March 31, 2020

“Do not judge me by my successes, judge me by how many times I fell down and got back up again.” Nelson Mandela

The first quarter, following an excellent year in 2019, commenced with reasonably strong results consistent with what was a strong economy characterized by near record employment, low interest rates, and low inflation. And then, “out of the blue,” came the coronavirus leading to what could be the greatest medical crisis, a global pandemic, the world has seen since the H1N1 pandemic (Spanish flu) of 1918. Emanating from a region in China, this disease, now known as COVID-19, has cast its horror on over 180 countries with the United States being hit the hardest. To boot, the epicenter, for now, is New York accounting for more than a third of the cases in our country.

The response by the President, the House and Senate, and the Federal Reserve has been rapid and bold, although many believe that our testing capability was slow to ramp up and that the Chinese were not as transparent and forthcoming as they could have been. Despite some missteps, the collective clout of the Administration and its task force, our Congress people, the vast majority of Americans, a resilient private sector including numerous leading companies, and research centers at hospitals and universities around the world, gives us optimism that we will defeat this invisible enemy in time.

However, without a vaccine (which scientists around the globe are working to develop) and treatment for the symptoms of the dreadful virus, the only prescription for stemming the tide of this scourge is social distancing and staying in our homes. This prescription has an obvious side effect, the crippling of our economy and that of the world economy. Despite our economic strength coming into 2020, we are now faced with an economic contraction that could take us from a 50-year low unemployment rate of 3.5% to potentially an unemployment rate as high as 20% or more. Small businesses shuttered, hotels nearly empty, airlines with drastically reduced flights and millions unemployed, our domestic economy and that of the world have fallen off a cliff for now.

Domestically, several bipartisan laws and the actions of the Federal Reserve will infuse trillions of dollars into our economy to aid the unemployed, small businesses, and various industries that have been crippled. This is to buy time for so many while waiting for the defeat of the virus and a return to some normalcy. (At some point we will have to deal with the potential of inflation given the mountain of debt being created.) Will it be like it was before or will it be a “new” normal? Only time will tell. Will most buying and traveling habits of Americans return to what they were? Only time will tell. Will Americans be comfortable attending sporting events, the theater, and the movies again? Only time will tell. We just do not know, except, if history is a guide, we as Americans will get up again and return to some significant level of normalcy.

When one thinks of all of the tragic events, market disruptions, and medical crises of the past we can think of two World Wars, the Spanish flu of 1918, the polio epidemic of the 1950’s, the oil crisis of the mid 1970’s, the hyper-inflation of the early 1980’s, the AIDS pandemic, the stock market crash of 1987, the implosion of Long Term Capital Management and the currency crisis of 1997, the tech bubble and collapse of 2001-2, the 9/11 terrorist attacks on the U.S., and the financial crisis (the “decession”) of 2008-9 as well as the Korean and Vietnam Wars. In most of these instances, financial markets fell dramatically or even crashed. Behavioral patterns for many Americans changed for a period of time. Yet at the beginning of this year, America was enjoying its possibly greatest period of prosperity with employment and the stock market at historic levels. In addition, housing prices were at or near their highest. And then “out of the blue.”

So, it is our opinion at FLI that once this virus is beaten (and we believe it will be), Americans and our businesses, with the help of the federal and state governments along with our strong private sector, will pick themselves up yet again!

How Do We Invest?

Let us be candid, we face an ugly medical crisis and a severe recession that we believe will be short lived. The ultimate numbers in terms of Americans and others falling prey to this virus will be horrifying. The number of unemployed will be startling and the number of shuttered businesses, despite help from the government, will be incredibly sad. We might also see empty hotels and dry docked cruise liners for quite some time. I sometimes speak of looking over the valley to the other side when overcoming economic hardships. This time we might be looking over the Grand Canyon, but just for what we believe will be a relatively short period of time. It could be six months or a year. Perhaps even longer.

If there is one thing that we have seen over all of the sad events in the last hundred or so years, is never ever count out Americans and American business. We always pick ourselves back up thanks to the resolve, ingenuity, creativity, and entrepreneurialism of the American people and our capitalistic system coupled with our democracy.

