

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. Partnership returns are estimated and are subject to change without notice. Performance information for Dividend Growth, FLI Core and AB Concentrated US Growth strategies represent the performance of their respective composites. FLI average performance figures are dollar weighted based on assets.

The views expressed are the views of Robert D. Rosenthal through the period ending July 19, 2019, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC. Copyright © 2019 by First Long Island Investors, LLC. All rights reserved.

NEW YORK, July 29, 2019 — Kudu Investment Management, LLC, a provider of permanent capital solutions to asset and wealth managers worldwide, has acquired a passive minority interest in Jericho, N.Y.-based First Long Island Investors, LLC which oversees approximately $1.6 billion in assets for high net worth individuals and families. Terms were not disclosed.

First Long Island was co-founded in 1983 by Robert D. Rosenthal and Ralph F. Palleschi, prominent local entrepreneurs who earlier in their careers were senior officers at both Entenmann’s national baked goods company and the Islanders pro hockey franchise. Rosenthal conceived First Long Island while working with Palleschi on the financial and investment needs of the Entenmann family. The operating and investing experience they gained from these endeavors made them attractive to similar clients – business owners, entrepreneurs, and wealthy families. They are well-known for delivering investment and wealth management services rooted in their core principles of trust, service, and performance.

“Bob and Ralph and their team have built an exceptional franchise, serving entrepreneurs and other high net worth individuals in the greater New York area. We look forward to them continuing their uniquely client-centric approach that is evident in every aspect of the relationship from asset allocation to service, communication, and more,” said Kudu CEO Rob Jakacki.

“The Kudu team really understood our service culture and entrepreneurial DNA. We were attracted to their philosophy of only investing in firms that continue to be managed and controlled entirely by their existing owners,” said Rosenthal, who is First Long Island’s chairman, CEO, and CIO. “Kudu also brings us a top-tier and growing network of partner firms and relationships we hope to leverage as we enter our next phase of growth.”

Kudu’s partners include West Coast wealth manager B|O|S; New York property fund manager Savanna; alternative asset platform TIG Advisors; real assets investor Versus Capital; and European alternative credit specialist Fair Oaks Capital. Kudu’s partners collectively manage approximately $19 billion in AUM for institutional and individual investors.

Sandler O’Neill & Partners, L.P. acted as financial advisor and Seward & Kissel LLP served as legal advisor to First Long Island Investors, LLC. Dechert LLP served as legal advisor to Kudu Investment Management, LLC.

About Kudu Investment Management, LLC

Kudu specializes in providing permanent capital solutions—including generational ownership transfers, management buyouts, acquisition and growth finance, as well as liquidity for legacy partners—to asset and wealth managers. Kudu was founded in 2015 and is backed by capital partner White Mountains Insurance Group, Ltd. (NYSE: WTM). For more information, please visit Kudu’s website.

About First Long Island Investors, LLC

First Long Island Investors is a Jericho, N.Y., based wealth management company dedicated to providing individualized advice and counseling in the preservation, growth, and administration of liquid and illiquid wealth for high-net-worth individuals, families, and select institutions. The team strives to provide its clients with sound advice, best-in-class service, and an unparalleled level of trust, which includes its principals investing alongside its clients. The firm, founded in 1983, oversees approximately $1.6 billion in assets (as of June 30, 2019). Visit fliinvestors.com for more information.