Our customized, prudent asset allocation for our clients today has, and always has had, security and defensive components. I am glad to say that our security and defensive baskets, although down, have for the most part preserved our clients’ capital better than the larger losses experienced in many of the traditional equity indices. All of our traditional equity strategies except one are outpacing their respective indices. We have always focused on quality companies with strong balance sheets. In several of our strategies we have made modest changes to further strengthen the quality where we could. We have not sold out or gone to cash trying to predict the bottom and then having to decide when to jump back in. Our experience over the years has suggested that selling into a panic is typically a big mistake, so we have not.

Where we could increase our equity weightings in secular growth trends like online purchasing, cloud computing, high-quality pharmaceuticals and medical instruments, or 5G technology we have. Social media companies and online search engines are also areas we believe will experience growth. Additionally, we should not forget electronic payments (especially important while being at home). Our goal is to preserve capital by owning strong companies that are well managed and look to the future. At the same time, in our Dividend Growth strategy we have focused on the balance sheets of our portfolio companies to increase the probability that dividends will at least be paid, and in many instances be increased, as they have for so many years.

The bottom line is that we are staying the course with our allocations to the baskets of security, defensive, and traditional equity strategies. Also, our mezzanine loan strategies seem to be weathering this period of stress as the properties we lend to are all very well located.

We have not included any charts showing macro- and micro-economic trends or valuation graphs based on earnings and interest rates because they would not mean much at this point as it is virtually impossible to predict much of anything economically this year. Our focus is on 2021 and beyond when we believe much will return to some normalcy. Our strong belief is that the prices we are seeing now for the companies we are investing in will be higher in a year or two. If anything, we view this as a long-term buying opportunity for the highest quality companies that have durable growth prospects, strong balance sheets, and/or the ability to pay meaningful dividends.

We believe that America and its companies will again pick themselves up as they have following periods of extreme stress in the past. We would ask you to judge us the way Nelson Mandela has suggested– by the way we pick ourselves up along with your entrusted funds.

Please do not hesitate to call any of us at First Long Island and most importantly stay safe and practice social distancing, and if possible just stay at home for now.

Best regards,

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. Partnership returns are estimated and are subject to change without notice. Performance information for Dividend Growth, FLI Core and AB Concentrated US Growth strategies represent the performance of their respective composites. FLI average performance figures are dollar weighted based on assets.

The views expressed are the views of Robert D. Rosenthal through the period ending April 23, 2020, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC.

Copyright © 2020 by First Long Island Investors, LLC. All rights reserved.

Background

We as a firm, had an excellent 2019 in absolute returns, making up for a downturn in the fourth quarter of 2018 caused by the premature Fed tightening and an evolving trade war with China. 2020 began with gains in the U.S. markets supported by the expectation of domestic growth fueled by almost record employment and strong consumers buttressed by low interest rates and low inflation. Corporate earnings were projected to increase modestly over 2019. Domestic GDP growth projections for 2020 and 2021 were between 1.8% and 2.2%. Stocks looked reasonably attractive to us especially when compared to low-yielding bonds. However, this level of valuation was attractive only if the projected earnings growth materialized.

Coronavirus

Reality interfered with our plans when “out of the blue,” a vicious virus emanated out of Wuhan, China in December 2019. It is believed the Chinese delayed disclosing the true nature of this coronavirus and the critically important fact that the virus was spreading from human to human – community spread. This element gave rise to what would become a global pandemic as Chinese nationals and visitors to and from China became lethal carriers of the virus. Unsuspecting nations including the U.S. and all European countries became victims, both victims of disease and the ensuing economic contraction necessary to stem the tide of the growth of this heinous virus. Social distancing and “shelter in place,” both prescriptions for killing the virus as well as killing the economy, have become part of the norm!

Unfolding Impact

What is now occurring is a two-pronged war. The first is a medical war against the virus. Our soldiers are healthcare forces made up of frontline doctors, nurses, physician assistants, and all others on the front lines in all medical facilities. They are battling day and night with the beginnings of a surge of patients as testing for the virus ramps up. The virus remains highly contagious and some carriers have no symptoms. Unprecedented amounts of testing are now being undertaken, but at a slower pace than required. The best prescription to stem the tide of disease spread is social distancing which has become the cause of our second war, the economic one.

Social distancing has required the shutdown of an unprecedented amount of commerce. Cruise lines, airlines, hotels, casinos, all professional sports, and live events (including concerts) began the economic contraction. Now given the disease spread, government at both the Federal and state levels have created guidelines limiting groups to no more than ten or even worse “sheltering at home.” Businesses have had to adapt to having employees primarily working remotely. Virtually all restaurants, bars, and clubs throughout the country have temporarily closed. Tens of thousands of workers are being let go or furloughed on a daily basis. Most automobile production facilities have closed. Schools, kindergarten through twelfth grade, across the country as well as many universities have sent students home indefinitely.

This unprecedented dislocation of our way of life appears to be necessary to limit the spread of the disease and keep the fatality level down by spacing out hospital admissions in an attempt to deal with the capacity of our hospitals. Additionally, this disease is particularly severe for seniors and people with preexisting health conditions. There is really no way to adequately describe this challenge although it is one we believe that we as a nation will beat in time.

Economic Impact

Clearly, this “out of the blue” global pandemic has already brought an end to our 11-year bull market and will cause a recession. A recession that a month ago seemed very unlikely to us. It has also brought incredibly rapid government action along with decisive and bold Fed action lowering interest rates and using the Fed balance sheet in many developing ways. It is expected that well in excess of a trillion dollars will be earmarked for afflicted workers, small businesses, and certain major industries. Hopefully our elected officials can come together in the next few days and leave behind partisan politics.

Investment Implications

As we write this, the S&P 500 Index has declined 30.4% year-to-date and declined 33.8% from its high in mid-February. With so many industries and companies, big and small, curtailed or closed for an unknown period of time, corporate earnings and GDP will substantially decline. Thus we are undoubtedly in recession and the stock market is declining. High-quality bonds have performed better than high-yield, low quality bonds. Real estate values will likely decline as commercial tenants defer or renege on rents. Shopping centers are closed as stores have been forced to close, waiting out the hoped-for decline in disease spread.

In addition to this debacle, our economy also is digesting an oil war resulting from the failure of OPEC countries to reach agreement on limiting supply, primarily between the Russians and OPEC countries led by the Saudis. The good news for now (for consumers and businesses) are lower oil and gasoline prices. The bad news is the impact of collapsing prices on America’s oil and oil shale businesses. This could also impact debt arrangements with many domestic banks.

Looking Across the Valley

As long-term investors, we have experienced other periods when unexpected events led to substantial market declines. October 1987, the dotcom crash of 2000-2002, and the financial crisis of 2008-2009 were other periods where we faced dramatic market routs. Our advice then was the same as it is now: stay the course in high-quality companies, bonds, and real estate. Valuations have become quite attractive assuming that the companies we invest in will at some point in the not too distant future return to “normalized earnings.” Some companies that we invest in might even benefit in the short- and long-term from this crisis including Amazon.com, Facebook, and Alphabet (Google’s parent company). Additionally, other companies that we have an interest in will ultimately benefit from new 5G technology like QUALCOMM, or the continued move towards cloud computing such as Adobe and Microsoft. We believe there is a certain inevitability of a return to normal where great companies will prevail. Look to 2021 for more normal earnings and economic conditions.

However, for the time being the equity markets are falling quickly. To make matters worse, high-quality companies are falling along with lower-quality ones. Future earnings and dividends do not seem to matter in the short term but our experience tells us that they will matter in time. Vitally needed pharmaceutical companies are trading at what we believe will be viewed as bargain prices with many paying high dividends based on the reduced share prices of these companies. Banks that are well capitalized are also in free fall despite rock solid balance sheets. Technology companies, as mentioned above, with great prospects also have fallen victim to the panic selling. Every sector of the S&P 500 is down at least 20% with more than half of them down more than 25%. There appears to be a disregard for a future that is brighter than the gloom and uncertainty of today.

As we have often said, we own interests in real companies that have assets and almost always make a profit. In today’s world, that does not seem to matter, but it will. We believe many of these companies are cheap and deserve to be held for the long term.

The consumer, who is the backbone of our domestic economy, has suffered a vicious gut punch. A punch that has temporarily stopped many from working, shopping, eating at restaurants, and participating in activities that were always taken for granted. Unemployment will soar in the weeks to come. Many smaller businesses will close. This is war. We need the Federal government to come to the aid of the consumer, worker, and business. We expect that to happen shortly. This will make a difference and the sooner the better.

How to Invest

Our adherence to a prudent asset allocation has worked for us to a degree. Many of our defensive and traditional equity strategies are outperforming their benchmarks despite being sharply down. Quality will ultimately prevail. Diversification in having some bonds and defensive strategies is keeping our clients in the battle.

We do not know where the bottom is as we have no crystal ball. However, we believe we know good prices for solid companies, and those of today seem like good prices for many. However, they could get even better. That said, if one has additional liquid assets (beyond what is needed to either live on or sleep at night) we would consider deploying in stages to what we believe is an exceptional long-term opportunity for the future.

Hold on and let’s beat this invisible enemy, the coronavirus. Once we as a society and government do that, you can count on America as consumers and businesses to come back. We always do.

Thank you for your confidence in us and the kind words many of you have said to us as we have reached out to you during this surreal period of time. Please do not hesitate to call.

Stay safe and practice social distancing and good hygiene.

In good health,

Robert D. Rosenthal, Chairman, CEO, and Chief Investment Officer

and

Ralph F. Palleschi, President and Chief Operating Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. Partnership returns are estimated and are subject to change without notice. Performance information for Dividend Growth, FLI Core and AB Concentrated US Growth strategies represent the performance of their respective composites. FLI average performance figures are dollar weighted based on assets.

The views expressed are the views of Robert D. Rosenthal through the period ending March 23, 2020, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC. Copyright © 2020 by First Long Island Investors, LLC. All rights reserved.

First Long Island Investors is proud to announce that Robert D. Rosenthal, our Chairman, CEO, and Chief Investment Officer, has been named to the Long Island Press Power List. Bob’s commitment to excellence in both is business and philanthropic efforts is commendable and he is honored to be recognized among such an esteemed list of peers.

https://www.longislandpress.com/2020/02/04/17th-annual-long-island-press-power-list-announced/

The 2019 investment landscape produced strong returns across equities and fixed income against a backdrop of low interest rates, flat earnings growth, and a slower growing economy with record low unemployment, rising wages and a strong consumer. Will 2020 be more of the same or not and how should a long-term investor position his/her portfolio for growth given all of the uncertainty?

In a recent web seminar members of the FLI Investment Committee reviewed the positive economic factors as well as the elements contributing to the wall of worry as we aim to make sense of the markets for our clients and position portfolios for long-term growth.

A transcript of the session is also available.

December 31, 2019

Listen to the report.

“It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.”

Robert Kiyosaki

(First, I would urge all of our clients and centers of influence to read our 2020 Investment Outlook which was distributed earlier this month, as it provides additional details on many of the thoughts that will be reflected in this abbreviated Investment Perspective.)

The fourth quarter and 2019 overall rewarded long-term investors with a robust equity market as well as gains in fixed income. All of our equity-based defensive and traditional equity strategies gained between 20% and 37% for the year, on a net basis. The Dow Jones Industrial Average, the S&P 500 Index, and the NASDAQ all reached record highs in the fourth quarter reflecting several significant factors. First, the Federal Reserve maintained reduced interest rates and suggested that it would not raise rates in 2020 unless inflation picked up significantly. Second, the President and his trade team announced, along with the Chinese that a Phase One trade arrangement with China had been agreed upon. This had the immediate effect of proposed tariff increases not taking place in mid-December as well as a partial roll back on already imposed tariffs. The equity markets greeted this news with significant gains throughout the month of December. Also, Congress agreed to the new U.S./Mexico/Canada trade deal replacing NAFTA. This too bodes well for our domestic economy and when coupled with the Chinese trade deal should relieve businesses that had held back on investments given the uncertainty regarding global trade.

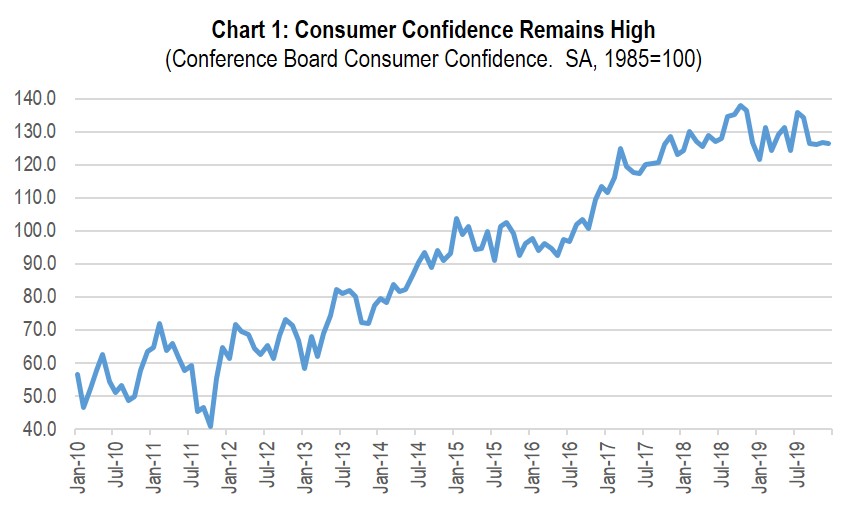

In addition to the above, the strength of the consumer was a major factor positively impacting the fourth quarter, and for that matter, the entire year. The consumer accounts for nearly 70% of our economic activity and has been strengthened by a very low unemployment rate of 3.5%, which is the lowest in 51 years. This, combined with wage growth now achieving 3%+, was reflected in a high level of consumer confidence (Chart 1).

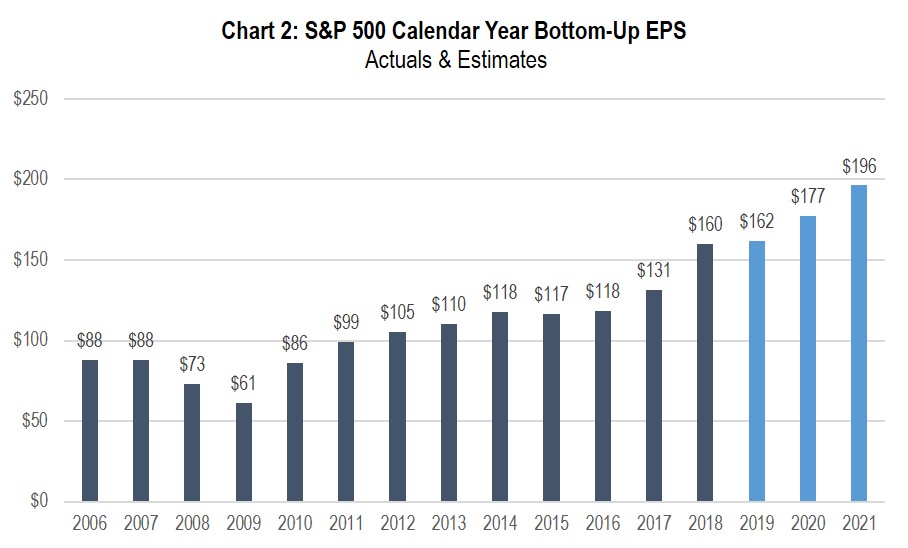

This high level of consumer confidence, a strong holiday season for retail sales, low inflation and continued low interest rates resulted in a strong fourth quarter. The S&P 500 Index, for example, increased by 9.1%! This is contrasted with the significant decline in the fourth quarter of 2018 (-13.5%) resulting from, in our view, the Fed’s premature policy to raise rates and the declaration of a trade war with China by President Trump. The 2018 decline was despite a significant rise in earnings for the S&P 500 (Chart 2).

Chart 2 shows that earnings increased (in large part from tax reform) in 2018 and were flattish for 2019. However, the stock market did the opposite of what one would have expected. 2018 resulted in a modest decline caused by the big drop in the fourth quarter, while in 2019 the markets rallied while earnings do not appear to have grown significantly. (2019 earnings are still yet to be reported for most companies.) Fundamentals in terms of valuation and other factors made us stay the course in terms of being exposed to the equity markets over this two-year period. We also “faced down” the suggestion that recession was imminent. (We stated a year ago that we did not believe that was the case and we turned out to be right). We maintain that a recession is not imminent and we do not believe that there will be a recession in 2020, barring some unexpected external event. With trade somewhat resolved and a very strong consumer, we continue to believe that our domestic economy will grow by at least 2% in 2020. This should bode well for corporate earnings in 2020.

Of course, we currently face both political and geopolitical risks. The President has been impeached by the House and the trial has begun in the Senate. This coupled with a Presidential election (as well as all seats in the House of Representatives and one-third in the Senate being up for reelection) less than ten months away could cause volatility in terms of potential policies espoused by both sides of the aisle. One could say there is a real battle developing between capitalism and potential democratic socialism if one looks at the extreme positions being bandied about. We doubt that either capitalism will go away or that democratic socialism as we see elsewhere in the world will take its place. However, real issues in terms of wealth inequality, the future funding of our social safety nets, and both annual deficits and accumulated debt will have to be dealt with one day by our elected officials.

Geopolitical hot spots, which have just gotten hotter, are also of concern. The situation with Iran is front and center given the President’s decision to take out Iranian general Qassem Soleimani, who was known as Iran’s “shadow commander” and viewed as a ruthless killer. There seems to be no argument that he was a terrible person responsible for many American deaths and maimings, as well as the slaughter of thousands in his own country and other countries around the Middle East. However, what this killing leads to is causing great concern and could result in stock market volatility. Plus, we cannot forget the issues with North Korea as well as Russia.

We always focus on valuation when evaluating a company, or other investment opportunity. The fourth quarter reflected investor optimism despite the fact that earnings did not grow much for the year, as shown in Chart 2. However, with interest rates as low as they are and global trade issues seeming to be at least partially resolved, share prices rose in the fourth quarter. With no recession in sight and the prospects for a growing economy and growing earnings, we remain “skeptically optimistic.” However, not all companies, all real estate, nor all investments will prosper in the year to come. So, selectivity remains our mission again this year. (Please refer to our 2020 Investment Outlook for additional information.) Companies with long-duration earnings growth and financially strong companies able to increase their dividends from year to year based on growing cash flows are the places to be in our opinion. It worked last year and we expect it will work again this year.

The fourth quarter gains were again biased to growth (as were many of our strategies), large-cap, and U.S. domiciled companies. Other asset classes did well, but not as well. Our underweight to international worked once again in 2019. We are watching this closely as the better trade environment and monetary/fiscal stimuli being introduced by China and Japan might make international investing more attractive going forward. A resolution to the Brexit situation should help as well. However, we would rather be a bit late to that party. Our approach to international has worked, on average, over the past 10 years.

We had a great fourth quarter led by our defensive equity and traditional equity strategies. We believe that our mezzanine real estate investments continue to do quite well. Given the political and geopolitical risks we have mentioned, we will remain with a tilt towards the defensive and still believe that will result in reasonable gains for the year. As well, we continue to underweight fixed income and cash where returns remain in some cases below the rate of inflation. As stated in our introductory quote, we need to have our capital working for us over the long term.

We hope you will join us for our web seminar on February 13, 2020 at 2 PM EST where we will review our 2020 outlook and approach to long-term investing.

Happy and healthy New Year!

Best regards,

Robert D. Rosenthal

Chairman, Chief Executive Officer,

and Chief Investment Officer

*The forecast provided above is based on the reasonable beliefs of First Long Island Investors, LLC and is not a guarantee of future performance. Actual results may differ materially. Past performance statistics may not be indicative of future results. Partnership returns are estimated and are subject to change without notice. Performance information for Dividend Growth, FLI Core and AB Concentrated US Growth strategies represent the performance of their respective composites. FLI average performance figures are dollar weighted based on assets.

The views expressed are the views of Robert D. Rosenthal through the period ending January 24, 2020, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Content may not be reproduced, distributed, or transmitted, in whole or in portion, by any means, without written permission from First Long Island Investors, LLC.

Copyright © 2020 by First Long Island Investors, LLC. All rights reserved.